Putting the market itself on the chain: Canton Network is quietly becoming the new bottom of institutional finance

INTEGRATION OF DATA VISIBILITY L1, SWEEPING WALL STREET。

Original Odaily Daily Planet (@OdailyChina)

author

I. A proposal approved for three days

On March 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, 20, According to The BlockOnly three days later, the proposal was approved and Visa formally became the Canton super certifier with a maximum weight of 10 (Super Validator Weight 10)。This is also the first time that Visa has submitted a proposal for block chain governance。

In the encryption circle, this may seem to be another entry into traditional finance. But if you have sufficient knowledge of the legal and compliance processes within traditional institutions such as Visa, you will find that the three-day approval is quite unusual. The submission of this document by the Visa compliance team must have been premised on caution and seriousness in the traditional financial world, with the highest weights, indicating that negotiations and due diligence have been completed before that date. The proposal was seen by the publicIt should be the result of months of cooperation between traditional finance and the encrypted world。

In his statement, Rubial Birwadker, Director of Global Growth Products and Strategic Cooperation, Visa, said: “Many banks believe that the lack of privacy is the biggest obstacle to moving meaningful operations into chains. By acting as a super certifier for Canton Network, we have brought Visa-level trust, governance and operating norms into this privacy-protected block chain infrastructure, allowing regulated financial institutions to move payments to the chain without disrupting existing operations.”

As can be seen, Visa ' s entry is an endorsement of a well-functioning institutional network, not a starting point。

Since 2017, there has been a high-profile announcement of “exploration block chains” by a group of traditional financial institutions in each turn, which has resulted in very little real business. On this occasion, Visa chose to enter the governance layers of the block chain with voting rights and participation in infrastructure decision-making. In his statement, Eric Saraniecki, the web strategy manager of Digital Asset, a co-founder of Canton Network, said: “Visa's addition confirms that the technology has moved from the experimental phase to the production readiness phase.”

I'm not sure what I'm talking aboutOdaily Daily interviewed Canton Network's team. What made this collaboration happen? And what made Canton, the long-deep project, chosen

II. Not more assets, but the market itself

To understand why Canton attracts Visa, we needLook at the core difference between Canton and the other chains。

The problem with the Ether and Solana is how to get more people involvedHow do we put more assets in the chainI don't know. Canton's problem is:How do financial institutions operate normally on the chainI don't know. It sounds differentBut when it comes to design, the trade-off becomes almost the opposite。

The overall transparency of the Ether Workshop is an advantage for the diaspora and an obstacle for institutions。To give a specific example, the bank ' s foreign exchange transaction department, if every dollar and euro transaction is visible in real time, will soon be able to adjust the offer against this information and the bank ' s transaction costs will increase significantly. If the marketer is fully open to hold and hedge operations, the competitors will be able to move directly in the opposite direction and run out of profit space. Repurchase agreements between the agencies concern the financial position of both parties and the size of the collateral, which, if released, poses a risk to the liquidity management of the institution as a whole. These restrictions are not directly related to regulation and are determined by basic business logic。

Even if there is no linkage between the address and the real name, transparent transactions along the chain change the logic of the entire secondary market. No traditional financial institutions want their own transactions to be sniveled, so design like Taifung and Hyperliquid is not the best option for large institutions。

Canton's approach was to fit into the designData visibility control。

THIS IS DONE BY PLACING SELECTIVE DISCLOSURE OF THE DATA ITSELF INTO THE PROTOCOL LAYER AS A PRIMARY DESIGN FOR L1, RATHER THAN BY PATCHING IT WITH A TOP APPLICATION. SPECIFICALLY, ONLY DIRECT PARTICIPANTS IN THE TRANSACTION CAN SEE THE TRANSACTION DETAILS AND THE NETWORK COMPLETES THE VALIDATION WITHOUT EXPOSING ANY SENSITIVE DATA. THE TWO BANKS COULD SETTLE ACROSS BORDERS ON THE SAME SHARED INFRASTRUCTURE, A TRANSACTION THAT WAS TOTALLY INVISIBLE TO ALL PARTIES INVOLVED。Competing parties can interact on the same network and their positions and strategies will not leak。

We also asked for relevant technical details, as Canton put it: “Canton separates the coordination layer (shared across the network) from the data visibility (only for participants), by separating the enforcement environment from selective synchronization. This allows agencies to trade safely, and there can be interaction between competitors without exposing each other to their own silos or tactics. It is a mechanism that allows real markets, not assets, to function in the chain.”

Canton Network tells us that this design logic sums up: data visibility control is the basis, not the additional function。

So, why does the Canton's certifier list look like an old money partyGoldman Sachs, Morgan Chase, BNP Paris, Citi, Bank of America, DTCC, NASDAQ, Broadridge, Tradeweb..These institutions come in because the infrastructure allows them to recreate the success of traditional finance on them, so liquidity is slowly flowing。

Canton's super-certifying list

I'm from Wall Street

Canton was created by Digital Assembly Holdings, created by Blythe Masters in 2014. Blythe Masters, once the star executive of Morgan Chase, was one of the major pioneers in the CDS field, with a deep human and industry endorsement on Wall Street. This company has not been a bulk-oriented block chain product since its first day, and its target clients are financial institutions with real balance sheets, strictly regulated and operating within the legal framework。

In terms of origin, we ask an acute question:We saw Canton in 2023. Why didn't he officially go online this year

Canton's answer is slow work。

Wall Street's origins determine the pace of the whole project. In interviews, Canton admitted that it took longer than the other L1s to get to this point, because it started with the regulated financial system, the building of institutional trust, and how to truly access markets with real operations。

This rhythm and the mainstream narrative of Web3 are completely opposite. Most of the public chains seek fast-line, fast-painted ecology, fast-manufacturing heat, and TGE spreads, and then "the team is not really clear." Canton's path is one step at a time: take the DTCC, then Goldman Sachs, then Morgan Chase, then Visa, by their endorsement, into actual business。

The year 2026 was a turning point, not because of the project's promotion itself, nor because the encryption of the world, the bear market, started shuffles, but because, for the first time ever, infrastructure actually met the institutional requirements: there were real balance sheet activities operating on it. That's why it's the best time to focus on Canton Network。

"So how much business has been introduced?"We'll keep asking questions。

IV. CENTON'S STRENGTHENING ACTIVITIES

Canton's current data are different across the block chain industry, and the nature behind these figures and most public chains are very different. Currently, Canton Network has more than $9 trillion per month in processing, hundreds of thousands of transactions per day, and the number of ecological participants has increased in number over the past three years. These figures correspond to traditional financial operations: tokenization buy-backs, national debt settlement, cross-institutional mortgage transfers. These are not brushes, but are real operations that occur on an institutional balance sheet。

We also asked which products are the mainstream of the current chain. Currently, there are a few flagship products:

JPM Coin:In January 2026, the Kinexys department under Morgan Chase announced the deployment of JPM Coin to Canton Network. Unlike the USDT, USDC, JPM Coin is a deposit token representing a direct claim on Morgan Chase deposits and following the existing banking regulatory framework. By way of example, the two agencies settled a cross-border transaction with JPM Coin on Canton, which was no different from what they did in the traditional system, except that the settlement was much faster and the operation time was no longer limited to working days. Kinexys currently has a daily average of between $2 billion and $3 billion, with a cumulative total of more than $1.5 trillion since 2019, which is about to run on Canton。

DTCC US TREASURY DEBT DECORATE:In December 2025, the United States Securities Regulatory Agency, DTCC, announced that, in cooperation with Digital Asset, it was planning to monetize a portion of the United States Treasury debt that was held in trust on Canton, with the goal of rolling out the first edition of the controlled production environment in the first half of 2026 and expanding it to market demand. DTCC is also co-chair of the Canton Foundation and is directly involved in network governance。

DTCC HANDLES SECURITIES TRANSACTIONS WORTH MORE THAN $200 TRILLION A YEAR AND IS AT THE HEART OF THE ENTIRE UNITED STATES CAPITAL MARKET SETTLEMENT SYSTEM. IN A MORE INTUITIVE ANALOGY, THE DTCC'S POSITION IN TRADITIONAL FINANCE IS A BIT LIKE THAT OF THE PEOPLE'S BANK; NO ONE CAN SAVE MONEY IN IT, BUT EVERYONE'S STOCK AND BOND TRANSACTIONS HAVE TO GO THROUGH ITS BACK OFFICE. THE TRADITIONAL BUY-BACK MARKET CAN ONLY OPERATE ON WORKING DAYS AND WAIT UNTIL FRIDAY AFTERNOONHowever, up-to-date buy-back transactions in Canton can operate 24 hours a day, with a chain of United States Treasury bonds as collateral, achieving real-time finance across institutions, across time zones and covering weekends。

So what will Visa do on Canton

One of the core objectives described by Canton in the interview was atomized settlement:The buyer ' s payment and the seller ' s delivery of the assets were completed in the same operation without having to go in two steps or rely on an intermediary to connect。For example, an institution currently buys bonds, transfers of assets and cash settlements are often two separate processes, with time lags, counterparty risks and the cost of manual reconciliation. What Canton wants to do is that both things happen at the same time, lock, no time difference. To achieve this goal, capital market and payment infrastructure must be linked simultaneously. Canton has a fairly solid layout on the capital market side, and Visa's addition has given the payment side a real institutional anchor。

In addition to this, it includes real-time cross-border capital flows, the embedding of programmable logic into block chains such as financial transactions。

According to Canton, 2026 is the first time that infrastructure actually meets institutional requirements, so institutions like Visa have chosen to intervene in block chain infrastructure now。

Other examples of running already

It is the most mature scenario at present。Repo, the most common short-term financing instrument among financial institutions, is agency A, which sells bonds to agency B in exchange for cash, while agreeing to buy them back in a few days. Traditionally, this process can be done only during working days and there are delays in the receipt of funds. The monetization buy-back on Canton has been made available 24 hours and settled immediately, and several head offices have completed a real buy-back transaction on Canton across institutions covering weekends。

Mortgage mobilizationIt is also a scene with real needs. Large financial institutions are often required to move collateral from one account or institution to another, for example, bonds in A to B to meet the requirements of a deposit for a derivative transaction. Traditionally, this process takes days, during which assets are locked and not available for other purposes. Canton’s settlement model allows the process to be completed in near real time。

Digital bond issuesIt's another area where Canton dominates. In the interview, Canton mentioned that it currently has more than half of the global digital bond issuing market. The reason for this is that Canton can provide complete delivery for payments (DvP), full life cycle management and multi-party coordination of bonds, which can be closed in the chain from issuance to settlement, rather than simply monetizing assets, and then relying on the bottom of the chain。

Stabilization currency settlementIt was Visa ' s accession that was moving in an accelerated direction, with the goal that stable currency payments between institutions could be made on the same compliance infrastructure with data visibility control, rather than bypassing the public chain。

SIMPLY PUT, IT'S NOT ABOUT RWA, BUT IT'S ALL ABOUT RWA NEEDS。

In his interview, Canton gave an overview of the road map that follows:In the medium term, corporate debt, private credit and trade finance will keep up; in the longer term, equities will be on the same path。From the existing examples to the road map, the logic is consistent, with the more mobile the more mature the regulatory framework is, the sooner it moves。

WHAT DOES CC MEAN

FOR THE WIDER MARKET PARTICIPANTS, CC, WHAT THIS TOKEN IS, IS A MATTER OF INDISSOCIABILITY。

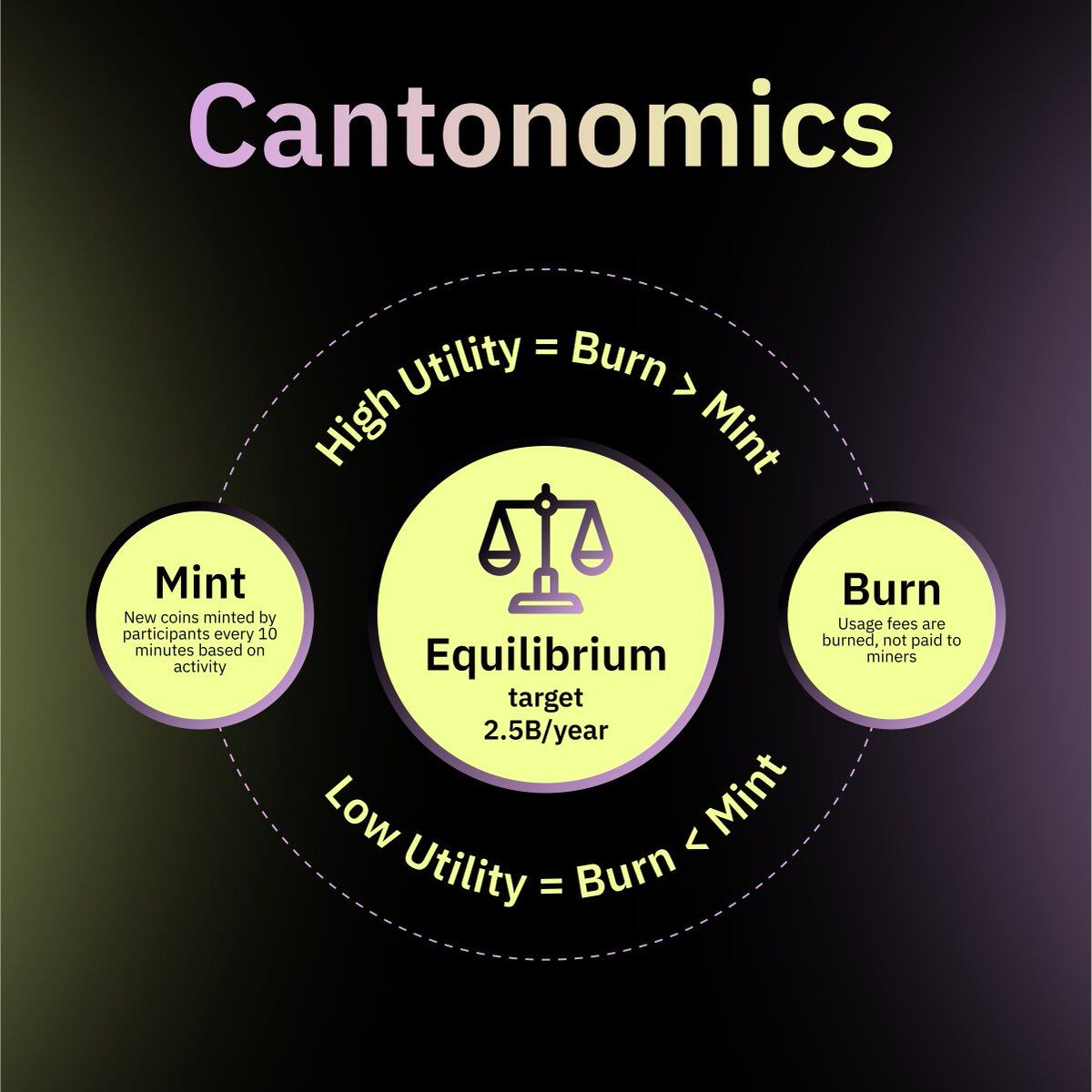

Canton's profile in interviews is more direct:CC IS A “NETWORK-EFFICIENT ASSET” WHOSE VALUE ANCHORS ARE SCHEDULED FOR THE REAL VOLUME OF FINANCIAL ACTIVITY ON THE NETWORK。

It means that the demand comes from actual use, and the larger the transaction on Canton, the more the network consumes the CC. Long-term drivers of tokens include institutional transaction flows, stabilization of currency settlement scales, total chain assets, and interoperability between Canton and other networks。

CC has a rather rare set in the Web3 circle on token allocation:ZERO PRE-DRILLING, ZERO TEAM ALLOCATION, ZERO VC SHAREAll tokens have access to markets in a fair manner. For institutional participants, this set-up reduces the concern that the rules are transparent and reciprocal to all participants "someone with super-cost chips and ready to flee in secondary markets"。

For ordinary market participants, Canton exists more as a back-office infrastructure and is more likely to be reached by ordinary people through exchanges, wallets or financial platforms than directly interacting with agreements. The improvements that it brings, such as faster settlement, tighter trade price differentials, and financial products that offer better conditions because of lower operating costs, are gradually transmitted to end-users through product layers rather than in ways that users can sense directly。

VI. Next steps

Canton's target of 3 to 5 years in the interview is not measured by the value of a chain TVL or a token. In the light of the specific objectives set out by Canton: to stabilize the currency as a standard means of inter-agency settlement, just as SWIFT wire transfers are the current standard; to operate directly in the chain by major financial institutions, such as banks' loans, deposits, bond issues and product packaging; and to eliminate the need for cross-border capital to experience traditional systems Days of settlement cycle, moving at near real-time speed; multiple asset classes complete original distribution and settlement on Canton instead of distribution under the chain and manually synchronized information into the chain。

Canton describes himself in this state as "invisible":At that point, Canton was just one of the bottom-of-the-board agreements driving global finance, like today’s TCP/IP on the Internet, or SWIFT on cross-border remittances, using people who didn’t know it existed, but couldn’t turn it around。

Of course it's a long road. Regulation is highly fragmented across jurisdictions, in a way that is completely different from compliance in Europe and Asia; existing legacy systems are difficult to integrate and banks cannot migrate overnight after decades of core systems; interoperability between different block-chain networks is an outstanding technical issue; and inter-agency coordination on the same set of infrastructure involves complex profit-making. The Canton team didn't shy away from the interviewTechnological bottlenecks are no longer the biggest problem, but how to really push them across the globe。

As can be seen, changes in the financial infrastructure have never taken place overnight. SWIFT was established in 1973, and it took almost two decades to become the true standard for cross-border settlement. People use it now, and they don't remember how it came. Canton's position now is probably the "no one knows what it's going to become." But for something that really wants to be an infrastructure, being forgotten may be the way it should be。