STRC broken anchor 11%, can Strategy's permanent motive still move

Photo by AzumaOdaily Daily Planet

Strategy's priority share of STRC is in the process of continuing to “de-convene”。

The US stock exchange shows thatSINCE 15 MAY, THE STRC HAS GRADUALLY DEVIATED FROM ITS TARGET FACE VALUE OF $100, AND THE RECENT DISCOUNTS HAVE INCREASED SIGNIFICANTLY, REACHING A LOW OF $83.26 IN YESTERDAY'S DISK AT A PRICE OF $88.59 AT CLOSING, EXCEEDING THE TARGET FACE VALUE BY 11 PER CENT。

FOR AN ORDINARY STOCK, THE DROP OF 11 PER CENT MAY NOT BE SIGNIFICANT, BUT FOR STRC, THE CONTINUED GRADUATION FROM THE $100 TARGET NOMINAL VALUE MEANS THAT THE CORE DESIGN OBJECTIVES OF THE PRODUCT ARE FACING SERIOUS CHALLENGES。

Because in Strategy's original design, STRC would have been created as a revenue-based security operating around a $100 face value rather than a highly volatile speculative asset. The growing divergence between market prices and target nominal values today has also led a growing number of investors to revisit the logic behind this product。

More importantly, as Strategy continues to expand its Bitcoin reserves, the STRC has grown into the company's most important source of financing。In a sense, the market’s pricing of STRC reflects not only investors’ attitude to a preferred share, but also market confidence in the business model of Strategy’s capital package。

STRC: Strategy Capital Wheel Engine

IN ORDER TO UNDERSTAND THE SERIOUSNESS OF THIS BREAKOUT, IT IS FIRST NECESSARY TO CLARIFY THE STRUCTURE OF THE STRC PRODUCT AND ITS UNIQUE ANCHORING MECHANISM。

STRC is an innovative financial derivative launched by Strategy in 2025。Unlike Strategy ' s regular MSTR, STRC ' s positioning is a sustainable priority unit with fixed target face value (US$ 100) and relatively stable dividends, which are more similar in nature to securities with fixed yield properties。

- Odaily Note: Strategy Founder Michael Saylor recently revealed that STRC was designed with AI support。

In Strategy's balance sheet expansion ring, the STRC is not just an ordinary financing tool, but the strongest engine of the current Strategy Capital Wheel。

Prior to the launch of STRC, Strategy relied mainly on the issuance of convertible Notes and the direct addition of common shares to raise funds to purchase bitcoin. However, there are limitations to both models - debt conversion is subject to the upper limit of maturity and debt-leveraging ratios, while frequent increases in ordinary shares dilute the interests of existing shareholders。

The emergence of STRC has successfully addressed this pain, and its core utility in the Strategy strategy is mainly in two dimensions:

- UNLIMITED “ATM” SCHEME: As long as the StRC market price is stable at $100 or more, Strategy can continuously increase its share of the second market source through the ATM (At-the-Market) mechanism and collect the French currency。

- Zero-equity diluted purchasing powerSTRC, as a permanent priority, does not have a statutory maturity pressure and does not have voting rights for the ordinary shares and distribution of surplus assets. This means that Strategy can create hundreds of billions of French dollars of purchasing power without diluting the interests of MSTR shareholders and increasing interest on hard debt, and put them all into the increase of bitcoin。

By "Increased SRC collection of French currency, buy BTC, raise the net assets of the company, push up the STRC confidence" In this closed circle, Strategy succeeded in building an seemingly infinite cycle of capital flying。

I don't knowTHE KEY PREREQUISITE FOR THIS WHEEL TO WORK IS THAT THE STRC MUST REMAIN CLOSE TO THE $100 FACE VALUE。Once the market price is significantly below $100, Strategy will no longer be able to effectively absorb funds into the market through a discounted priority, based on the ATM collection clause and the market arbitrage logic, and its whole set of capital magic will be de facto stalled。

At the beginning of the design, and in order to ensure that the STRC secondary market price would always match the target face value of $100, Strategy introduced a mechanism for “mutually dynamically adjusted dividends”. In short, Strategy can increase the rate of dividends to increase the attractiveness of products when the market price of STRC is below $100; when the price is above $100, the rate of dividends can be reduced --THEORETICALLY, BY CONSTANTLY ADJUSTING THE RATE OF DIVIDENDS, STRC SHOULD BE ABLE TO OPERATE AROUND $100 FOR A LONG TIME。

But nowEven though Strategy has raised the dividends to 11.5 per cent, and has also changed the rate of distribution from monthly to semi-monthly, the STRC's “de-condensed” state has not been effectively repaired

Reasons for breakout: faith, confidence, or confidence

It's not workingIT MEANS THAT THE RISK THAT THE MARKET IS PRICING HAS EXCEEDED THE RATE OF RETURN ITSELF。In the light of current market discussions, the risk concerns of the market are mainly at two levels。

The first is the technical aspects of the surface。According to some marketers, much of the recent decline has resulted from the concentration of arbitrage when leveraged。

DURING THE PAST YEAR, THE STRC HAS BEEN TRADING AROUND $100 A LONG TIME, THUS ATTRACTING A LARGE AMOUNT OF REVENUE-TYPE ARBITRAGE. THIS TYPE OF FUNDING TENDS TO LEVERAGE THE GAINS TO GENERATE DIVIDENDS WHILE GENERATING ARBITRAGE FOR PRICE RETURN. HOWEVER, AS THE STRC FELL BY $100 AND CONTINUED TO WEAKEN, SOME LEVERAGE ACCOUNTS BEGAN TO TRIGGER WIND LINES AND WERE FORCED TO SELL THEIR HOLD; THE FALL IN PRICES, IN TURN, CAUSED MORE LEVERAGE TO FLATTEN, EVENTUALLY CREATING A CHAIN REACTION。IN THE PROCESS, THE PRESSURE OF DUMPING CONTINUES TO STRENGTHEN ITSELF, RESULTING IN A DECLINE IN THE STRC THAT FAR EXCEEDS THE NORMAL CHANGES IN SUPPLY AND DEMAND。

However, the mere use of leverage to explain current market performance does not seem to be sufficient。For many investors, deeper concerns are related to Strategy ' s liquidity reserve position。

Earlier this month, Morgan Chase published a study that states that:Strategy has an interest obligation of approximately $1.7 billion per year, which, at the current level of cash reserves, is sufficient to cover only about 6.3 months of priority dividends expenditureI don't know. It also raises concerns about the ability of Strategy to cover future liquidity commitments。

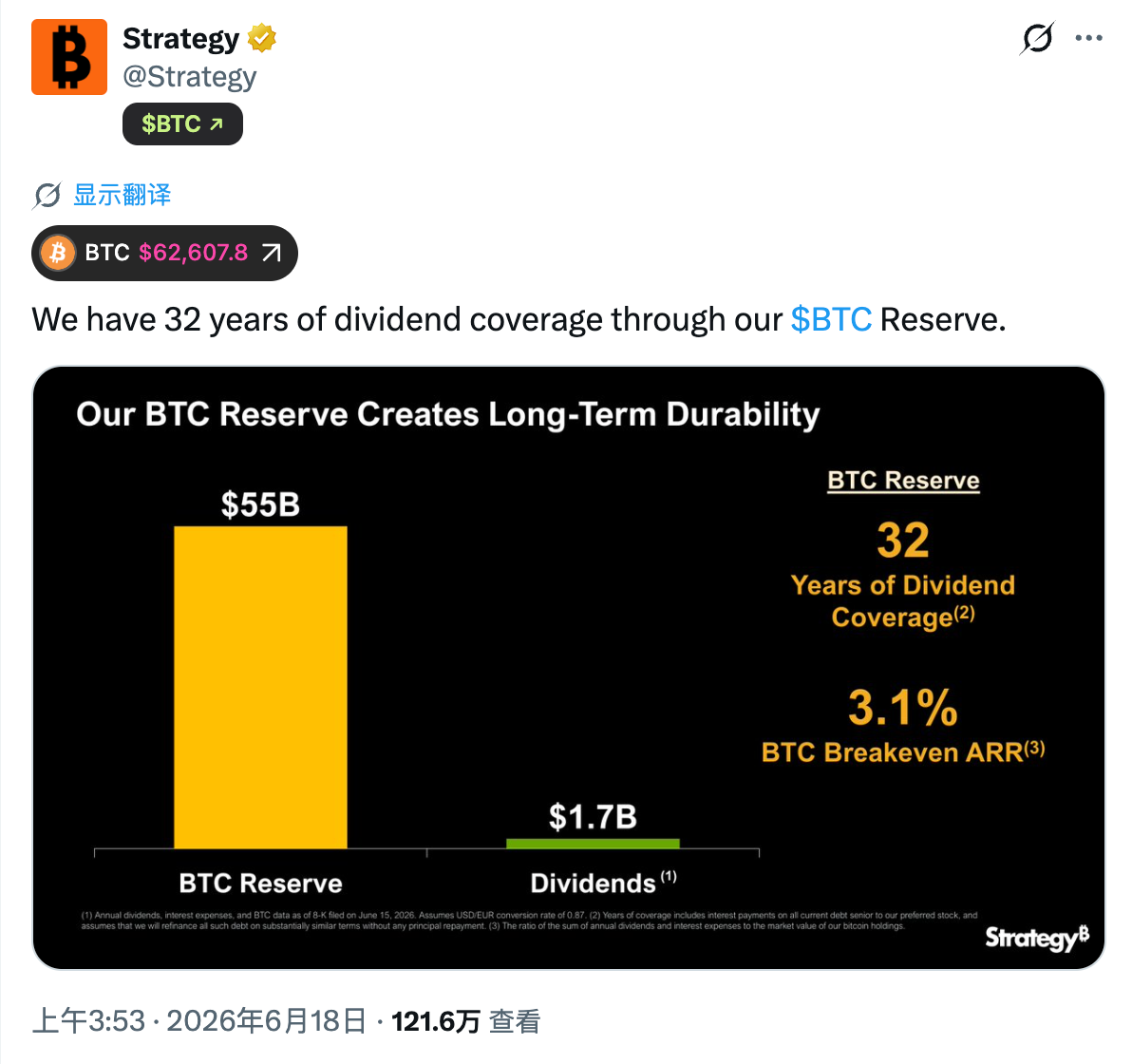

This was explained differently by Strategy, whose official communication in X stressed thatThe inclusion of its large bitcoin reserves would be sufficient to cover 32 years of dividends payments。

The problem, however, is that the two statements are actually based on different premises. Morgan Chase is concerned about the cash nature of Strategy, while Strategy's calculations imply an important assumption --Where necessary, companies can obtain funds by selling bitcoin。

This is precisely where the market is most sensitive. At the beginning of this month, Strategy sold its Bitcoin warehouse for the first time, although it was only 32 in size and was officially packaged as a “active market de-sensitization test” and mentioned that “more will be bought later”, but this continued to have a severe impact on the market. This is because, over the past few years, Strategy and his founder, Michael Saylor, have been passing on a central narrative to the market — that bitcoin is a long-term strategic reserve asset, and that companies will be able to access operating capital market finance rather than relying on the sale of bitcoin。

So, when the market first sees Strategy actually sells bitcoin, it inevitably raises even greater concerns --In the event of a tightening of the future financing environment, does Strategy need to rely further on the sale of bitcoin to meet dividends obligations? If the answer is not absolute, then the investor must reassess the risk level of the relevant securities。

From this point of viewBehind STRC, which continues to be “de-constructed”, is a re-evaluation of the robustness of the capital structure in general。

Strategy's buyout is probably going to sell

For Strategy, the greatest impact of the continuous breakout of STRC is the weakening of the financing function。

Over the past few years, Strategy has been able to continuously expand its Bitcoin reserves, with the core logic being to obtain funds from capital markets through the issuance of securities such as equities, debt swaps and priority shares, and then to use funds to raise bitcoin. The STRC is the most important financing tool for Strategy, which means that the market is demanding higher risk compensation when it deals with a target value of less than $100 for a long time, and that Strategy’s ability to finance will be put on a temporary standstill。

Next, the sturdy state of STRC may be an important indicator of the market's risk profile。If STRC is in a long-term state of discount, which results in continued capacity constraints, and Strategy ' s cash reserves are being depleted, the market ' s concern that Strategy may in the future meet the demand for dividends by selling more bitcoin will increase。

Once this expectation has been strengthened, its impact will no longer be limited to STRC itself. As one of the most important marginal buyers of the Bitcoin market in the last few years, Strategy’s ability and pace of financing have always profoundly affected market supply and demand expectations, if Strategy’s purchases were converted to sales boards, or if it created unimaginable downward pressure on bitcoin。