Star chains make money, AI burns money, $1.7 trillion SpaceX, buy it

THIS PRICING LOGIC IS POSSIBLE ONLY IF THE MARKET IS CONVINCED THAT AI, ORBITAL DATA CENTRES, NEXT-GENERATION SATELLITE NETWORKS AND LONGER-TERM SPACE INFRASTRUCTURE CAN BE A REAL SOURCE OF INCOME.

TL;DR

- SpaceX plans to issue equities at $135 per share and raise approximately $75 billion, with a corresponding valuation of about $175 trillion. The dispute is not about the company ' s technical strength, but about the early inclusion of AI, orbital data centres and Mars vision。

- THE MARKET FUD COMES MAINLY FROM THREE POINTS: VALUATIONS ARE WELL ABOVE THE CURRENT INCOME SCALE, CHAINS OF PROFITS ARE SUBSIDIZING HIGH-INPUT AI OPERATIONS, AND ASSOCIATED FINANCING AND INTERNAL M & AS ALLOW RISK TO GRADUALLY CONVERGE TO THE SAME BALANCE SHEET。

- ASSOCIATED OBJECT: SPCX (TO BE LISTED)

SpaceX is preparing an IPO that may be rewriting capital market records。

The company plans to issue approximately $556 million in equities at $135 per share, raise approximately $75 billion, corresponding to an overall valuation of about $175 trillion. If the listing is successfully completed, it will be one of the largest IPOs in history, and will allow SpaceX to enter the top United States market value companies on its first day on the market。

Such market concerns are not difficult to understand, given the performance of SpaceX over the past two decades。

The company ' s reliance on recyclable rockets has significantly reduced commercial launch costs, created the world ' s largest satellite Internet network and allowed Starlink to move from a technological experiment to a real source of income and profits. In the field of global commercial space, SpaceX has almost no real comparable company。

BUT THE CLOSER IPO GETS TO THE GROUND, THE MORE QUESTIONS IN THE MARKET GET。

These challenges do not mean that investors deny SpaceX ' s technical capabilities, nor do they mean that the market considers the chain to be worthless. What really triggered the FUD is that companies want the open market to accept a very radical pricing logic once and for all:

Today's investors need to pay not only for rocket and satellite networks, but also for AI infrastructure, orbital data centres, the next generation of Starship and the longer-term space economy。

The market is not worried that SpaceX has no future, but that the future has been priced too much。

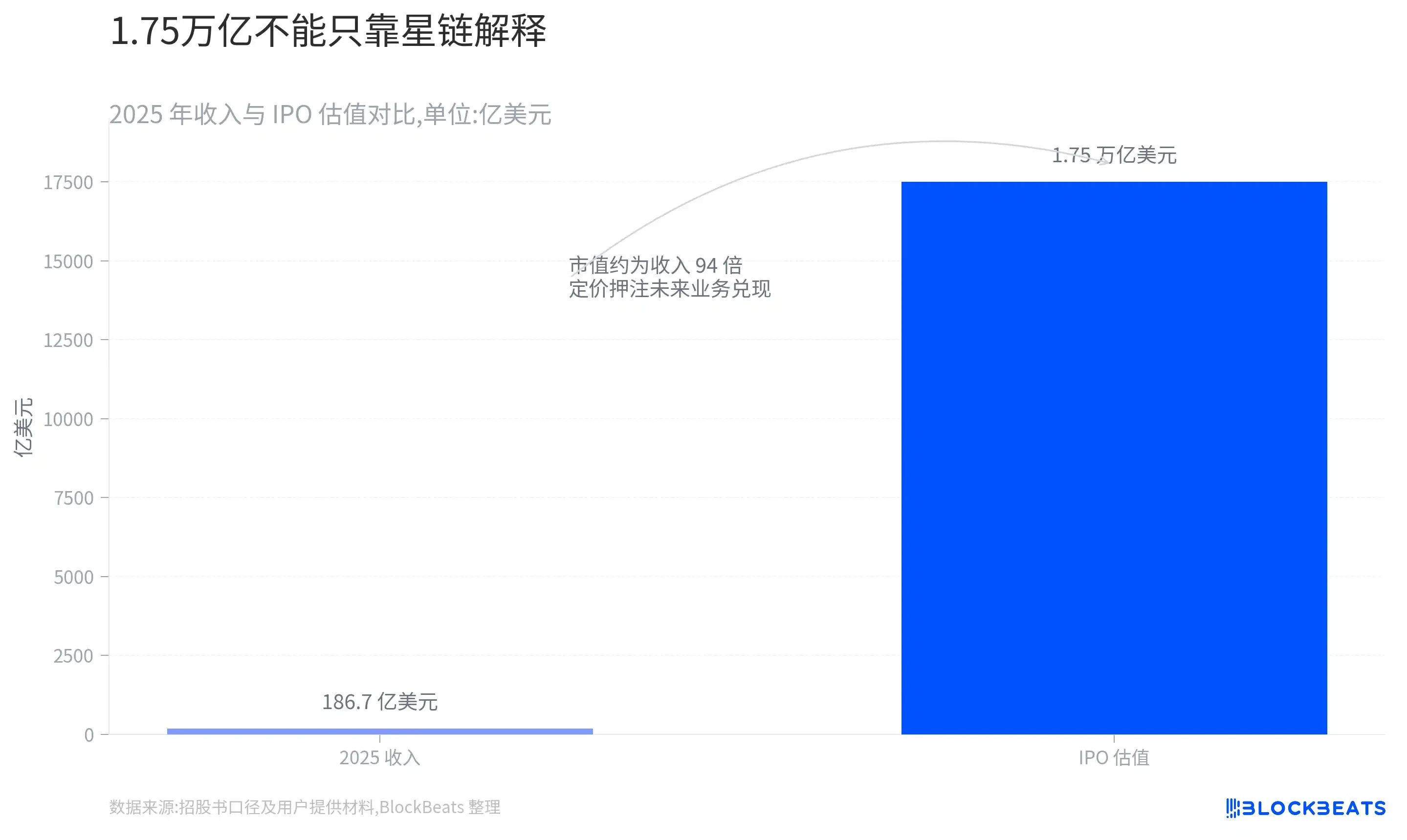

1.75 trillion dollars in valuation, which cannot be explained by a chain of stars alone

SpaceX this time IPO is the most direct dispute from valuation。

In 2025, corporate revenues amounted to approximately $18.87 billion, an increase of 33 per cent over the same period, but the net loss still amounted to about $4.94 billion. Based on the $175 trillion valuation, SpaceX ' s market value was close to 94 times the previous year ' s income。

This multiple does not mean that the company must be overestimated. SpaceX has a very scarce infrastructure, and operational structures are difficult to compare with traditional space, communications or technology companies。

The problem is that when the valuation reaches 1.75 trillion dollars, it is already difficult to fully explain market pricing on the basis of existing operations alone。

If investors see SpaceX only as a rocket launcher and satellite Internet company, the current valuation is very radical; this pricing logic is possible only if the market is convinced that AI, orbital data centres, next-generation satellite networks and longer-term space infrastructure can be a real source of income。

And that's why the grand vision in SpaceX's book of equity is the starting point for market disputes。

When the valuation of a company relies on business that has not yet developed a mature business model, the market naturally increases the risk discount。

IT'S THE CHAIN, IT'S AI

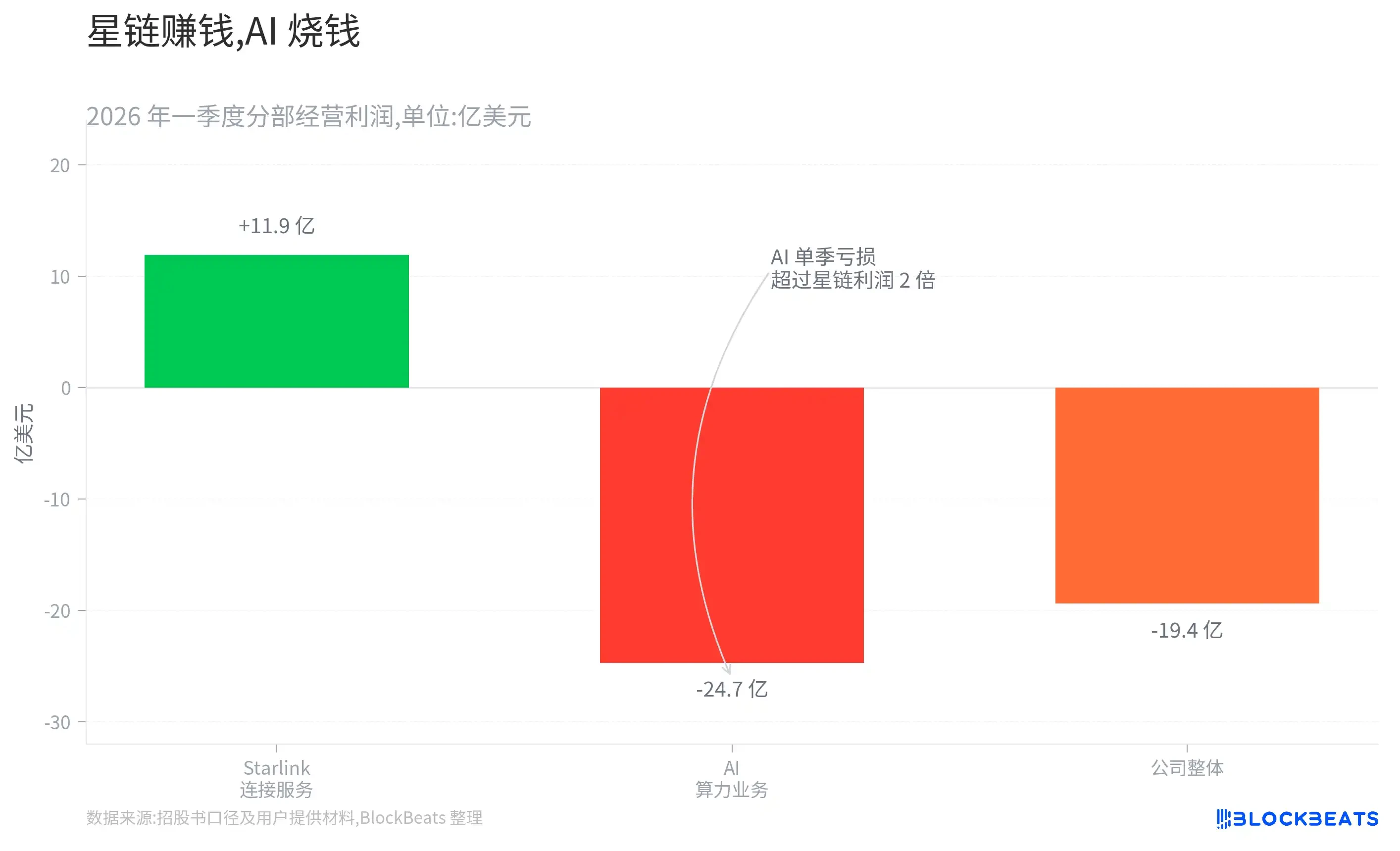

If Mars, orbital data centres and deep space transport were to be put down temporarily, SpaceX ' s current financial structure would be quite clear。

In the first quarter of the year, companies realized revenues of approximately $4.69 billion, but operating losses of about $1.94 billion. Of the three main business blocks, only the Starlink-based connectivity service sector was profitable, with a single-quarter operating profit of approximately $1.19 billion. AI earned about $818 million in revenue, while operating losses amounted to about $2.47 billion。

At the same time, SpaceX ' s capital expenditures are accelerating significantly. The company ' s capital expenditure in the first quarter was approximately $10.1 billion, of which 76 per cent went to AI-related operations。

This means that SpaceX is still the most stable source of profits for the time being, while the company’s most radical investment is going to AI。

THE MODEL IS NOT UNREASONABLE. AI INFRASTRUCTURE IS ITSELF AN INDUSTRY THAT REQUIRES SIGNIFICANT INVESTMENT IN ADVANCE, AND DATA CENTRES, ELECTRICITY, CHIPS AND NETWORK EQUIPMENT CANNOT BE RECOVERED IN A SHORT TIME。

But the real concern of the market is:

Is the profits of the chain being invested in a new business that requires constant burning of money but with a return cycle that is still unclear

IF AI IS ABLE TO GRADUALLY GENERATE STABLE INCOME AND PROFITS, THESE INPUTS WILL BE CONSIDERED AS EARLY LAYOUTS。

Conversely, SpaceX ' s valuation logic would be put under pressure if AI ' s operations were to remain in the recapitalization lease phase. Because markets ultimately need to see not just income growth, but whether profits keep up with capital investment。

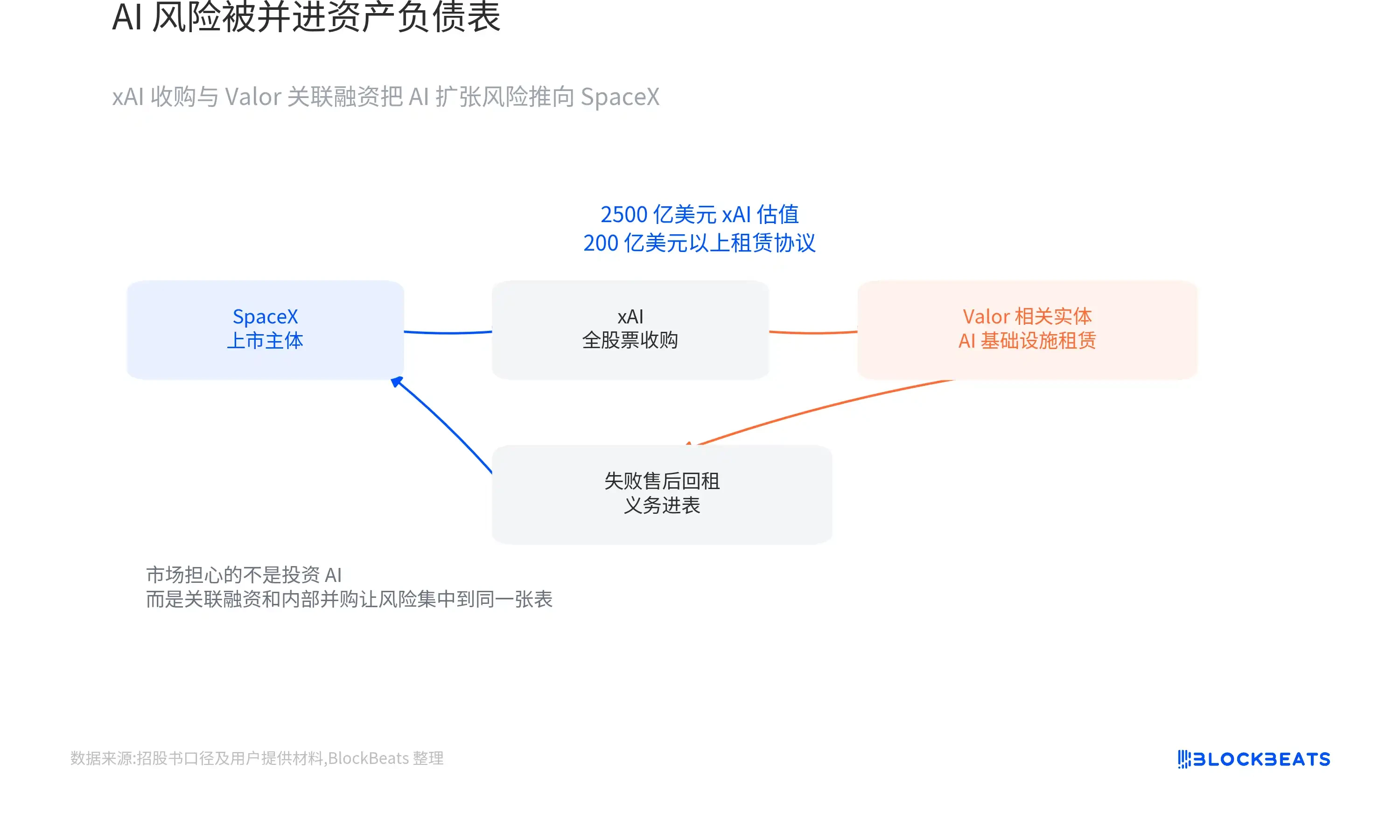

After the acquisition of XAI, SpaceX took over the risks of AI expansion

SpaceX's AI input is not just about increasing capital spending。

In February 2026, SpaceX acquired xAI as a whole stock exchange. The transaction was valued at approximately $1 trillion for SpaceX, approximately $250 billion for xAI and about $1.25 trillion for the consolidated total。

The transaction is not strategically difficult to understand. SpaceX has rockets, satellite networks and potential orbital infrastructure, while xAI has Grok, large data centres and AI operations. Together, the two could provide a more complete framework for orbital data centres and space computing narratives。

But from a financial point of view, SpaceX is not just about the growth space of AI, but about the capital pressure behind the expansion of AI。

The equity book disclosed that XAI affiliates had entered into over $20 billion AI infrastructure lease agreements with the related entities of Valor Equity Partners, covering GPU and data centre hardware. Valor founder Antonio Gracias is also a SpaceX board member and a long-term partner of Mask。

Some of these transactions were classified as “failed sales and leasebacks” because they failed to meet the accounting recognition requirements for the return of the lease. This means that the corresponding obligation needs to be entered into SpaceX ' s balance sheet as a debt, rather than simply treated as a lease cost。

Reducing the pre-existing cash pressure on data centre construction through leasing and financing arrangements is not by itself uncommon. The real source of market concern is the fact that the financier is not a fully independent third party and that both the purchaser and the seller of XAI are controlled by Mask。

This makes it difficult to avoid two issues:

is the $250 billion valuation of xAI reasonable

Are the terms of the transactions related to financing sufficiently transparent

Rather than SpaceX starting to invest AI, the market is concerned that the debt, financing arrangements and implementation risks of AI operations are entering the balance sheets of listed companies through internal M&As and related transactions。

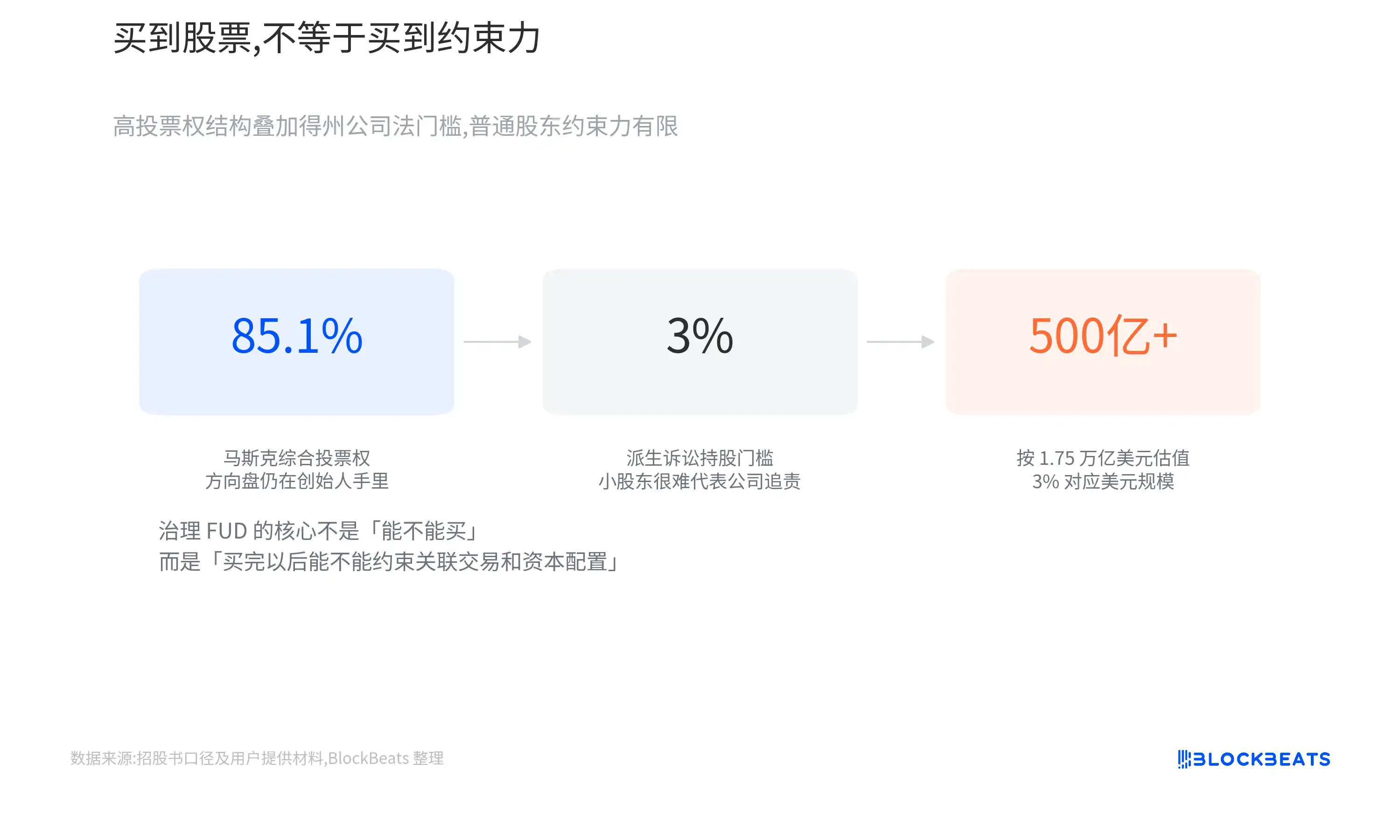

This concern is further amplified by the Texas Companies Act. SpaceX is registered in Texas, and the law allows open companies to raise the equity threshold for shareholder-assigned litigation and limits shareholders ' access to selected mail, text messages and electronic communication records. For the proposed valuation of approximately $175 trillion SpaceX, the 3 per cent equity equivalent has exceeded $50 billion。

This does not mean that ordinary shareholders are not in a position to sue companies under any circumstances。

It means, however, that the actual threshold would be very high if investors felt that related transactions were detrimental to corporate interests and wished to challenge directors or executives on behalf of companies。

As corporate boundaries become increasingly blurred, the open market bears not only business risks, but also capital allocation risks for the entire business system of Mask。

Investors can buy growth but can hardly influence decision-making

Governance issues are important because SpaceX is about to become a listed company, but the influence that ordinary investors can exert is very limited。

SpaceX uses a dual equity structure. Mask would continue to maintain absolute control through high-voting shares, and it would be difficult for ordinary shareholders to change the outcome through voting mechanisms even if companies would have future capital allocation disputes, related transaction disputes or strategic directions。

This structure is not uncommon. Many technology companies will use dual-equity designs to prevent the founders from losing control when they are listed。

However, SpaceX is unique in that companies still need to make a large number of high-risk, long-cycle and high-capital intensity decisions in the future. Investors need to accept not just a lower vote but a more extreme governance premise:

Companies can continue to invest substantial resources in Starship, AI and orbital infrastructure, and even if these projects are not profitable in the short term, it is difficult for ordinary shareholders to change strategic direction。

Such a structure may not be a problem for long-term Mask investors. SpaceX ' s past successes are built on the founding fathers ' strong individual decision-making abilities and risk preferences。

But for investors who are more focused on transparency in governance, this means another thing:

Investors have long-term implementation risks, but it is difficult to really constrain management。

Starship is a technical project and a valuation variable

Market concerns about SpaceX are not focused solely on AI and governance structures。

The next generation of Starlink satellites, orbital data centres and Mars transport ultimately depend heavily on the same infrastructure: Starship。

Starship means more than just making a bigger rocket. It requires a significant reduction in unit launch costs, an increase in the size of a single payload and, ultimately, a high frequency and repeatable commercial launch。

Only when Starship actually enters the scale-up operational phase will SpaceX make it possible to deploy the next generation of satellite networks at a lower cost, put larger equipment into orbit and create realistic conditions for the orbit computing infrastructure。

That is why every Starship test is not just space news, but also how the market understands SpaceX's long-term valuation。

SpaceX ' s valuation does not depend solely on Starship ' s ability to fly, but rather on its ability to fly as stable, low-cost and high-frequency as an infrastructure tool。

WHAT ARE YOU WORRIED ABOUT

Looking at several data sets together, a more complete framework than "Is SpaceX overestimated": the chain of stars has proven its commercial value, recycleable rockets have created clear competitive barriers, and AI and Orbital Data Centres provide new growth space for companies。

AT THE SAME TIME, HOWEVER, CORPORATE VALUATIONS HAVE REACHED US$ 1.75 TRILLION, THE AI SECTOR CONTINUES TO SUFFER SIGNIFICANT LOSSES, CAPITAL EXPENDITURE CONTINUES TO EXPAND, ASSOCIATED FINANCING AND INTERNAL M&AS HAVE BECOME INCREASINGLY BLURRED, AND THE GOVERNANCE CONSTRAINTS THAT ORDINARY SHAREHOLDERS CAN IMPOSE ARE LIMITED。

These facts can be established at the same time and are not contradictory to each other。

Because the FUD around SpaceX is not a denial of the company's past performance。

They are:

WHEN MASK PUTS THE CHAIN OF STARS, ROCKETS, AI AND FUTURE ORBITAL INFRASTRUCTURE IN THE SAME VALUATION MODEL, WHAT ARE THE POSSIBILITIES FOR WHICH THE OPEN MARKET IS WILLING TO PAY A PREMIUM, AND FOR WHICH UNCERTAINTIES SHOULD THE DISCOUNT BE RETAINED