The strange thing about the mechanism, the starting point for the cattle market: selling the air is the puzzle that will inspire the next round of the cattle market

This is the next round of the Yamashita Bulls。

Original by: Danny (X:@aginnder)

For 300 years, there has been a pattern that has been repeatedly tested in the financial markets: the cattle market has never been set on fire by a narrative, but by the upgrading of trading mechanisms. Whether ICO, the Enduring Contract, AMM, DeFi, NFT... are the mechanisms that drive the game, which brings money into the cycle. It is the upgrading of mechanisms that brings prosperity。

Looking back at the starting point of each big thing, you'll find that what they all have in common is not "a good story" but "a new way of playing."。

It's not a narrative, it's an evolution of every trading mechanism

This rule, from Wall Street to Currency, from spot to contract, from DeFi Summer to Hyperliquid, never expired。

You can short it, you can empty it -- an aka is the next round of Yamamoto Bulls。

In 1609, a Dutch businessman changed his financial history

1609, Amsterdam。

THE DUTCH COMPANY EAST INDIA (VOC), THEN THE WORLD ' S LARGEST LISTED COMPANY, MONOPOLIZED THE TRADE IN ASIAN SPICES, WITH STOCK PRICES RISING. EVERYONE'S BUYING, EVERYBODY'S MAKING MONEY. THE MARKET HAS ONLY ONE DIRECTION — UP。

Then a businessman named Isaac Le Maire did something that everyone thought was crazy: He borrowed VOC's shares, sold them and bet it would fall。

This is the first empty trade ever recorded in human history。

The Dutch government is angry. Parliament considered this to be a malicious attack on the State-backed enterprises, and legislation prohibited the use of empty space. Le Maire was publicly condemned. But the story does not end here — despite repeated prohibitions, empty acts never really disappear in Amsterdam. Because market participants discovered a fact that could not be denied by legislation: the price became more real when it became empty. Those overvalued stocks can no longer maintain their false prosperity indefinitely。

TODAY, 400 YEARS LATER, THE ENCRYPTION MARKET IS REPEATING THE SAME SCRIPT. IN THE MARKETS OF THOUSANDS OF COINS, ONLY BUY, NOT EMPTY. PRICES REFLECT ONLY HALF OF THE OPTIMISM, AND PESSIMISM IS FORCED TO SILENCE. EACH TURN IS THE SAME CYCLE: FOMO PUSHES, FOAM BREAKS, A CHICKEN HAIR WAITS FOR THE NEXT NARRATIVE TO START AGAIN。

But history has told us — every time a free-air right is introduced, it is not the end, but the beginning。

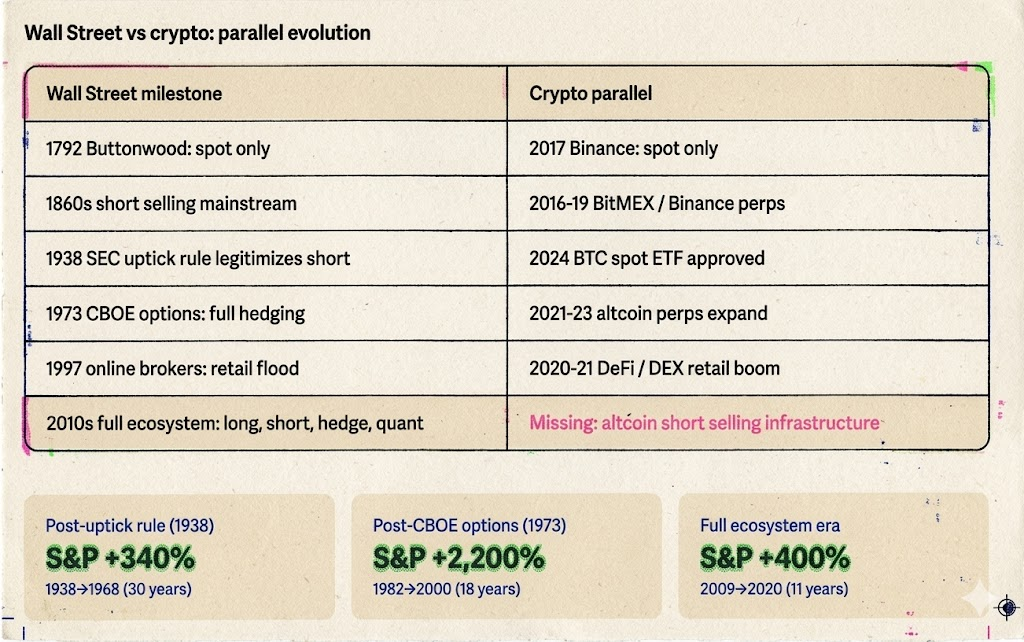

Two-hundred years on Wall Street: how to make space from "the enemy of the nation" to "the cornerstone of the market."

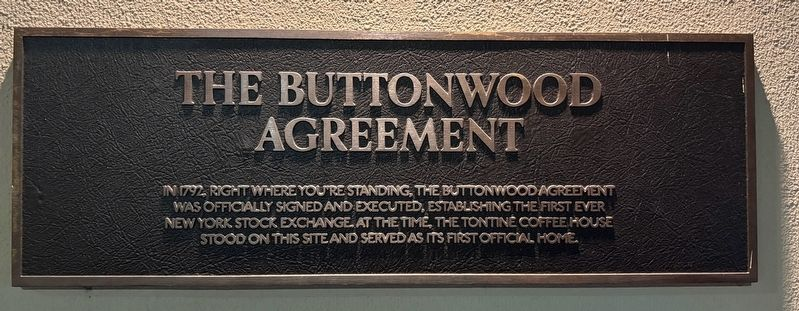

1792-1840: The Wild Age - there are only many original markets

On 17 May 1792, 24 brokers signed the Buttonwood Agreement under a tree on Wall Street, under which they agreed to trade in shares. This is the predecessor of NYSE。

The market at that time was similar to today's market for the Yamashita currency: it can only be bought, held, divided equally, for years. No leverage, no gaps, no standardized delivery process. The average daily turnover may be less than $500,000, with dozens of participants. The market is extremely small because there is too little that can be done。

Price volatility is driven entirely by multiple emotions. Good news, everybody buys, prices go up. Bad news came, everyone wanted to sell it, but because the market was too shallow to sell, the price fell. There are no empty buy-backs when they fall, so the market is not supported by nature, and the bottom depends entirely on when the last multiple loses。

It's like Meme, high FDV, low Float, 2024-2025

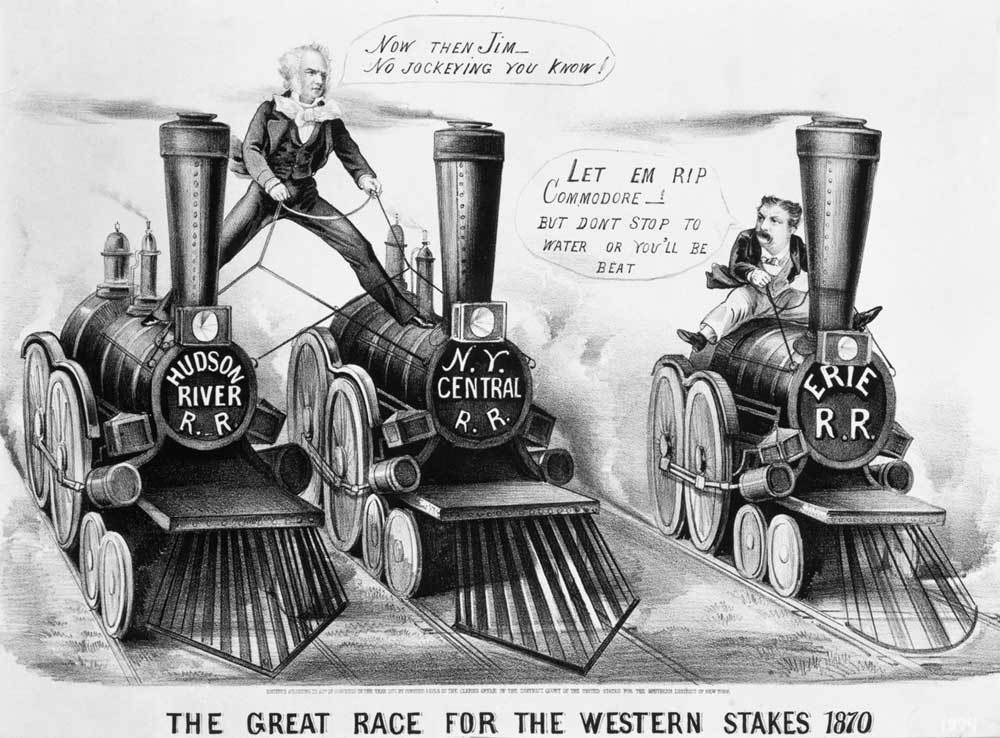

The 1850-1860s: Making space for the main stage -- fear comes with prosperity

In the 1830s and 1840s, a trader named Jacob Little made a fortune by doing nothing, known as "the first big hole on Wall Street." But it was a decade before and after the war with the North。

Daniel Drew, Jay Gould, Cornelius Vanderbilt - these names define Wall Street in that era. They staged a series of epic battles around the railway unit: Drew made empty Eric Railroad, Gould and Fisk joined forces to sniper Vanderbilt's multiple positions. These battles were bloody, chaotic and full of fraud, but the objective result was to make a secret weapon empty of a few people and turn it into a marking tool for Wall Street。

The social response is the same as in the Netherlands in 1609. Members of Congress call empty people "enemies of the State", and the papers say they "really rich by someone else's disaster." The public's fear of emptying has barely changed in 400 years。

But the market response is as positive as it was 400 years ago:

Each one creates a bill of sale, while the next one is a necessary one. The trade went up, the price gap narrowed, and more people were willing to come in. Wall Street began in a small circle of dozens of people, turning into a true capital market。

♪ 1938uptick rule: the tip of fear, the turn ♪

October 1929, Wall Street crashed. The Dow Jones Index fell by almost 90 per cent in two years. The anger of the public needs an exit, and empty head becomes the easiest target - Although the real culprits are the crazy leverage bubble and the systemic collapse of banks。

The United States Securities and Exchange Commission (SEC) was established in 1934. It is once again in danger of being totally banned. But the SEC made a historic choice: in 1938, it did not prohibit emptying, but instead introduced "uptick rule" -- - Emptyness can only be carried out when stock prices rise, so as to prevent empty space from breaking up。

The significance of this choice cannot be overemphasized. It establishes a principle that continues to this day: that what is done should not be eliminated and what is done should be regulated. Rules are not empty enemies, and rules are a prerequisite for empty legitimacy。

With rules, empty is no longer a grey area. The institutional funds, which were timid and now protected by the legal framework, were bold enough to participate on a large scale. Regulation has not killed empty space, making it safer and more credible and attracting more capital to markets。

That lesson, the encryption market has not really learned yet。

1973: Standardization of options - from one direction to four

On 26 April 1973, the Chicago Futures Exchange (CBOE) opened. Only 16 stock increases (Call) were traded on the first day. Put, joined in 1977. In the same year, Fischer Black and Myron Scholes published a Black-Scholes options pricing model to change financial history, which provides a mathematical basis for long-term trading。

The significance of the option lies in the fact that it expands the gamut of the market from two (buy-in/sale-out) to four (buy-off/buy-down/sell-out-down). For the first time, investors can express their judgment about the market in a very precise way — not just "up or down," but "in what time, at what speed, up or down."。

More critically, the option gives institutional investors a full pool of hedge weapons. In the 1980s, Bulls (S& P500 rose by more than 220 per cent between 1982 and 2000), the direct trigger was Volcker's control of inflation, the Reagan tax cuts and deregulation, but options provided a risk-management infrastructure that allowed agencies to dare increase their positions. If you can do it, you'll be able to do it again; if you can do it again, you'll get more money and the bulls will come。

For the rich and the institutions, controlling how to pull back is more important than how much money you can make -- the inconvenient nature of risk means that big money can't come in。

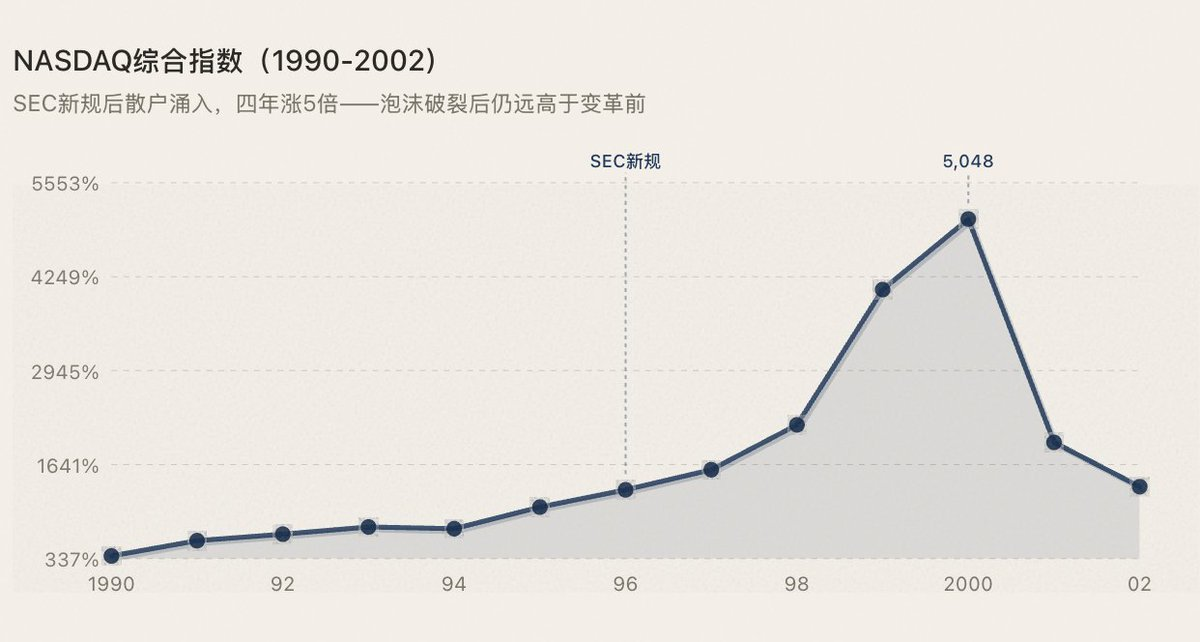

1996-1997: break-in in by the dispersed family

NASDAQ was the first electronic exchange in human history since its inception in 1971. The changes that were taking place in 1996-1997 were two things: the Council ' s Order Handling Rules broke the market monopoly on quotations; and the online coupons (E*trade, Ameritrade) pushed the turnover commission from $50 to $100 to less than $10。

THE FOAM EVENTUALLY BROKE, BUT THE MARKET VALUE OF NASDAQ WAS STILL MUCH HIGHER AFTER THE BUBBLE THAN BEFORE THE CHANGE — BECAUSE THE PARTICIPANT INCREASE FROM INFRASTRUCTURE UPGRADES WAS IRREVERSIBLE。

1993-2010: complete ecological maturity

Many thought that ETF was the product of nearly a decade, but the first ETF — SSY (Tracing Pistol 500) — was listed on the United States Stock Exchange in 1993. In 2001, the SEC imposed the Decimal Quoting (Decimalisation) price differential from $0.125 to 0.01, with a significant reduction in transaction costs. Between 2005 and 2010, high-frequency (HFT) transactions rose, once accounting for more than 60 per cent of United States stock market transactions. Quantified strategies, ETF arbitrage, multi-space hedges - all directions are supported by standardized tools。

Here, the U.S. stock game tool system is fully mature. Multiple, empty, hedged, arbitrage - every type of strategy can find a way to get in. Results:

In fact, the pattern can no longer be clearer: whenever a new trading mechanism allows more people to participate in markets, prosperity comes. (see figure below)

III. Eight years of the encrypted market: 200 years of evolution, eight years of travel

Wall Street was upgraded by a mechanism completed in 200 years, from the inception of Binance in 2017 to the maturity of the durability contract, which took less than eight years. But it's evolved to the base of the Yamashita. It's stuck。

2017 — Elephant Hour

Binance's on line, only spot. What can be done is the same as in 1792: buying, holding, waiting for an increase。

ICO FOAM IS THE BEST MIRROR. EVERYONE'S BUYING, AND THE PRICE CAN ONLY RISE. THE BUYOUT IS THEN DEPLETED — IN A MARKET THAT HAS NO EMPTY HEAD, THERE IS NO NATURAL SUPPORT WITHOUT A PAYBACK, PRICES ARE FREE TO FALL, AND THE BOTTOM DEPENDS ON WHEN THE LAST MULTIPLE DROPS. IT'S A TOTAL COLLAPSE. THIS IS EXACTLY THE SAME AS THE MARKET CHARACTERISTICS OF THE 1792 ERA OF ZIRCONIUM。

2016-2019 — Open weapons

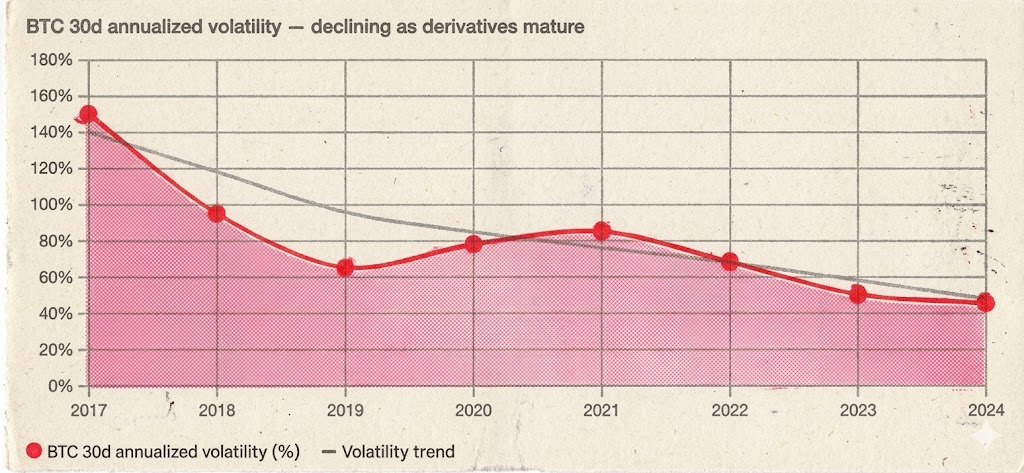

In May 2016, BitMEX launched the XBTUSD contract - the first empty tool in the encryption market. In September 2019, Binance went online to renew the BTC/USDT contract, emptying the mainstream。

What happened? The same thing that happened when Wall Street was introduced in the 1860s: a surge in liquidity, prices became two-way and volatility fell structurally。

BTC'S 30-DAY ANNUALIZED FLUCTUATIONS FELL FROM MORE THAN 150 PER CENT DURING THE CATTLE MARKET IN 2017 TO 60-90 PER CENT DURING THE CATTLE MARKET IN 2020-2021 — A GREATER BUT MORE ORDERLY INCREASE. THERE IS STILL A SURGE AND A FALL, BUT THERE HAS BEEN A MARKED DECREASE IN THE "NO-VOLUME DROP FOR THREE MONTHS" AS THE EMPTY PRICE-FIXING SLOTS ARE RESTORED, CREATING NATURAL SUPPORT。

More importantly, there has been a leap in funding levels. With a hedge tool, institutional funds are willing to enter on a large scale. You can't expect a fund manager who manages billions of dollars to throw money into a market that can only do more than that. The durability contract does not just give the occupant the right to empty, it gives the whole market an "institution-accessible" infrastructure。

Derivatives as a proportion of total trade volume increased from less than 10 per cent in 2017 to about 90 per cent in March 2026 — derivatives have taken full ownership of the pricing power of the encrypted market:

DOING NOTHING TO KILL BTC. DOING NOTHING HAS TRANSFORMED THE BTC FROM A $10 BILLION SPECULATION TO A $2 TRILLION ASSET CLASS。

2020-2021 — DeFi Summer: More than mere narrative, it is in itself the evolution of mechanisms

The BTC and ETH options markets matured rapidly in 2020-2021 (predominantly Deribit). This is the "CBOE Time of 1973" of the encrypted market -- institutions that can not only be empty, but can also be accurately hedged and structured. The dimensions of the strategy have been expanded from two dimensions to higher dimensions。

In addition, DeFi Summer has been classified as a "dissemination" -- just like the NFT hot tide, the meta-cosmic concept, just another windfall. But it was a fundamental error. DeFi Summer is essentially not a narrative, but a structural leap in the trading mechanism。

AMM rewrites the bottom logic of the transaction. Before Uniswap, the transaction required a book of orders, a marketer and a centralized arrangement. AMM reversed all this — anyone could form a mobility pool in two currencies, anyone could trade instantaneously, without the need for a counter-party to put up a bill and without anyone's permission. This is not narrative. This is a paradigm shift in the trading infrastructure. It allowed thousands of long tails that had previously been out of the market for the first time to gain liquidity。

Loan agreements create chain leverage and circular strategies. Aave, Compund allows the user to mortgage the asset and lend another asset - essentially the chain of margin trafficking. And more importantly, it gave rise to "revolving loans": mortgages on ETH to borrow stabilization coins, buy more ETH in stable coins, then mortgages... This strategy has been called leverage in traditional finance, and in DeFi it has been packaged as "yeeld farming," but at the bottom, the same logic — it is a new game approach that allows participants to participate in markets with more dimensions。

PORTFOLIO ALLOWS INNOVATION TO BE INDEXED. AMM + LENDING + LIQUID MINING + CROSS-ACCORDING ARBITRAGE – THESE COMBINATIONS OF "MONEY IS HIGH" CREATE STRATEGIC SPACE THAT NEVER EXISTED IN TRADITIONAL FINANCE. EACH NEW COMBINATION IS A NEW FORM OF PARTICIPATION, WITH NEW FUNDING AND NEW USERS。

So the Super Cows in 2020-2021 are not a combination of two factors, but three: the BTC and ETH lasting contracts/opportunities give access to institutions, DeFi's AMM and the loan agreement make a qualitative difference to the chain-based trading mechanisms, and narratives are merely the evolutionary surface packaging of these two mechanisms。

Once again, the same rule has been tested: every evolution of the trading mechanism has led to the next round of prosperity。

2021-2023 — Long-lasting expansion of the Shancocoin

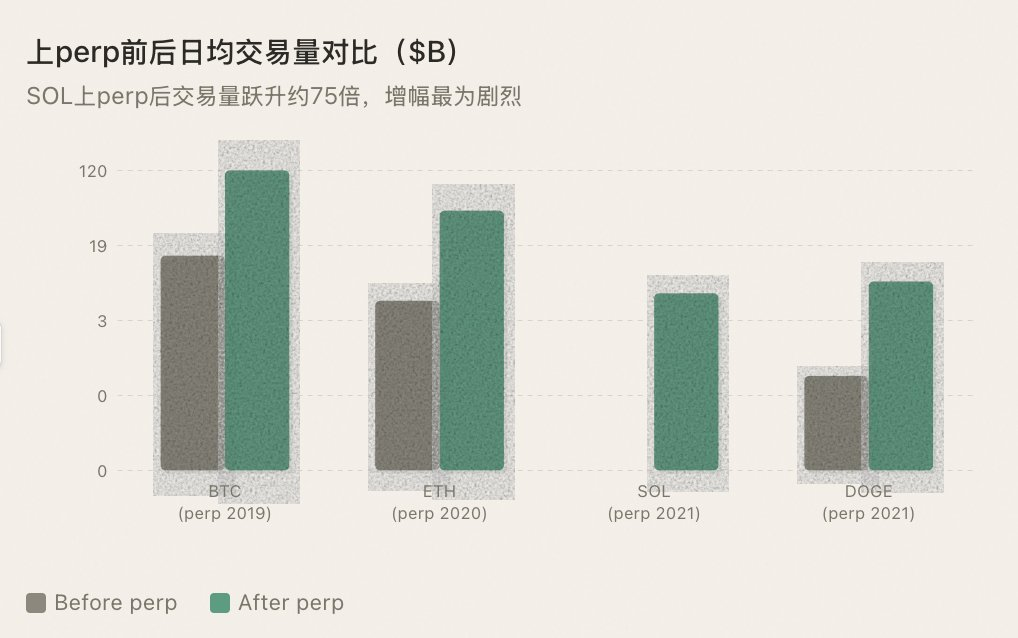

Binance began to renew the contract for a growing number of quid. Every new perp currency, there is a spiral of transactions -- not because "upper" is good news, but because the introduction of empty tools allows more strategic types of money to participate. Quantitative funds can be marketed, hedge funds can be hedged and trend traders can be empty. The diversity of participants is directly equal to the depth of mobility。

The pattern continues: the BTC has a perp coming to Bullsville, ETH, and SOL has experienced a liquidity leap in each of the perp coins。

2023-2025 — the moment when the rule fails

Then, if there is no accident, there will be an accident. Like an idolic play, there will be a “block” around the corner, but only a barrier。

In late 2023 to Q3 in 2025, Binance renewed the contract at an unprecedented rate. Almost every week, new perp deals are on the line — from mainstream public chain tokens to AI concept coins, from GameFi to Meme, and even projects with a market value of only tens of millions of dollars have been awarded sustainable contracts。

On the face of it, this is a continuation of historical patterns: providing more assets with empty tools, creating more liquidity and attracting more participants. And objectively, these perp do create liquidity in a vacuum — a project with billions of FDVs but a market value of tens of millions in real circulation, which simply cannot afford a decent trade depth on the spot market. The use of commercial stability coins for the renewal of contracts provides a bilateral offer, which amounts to an injection of synthetic liquidity into these thin paper-like markets。

But this time, the pattern didn't work。

the problem is the disconnect between "mobility" and "confidence". mobility is created on the premise that people are willing to play. and the reality of 2024-2025 is that everyone is afraid. the market is now looking at the top as the end point, the exit signal, the news deal。

The family is afraid. After the FTX thunderstorm, the Luna crash, and numerous Rug Pulls, the diaspora's trust in the banknote fell to the ice point. More deadly is the fact that a large number of newer perp projects have deformed token economics: billions of FDVs combined with extremely low circulation, which means that in the future there will be natural coins waiting to be unlocked. It's not stupid -- you make me empty tools, but it's a designed chronic blood pump. Why should I be involved? I don't want to touch it, either。

the dealer's scared. going online means that their control is exposed to empty fire. previously, in the net spot market, the dealer was able to pull the goods out at low cost, without any threat to him. with a perp, each pull could lead to a large number of blanks and the cost of maintaining prices rose sharply. many of the project parties respond not by accepting the game, but by lying flat — without pulling the plate, allowing the price to decline naturally and selling the unlocked tokens slowly. without the pull project, there would be no profit-making effect; without the profit-making effect, there would be no trade。

the market is scared. that is the key. there is a high risk of resuscitating contracts for a project with a daily average spot trade volume of hundreds of thousands of dollars. liquidity is too thin, prices are easily manipulated, and stock risk (inventory risk) for market traders is difficult to hedge. once there is an extreme situation, the list that the market merchants get won't come out. after a number of detours, marketers began tightening prices, widening the price differential, lowering depth and even withdrawing directly. without the perp that the market would like to do, mobility is an empty shell。

Worse still, those that are still in operation have been turned into private casinos。

bankers can almost do whatever they want in the perp market. the pull drive does not require much money — spot control raises prices, and perp collects a wave of empty-headed warehouse money. it is also easy to smash — to open the perp first, then to break the plate and profit from it. repeatedly, perp leverage has become a tool for the dealer to magnify the proceeds, rather than a weapon for the risk of sprinting。

this game is far more destructive than controls on the spot market. the dealers in the spot lie to the side of the switch, and the dealers in the perp harvest the whole empty side — no matter how much you do or how empty, your deposit is his profit as long as you stand opposite the dealer. experienced traders are afraid to touch these mountaintops, and inexperienced traders come in and are harvested repeatedly and leave forever。

in the first place, empty tools should be the power of the dealer. but on a very mobile hilltop, the relationship is the reverse: empty tools become another knife in the hands of the dealer. it is not just the ecology of a single currency that destroys trust in the whole encrypted market. every trader who has been targeted and blown up on a hilltop is a user of the permanent loss of the encryption market。

Paradoxically, Binance has become more and more perp, but the trade volume and dynamism of the Yamashita currency market is shrinking。

What does that mean? The mechanism for the renewal of the contract has been upgraded to the ceiling. Perp is a heavy-duty machine that requires commercialization, prophecies, financial rates, centralization of approvals to operate. BTC and ETH can afford the machine, but thousands of long-tailed coins can't - it's on, but it's out of gas. And the machines, which are barely open, become bankers' ATMs。

iv. Why is the contract for eternity doomed to failure

The results of the 2023-2025 experiment are explained at the institutional level。

The flow of death. Perp needs to make a bilateral offer for a stable currency. Who's willing to market anonymous projects with hundreds of thousands of dollars in Japanese transactions? There is no mobility, there are no traders, and there are no traders. The off-the-shelf leverage does not need to build a derivative market from zero — borrow it in tokens and sell it in existing DEX pools. The loan agreement provides supply and AMM provides enforcement, decoupling the two。

two prices, two worlds. the perp and the spot are two separate pools, and the pool is thin when a trade can pull the price gap to the wrong level. you think you're doing this empty project, and you're actually gambling in a parallel universe detached from the spot. there is only one market, and there is no breakout。

funding rates are manipulated. the dealer pushes up the perp price to create extreme capital rates and is drained every few hours, and in the right direction it will be worn to death. worse still, the dealer operates both the spot and the perp — the spot pull, and the perp eats the empty silo. the spot leverage is only the interest rate of the borrowing, determined by supply and demand, and is not distorted by the ratio。

synthetic positions do not produce real sales pressure. that is the most critical point. it's empty on the perp, and there won't be any bills on the spot market. the dealer turned his right hand on the spot, and perp threatened him with nothing. shorthand leverage is the sale of real coins on the spot — real pressure is a direct effect on the price, and the dealer has to pay for real money to keep the price high。

Check + the prophecy machine. Perp needs exchange approval and a reliable predictor machine, both in small currencies. No approval is required for a chain loan, and the settlement price depends on the AMM real-time price。

The terminus contract is a heavy infrastructure with operating costs higher than the value it can generate for long-term assets. What's needed is the lightest way to make it empty - borrow it, sell it and buy it back. That's where the spot-lender lending is empty。

V. Fear is empty, or fear is no price discovery

From Amsterdam in 1609 to Wall Street in the 1860s to Crypto Twitter in 2024, the fear of doing nothing has never changed. "Doing empty will smash." "Doing empty is malicious attack." "doing nothing to make the market crash. For 400 years, the wording remained almost unchanged。

But 400 years of history have proved the same thing repeatedly: the cost of fear is far greater than the cost of doing nothing。

When criticism is not allowed, praise will no longer be meaningful. When empty is not allowed, doing more will be meaningless。

Because in a market that can only be bought, prices reflect only half of the optimism. The pessimistic half of the message — suspicion, space, fraud — was forcibly silenced. All we can do is say "no" and no one can say "no"。

Such prices are distorted, fragile and unsustainable. It's not a price discovery. It's a price illusion。

The most basic respect for finding prices is when you can do as much as you can。

And with real prices, the market is likely to last. Institutions come because prices are credible; marketers come because they can do it in both directions; long-term investors come because current prices have been tested emptyly, not by the dealer。

Conversely, markets without price discovery depend on narratives. Each round of heat used to be a chicken hair, and then the next narrative, attracted another wave of people to pick up the wheel. It's always this cycle. It can never accumulate。

The biggest tragedy in the market for the Yamamoto currency is not "too many dealers", but not even the basic conditions for price discovery. What's the long-term value

Six, emptying is not a tool to see, it's a catalyst for cattle

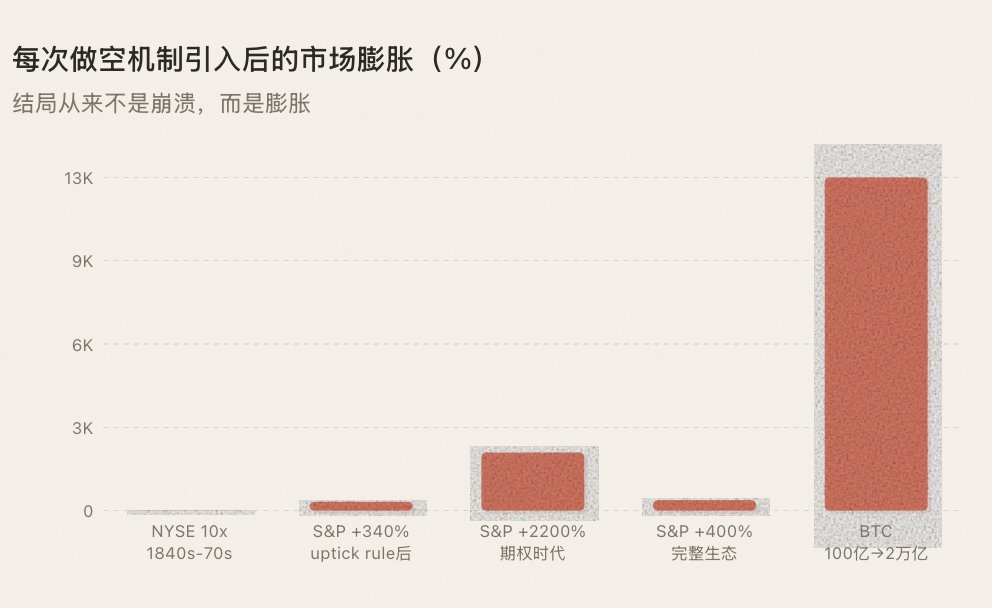

The most anti-intuitive pattern in history: every introduction of empty mechanisms does not, in the long run, reduce prices, but rather raise them。

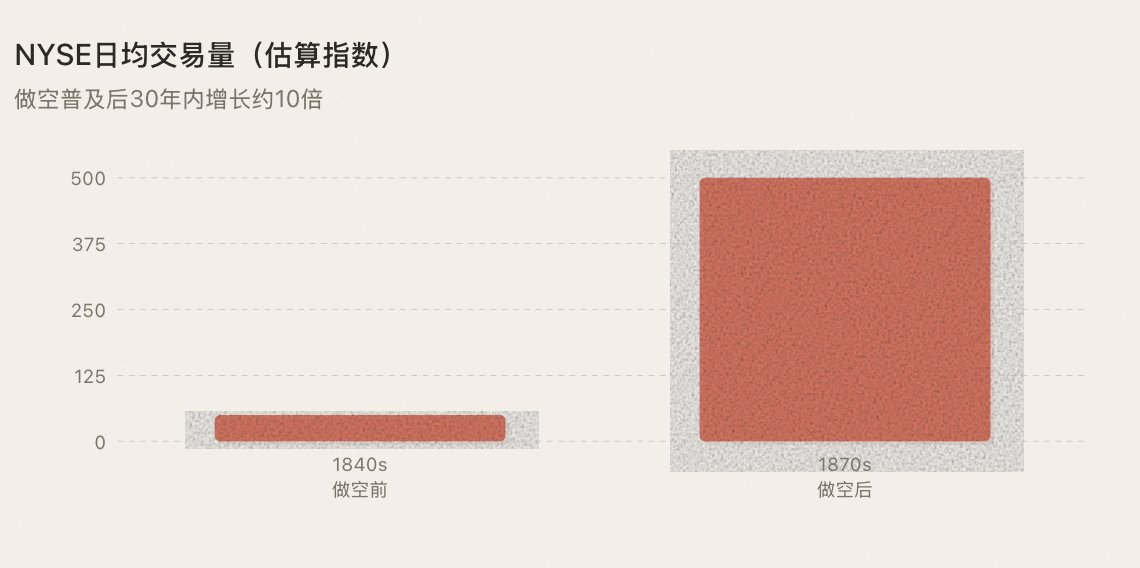

In the 1960s, when the air had spread, NYSE transactions had increased tenfold over a decade, and Wall Street had moved from a small circle to a real capital market. After the legalization of utick rule in 1938, institutional funds entered the field on a large scale, S& P 500 rose by 340 per cent over the next 30 years. After the creation of the CBOE option in 1973, the number of options traded increased by 10,000 times in 50 years, and the United States stock expanded for decades. When the BTC contract came online in 2019, the BTC volatility dropped from 150 per cent to 50 per cent, while the market value expanded from $10 billion to $2 trillion。

In each case, the outcome was not market collapse, but market expansion. There are three reasons for this:

Emptyness creates liquidity - every empty bill is a bill of sale plus the inevitable future purchase (refill) and the more active the empty is。

Doing nothing to attract new participants — doing business as market merchants, quantifying funds, hedge funds, arbitragers — is not here to crash, but to provide mobility, which is the oxygen of the cattle market。

Building confidence in the air — prices that have been tested by the air are credible prices that attract real money, which drives real growth。

The full gaming tool is not destroying confidence, but building confidence。

VII. The next round of cattle markets

From Amsterdam in 1609 to the encryption market in 2025, the four-hundred-year financial history has repeatedly tested the same pattern: there is a mechanism to evolve and then prosperity. This order cannot be reversed。

The market is now stuck in a death spiral: it can only be a model of multiplicity and less and less and less and less and less and less and less and less and less and less liquid. Why can't you buy money and open it

An enduring contract would not solve the problem — the experiment of 2023-2025 had proved itself. Perp is a heavy infrastructure that cannot be supported by a long-tail money. The "upperp" itself became another narrative trigger, like Alpha on the "on-the-shelf" and became the source of news transactions, away from the transaction and the game itself. The trading tool was intended to serve the transaction, but now it's the object of the transaction. - For long-tailed assets, perp is structurally the wrong tool。

The right path is on the chain."The original spot leverage is empty."- Lending through over-collateralization, borrowing in real currency, selling in spot markets, generating real sales pressure and participating in real price discovery. There is no need for marketers to build markets from zero, no need for prophecies to maintain anchors, no need for flat rates and no need for approval。

This is in line with the path of every empty mechanism in history. The 1609 Le Maire job was not approved by the Amsterdam Exchange. The 1850 Wall Street coupons were not designed by NYSE. They were created by market participants on their own initiative — with tools and rules. What the SEC did in 1938 was not create a vacuum of inventions, but rather a framework of rules for almost 100 years of empty behaviour。

The same path is followed by empty agreements on the chain。

When this happens — when a mountain coin is no longer just a one-way game of “buy-and-roll” but rather a multi-empty exchange of real-gold and real-gold faces on the spot market — the quality of the market changes fundamentally. Liquidity will come back, participants will come back, funds will come back. Not because of new stories, but because of new ways to play。

If the historical pattern continues — and we have no reason to believe that it will not — then the starting point for the next round of Yamamoto City will not be a new narrative, a celebrity shout, a one-time cut-off。

It would be an infrastructure upgrade: it would give thousands of long-tailed machete coins an empty tool in the chain — this is where the money circles are priced。

THIS TIME, IT IS NOT THE BTC LIQUIDITY SPILL THAT GOES TO THE MOUNTAINS, BUT RATHER THE REVERSE。

Concluding remarks

In 1609, the Government of the Netherlands banned empty space and Le Maire was publicly condemned. In the 1860s, the United States Congress called the empty head an enemy of the State. After the collapse of 1929, the public demanded the complete elimination of the void. In 2024, "doing nothing" in the encrypted community was still a dirty word。

For 400 years, the fear of doing nothing has never changed。

But 400 years of history has proved the same thing: Each time such fears were overcome and empty rights introduced into markets, markets did not collapse — markets swelled. Amsterdam has become a global financial centre. Wall Street was transformed from a tree to a trillion-dollar capital market. Binance became the universe. BTC went from $10 billion to $2 trillion。

And now, thousands of them are locked in a cage that can only do more. There is no price discovery without empty space, no trust without price discovery and no lasting prosperity without trust. The whole market has deteriorated into a single game of gambling "as expected" — fewer people making money, fewer people participating, more quiet. And those that barely have a lasting contract, emptying the tools becomes a new cutter for the dealer, accelerating the loss of market confidence。

When criticism is not allowed, praise will no longer be meaningful. When empty is not allowed — or when empty is the prerogative of the dealer — the price will never be true。

Worse than empty fear, a market without price discovery。

Cow City never waits. It's an evolutionary mechanism. And the core of each mechanism's evolution, from 1609 to today, is the same thing —

Give the market back the right to sellI don't know。

"you can short it@heyibinanceI'm not sure