From Echo to Flying Tulip, interpret new trends in encrypted finance

By Sarabh Deshpande

Original title: Capital Force in Crystal

Compiled and collated: Bitpush News

Experiments such as Coinbase's $400 million acquisition of Echo and the Flying Tulip's permanent downtime options indicate that financing modalities are being completely reformulated。

These models may be different, but the common denominator is to seek equity, liquidity and credibility in the mobilization and deployment of new projects。

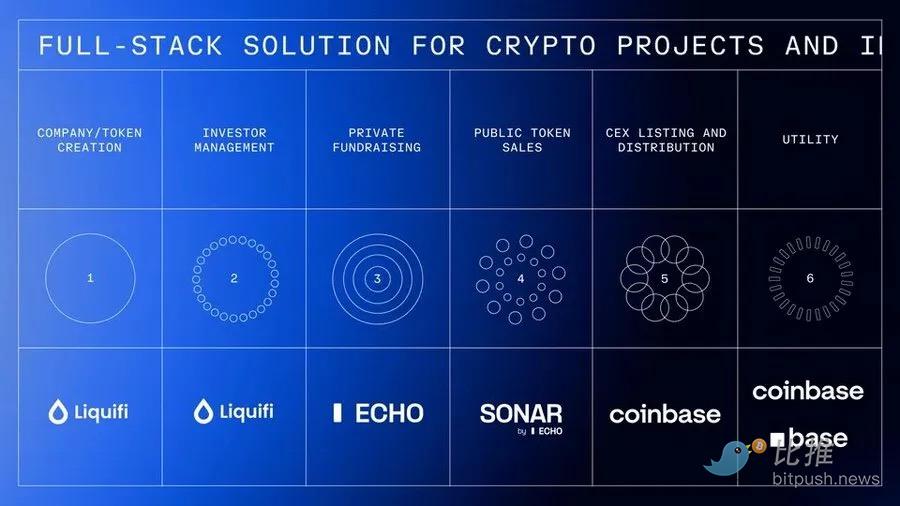

Coinbase Vertical Integration

Coinbase recently acquired Echo, a community finance platform created by Cobie, for approximately $400 million。

The same transaction also included a $25 million NFT purchase to revive a podcast, which imposed a binding obligation on the facilitators Cobie and Legger Status to produce eight new sets of content after NFT had been activated. Echo has assisted in the completion of more than 300 rounds of financing, totalling over $200 million。

This acquisition followed the recent acquisition of Liquifi by Coinbase, which resulted in the completion of the entire service warehouse for encrypted project tokens and investments。

The projecter may use LiquiFi to create tokens and manage the stock structure, finance them through a private group of Echo or the public distribution of Sonar, and then place the token on the Coinbase Exchange for secondary market transactions. Income opportunities are created at each stage:

LiquiFi receives the replacement fee for currency management services, Echo obtains value through profit-sharing arrangements, and Coinbase earns handling fees from offline token transactions。

This integrated service warehouse enables Coinbase to benefit from the life cycle of the project, not just the trading phase。

This is a good deal for Echo, because without upward integration with the exchange, it will be challenging to generate sustainable income. Currently, the model focuses on performance fees, which may take as many years to monetize as risky transactions。

Why would Coinbase pay such a high price for a product that only helped finance (which means Echo helped finance $200 million and bought $400 million)

Remember that $200 million is not Echo ' s income, but only its total value of assisted financing。

Coinbase pays a counterweight that includes links with Cobie (Cobie is considered to be one of the leading players in encryption for a long time), Echo’s network effects, technological infrastructure, regulatory positioning, and its position in the emerging encryption capital formation architecture。

Prominent projects such as MegaETH and Plasma have been financed through Echo, where MegaETH has chosen to make a follow-up round of financing through Sonar, the Echo public distribution platform。

The acquisition gained the confidence of Coinbase ' s founders who were sceptical about the centralization of the transaction, enabling them to access community-driven investment networks and to acquire infrastructure that would extend far beyond purely encrypted money to traditional assets of monetization。

Each project has three to four stakeholders: teams, users, private investors and public investors. Finding the right balance between incentives and the distribution of tokens has been challenging. When the encryption sector launched the ICO in 2015-17, we saw it as an honest model for investment channels for early "democratization" projects. However, some sales are sold out even before you can connect with MetaMask, while private fundraising is based on white lists, thus excluding most retail buyers。

Of course, the model must also evolve in response to regulatory concerns, but this is another topic. However, the story here is not just about Coinbase ' s vertical integration, but focuses on how the financing mechanism itself evolves。

Flying Tulip's permanent downside options

The Flying Tulip of Andre Cronje aims to build a whole chain exchange that integrates spot transactions, derivatives, borrowing, currency markets, primary stable currency (ftUSD) and chain insurance into a unified cross-guarantee system. Its objective is to compete with Coinbase and Binance, and at the product level with rivals such as Ethena, Hyperliquid, Aave and Uniswap。

THE PROJECT USES AN INTERESTING MECHANISM FOR RAISING FUNDS AND EMBEDDING A PERMANENT DOWNSIDE OPTION. INVESTORS INVEST IN ASSETS TO OBTAIN FT COINS (10 FTS PER $1 INVESTMENT) AT A COST OF $0.10 PER UNIT, WHICH ARE LOCKED IN. INVESTORS CAN DESTROY FT COINS AT ANY TIME TO REDEEM THEIR INITIAL CONTRIBUTION OF UP TO 100 PER CENT OF THE CAPITAL OF THE ASSET. IF SOMEONE INVESTS 10 ETH, THEY CAN REDEEM 10 ETH AT ANY TIME, REGARDLESS OF THE MARKET PRICE OF THE FT。

It's time to watch the options never expire, so it's called "forever." Redemption takes place through an independent chain reserve managed by a funded, audited smart contract, which is settled in a procedural manner, with a queue and speed limit mechanism to prevent abuse while maintaining solvency. If the reserve is temporarily insufficient, the request enters a transparent line and is processed sequentially after replenishment。

It creates three options for investors and aligns incentives。

- First, investors can hold locked tokens and retain foreclosures, maintaining downside protection while capturing any upward potential when the agreement succeeds。

- Secondly, they can redeem their original principal by destroying tokens, which have been permanently destroyed。

- Alternatively, they could transfer the tokens to CEX/DEX for a cash withdrawal, but see that the downside option lapsed immediately after the presentation, and that the original principal released was attributed to Flying Tulip for operation and currency buy-back. This creates a strong deflationary pressure: the sale of tokens is the loss of bottom protection. Secondary market buyers do not get foreclosures. This protection applies only to participants in the first sale, thereby creating a two-tiered token structure with different risk situations。

The capital deployment strategy addresses an obvious paradox: since all fund-raising efforts have a permanent downside, the team is effectively unable to access these funds, and therefore effective funding is zero。

INSTEAD, THE $1 BILLION RAISED WILL BE DEPLOYED TO LOW-RISK CHAIN-BASED REVENUE STRATEGIES WITH A TARGET ANNUALIZED RETURN OF ABOUT 4 PER CENT. THE FUNDS CAN BE TRANSFERRED AT ANY TIME. THIS GENERATES ABOUT $40 MILLION PER YEAR, ALLOCATED TO OPERATING EXPENSES (DEVELOPMENT, TEAM, INFRASTRUCTURE), FT COIN BUYBACK (CREATING BUYING PRESSURE) AND ECOSYSTEM INCENTIVES。

OVER TIME, ADDITIONAL SOURCES OF REPURCHASE FINANCE WILL BE ADDED TO THE COST OF AGREEMENTS FROM TRANSACTIONS, BORROWING, LIQUIDATION AND INSURANCE. FOR INVESTORS, THE ECONOMIC TRADE-OFF IS TO GIVE UP 4 PER CENT OF THE EARNINGS THAT THEY MIGHT DERIVE FROM SELF-DEPLOYED CAPITAL AND TO OBTAIN A FT TOKEN WITH THE UPPER POTENTIAL AND PRINCIPAL PROTECTION. IN ESSENCE, INVESTORS WOULD ONLY EXERCISE A DOWNSIDE OPTION IF THE FT TRANSACTION PRICE WAS BELOW THE PURCHASE PRICE OF $0.10。

Gains are only an integral part of income flows. In addition to lending, product packages include automated marketers (AMM), permanent contracts, insurance and a continuous income-generating delta neutral stability currency。

In addition to the projected revenue of $40 million from deploying $1 billion to different low-risk DeFi strategies, other products can generate revenue。

A top-end permanent contract trading place such as Hyperliquid has earned $100 million in single-month fees, almost twice as much as a $1 billion capital could earn by borrowing through DeFi at a rate of 5-6 per cent。

The pattern of token distribution is very different from all past secure financing. Traditional ICO and wind project support usually allocates 10-30 per cent to teams, 5-10 per cent to consultants, 40-60 per cent to investors, 20-30 per cent to foundations/ecosystems, usually with locks but secure distribution. On start-up, Flying Tulip allocated 100 per cent of its tokens to investors (private and public) and the initial allocation for teams and foundations was 0 per cent. Teams are exposed only through open market buy-backs funded by agreed income shares and are bound by transparent published schedules. If the project fails, the team will get nothing. The supply began with 100 per cent ownership of the investor, with the gradual shift over time to the Foundation through redemption and the permanent destruction of the redeemed tokens. The currency supply is capped on the basis of actual fund-raising. If $500 million were raised, only 5 billion FTs would be found; the ceiling for the collection window would be 10 billion FTs (the equivalent of $1 billion raised)。

This new mechanism addresses the problems that Cronje himself experienced in the course of the Yorn Finance and Sonic projects。

As he explained in his presentation document: "As a founder of two large coin projects (Yearn and Sonic), I am aware of the pressure of tokens. The token itself is a product. If the price falls below the price that the investor enters, this may lead to short-term decision-making choices that may be compromised by token benefits. Providing a mechanism to reassure the team, to know that there is a bottom line and that investors can take back principal in the worst-case scenario would greatly reduce this pressure and cost. "

The permanent fall-over option separates the token mechanism from the operating capital and removes the pressure to make agreed decisions based on currency prices, allowing teams to focus on building sustainable products. Investors are protected, but at the same time they are encouraged to hold them in order to capture up-to-date gains, making the coin less "successful" to the survival of the project。

The self-enhanced growth wheel described in the Cronje file outlines the economic model: $1 billion in annual gains of $40 million from 4 per cent annualization, distributed between operation and currency buy-backs; the start-up of agreements generated additional costs from transactions, borrowing, clearing and insurance; and these revenues financed more buy-backs。

Foreclosure and buyback create deflation of supply pressures; supply reductions, combined with buying pressure, drive price appreciation; higher token values attract users and developers; more users incur more costs and finance more buy-backs; and recycle. The model is successful if the agreed income ultimately exceeds the initial revenue, allowing the project to be self-sustaining beyond the initial contribution。

ON THE ONE HAND, INVESTORS HAVE ACQUIRED DOWNSIDE PROTECTION AND CORPORATE-LEVEL RISK MANAGEMENT. ON THE OTHER HAND, THEY FACE REAL OPPORTUNITY COSTS OF 4 PER CENT OF THEIR ANNUAL EARNINGS, AS WELL AS CAPITAL EFFICIENCY LOSSES THAT ARE LOCKED IN BECAUSE THEY EARN LESS THAN MARKET RETURNS. THE MODEL WOULD ONLY BE JUSTIFIED IF THE FT PRICE APPRECIATED SIGNIFICANTLY TO MORE THAN $0.10。

Financial management risks include the decline in DeFi returns to less than 4 per cent, the failure of return agreements (e.g., Aave, Ethena, Spark) and doubts as to whether $40 million per year is really sufficient to fund operations, competitive products and meaningful buy-backs. Moreover, to go beyond peers like Hyperliquid, Flying Tulip must truly become a liquidity centre, a difficult battle, given that existing players have taken the lead and have taken over markets with excellent products。

A 15-person team to build a whole-house DeFi system that competes with mature agreements with huge pre-emptive advantages is at risk of implementation. Few teams have been able to match Hyperliquid ' s implementation, and the agreement has cost over $800 million since November 2024。

Flying Tulip reflects the evolution of lessons learned from Cronje ' s previous projects。

Yearn Finance 2020 has pioneered a fair start-up model for zero-founder distribution (Andre had to obtain his YFI through mining), rising from 0 to more than $40,000 in a few months, reaching a market value of over $1.1 billion in one month. The same zero team allocation was used by Flying Tulip, but institutional support was increased (200 million United States dollars, compared with zero self-financing) and the lack of investor protection in Yern。

The release of Keep3rV1 in 2020 of the unexpected test version (the token surged from 0 to 225 US dollars in a few hours) made people aware of the risks of unaudited, sudden releases; Flying Tulip implemented audited contracts and clear documents prior to the public sale. The experience with currency price pressure in the Fantom/Sonic project has directly shaped the downside options model。

Flying Tulip appears to combine the best elements — — equitable distribution, no team allocation, structured start-up and investor protection through innovative, permanent downscaling options mechanisms. Its success depends on the quality of the product and its ability to attract liquidity from powerful users who are used to using competitors such as Hyperliquid and centralized exchanges。

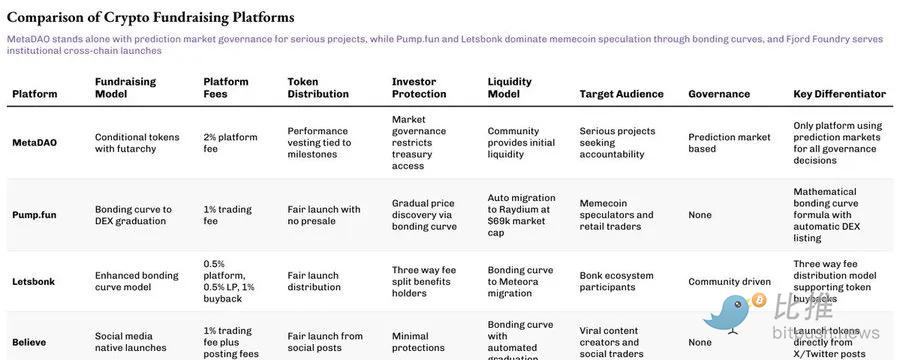

MetaDAO finance supported by Futarchy

If Flying Tulip had reformulated investor protection, MetaDAO had re-examined the other half of the equation: accountability。

Projects funded through Matadao do not actually receive the funds they raise. Instead, all capital is stored in a chain-based treasury, with conditional markets certifying each expense. The team had to propose how they intended to spend it, and the token holders had to be sure that the actions would be of value. Only when the market agrees will the transaction take place. This is a recasting of finance as a governance structure in which financial controls are distributed and codes replace trust。

Umbra Privacy is a groundbreaking example. The Solana-based privacy project received over $150 million in committed investment, with a market value of only $3 million, distributed pro rata, with the excess being automatically refunded from smart contracts. All team tokens are locked behind price milestones, meaning that the founders can only achieve value when the project truly grows. The result was a sevenfold performance after publication, which also proves that investors still aspire to equity, transparency and structure, even in a rich market。

The MetaDAO model may not yet have been mainstreamed, but it restores what was promised in the area of encryption: a system in which markets, not regulators, determine what is worth financing。

Currently, encrypted money financing is entering a period of reflection, and many of the inherent perceptions are being broken:

- The Echo case demonstrates that even without direct access to the exchange, access to high-quality community resources has its own great valuation potential

- The Flying Tulip experiment is testing whether new investor protection mechanisms are likely to replace the traditional token economic model。

These explorations are reshaping our perception of the value logic of encrypted markets。

The key to the success of these experiments is not how perfect the theory is, but the effectiveness of actual implementation, whether users pay for them, and whether these mechanisms can withstand market pressures。

The underlying reason why the financing model continues to emerge is that the core contradictions between projecters, investors and users remain unresolved。

each new model claims a better balance of interests, but ultimately faces the same reality test — — whether or not to stand firm in real markets。