DeFi earnings winter: liquidity silt, leverage shrink, arbitrage no door

Is it a simple cycle of fluctuations or is the market undergoing a structural reshaping

This post is part of our special coverage Syria Protests 2011

The end of a cycle often begins with the most subtle indicators。

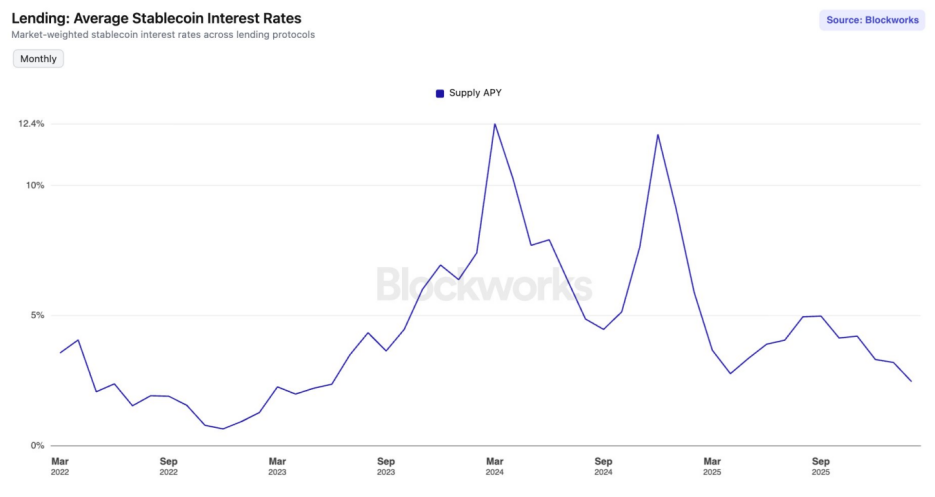

Since September 2025, the DeFi (decentralized finance) market has entered the “cold winter of interest rates”. The average annualized rate of return on deposits (APY) in the mainstream stable currency in the head lending agreement has touched the lowest level since June 2023。

USDC and USDT deposit rates have fallen by 2 per cent on the Aave V3 of the ETA host network. At the same time, interest rates on the United States 10-year national debt have recovered to 4.24 per cent. For DeFi Summer, a DeFi player who's used to high ASY, it's not just a fall in numbers, it's more like a dead-end clock。

Is this a simple cycle of fluctuations or is the market undergoing a structural reshaping

Supply and demand mismatch, liquidity overload causing interest rate collapse Fall

Over the past six months, the interest-rate curve of mainstream lending agreements has shown a downward trend, and their interest-rate model is experiencing a collapse in returns triggered by “supple demand”。

The interest rate is the price of capital. The physical basis for determining prices is the supply of capital。

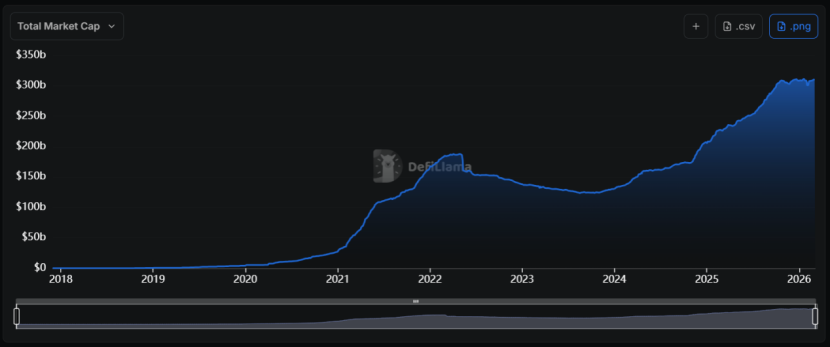

Since 2024, the stable currency track has experienced an unprecedented “expanding tide” with a dramatic increase in the total market value from less than $130 billion to over $310 billion, with a complex annual growth rate of about 55 per cent。

The problem is:The surge in supply has not been accompanied by a proportional expansion of demand in the chainI don't know。

The problem is:The surge in supply has not been accompanied by a proportional expansion of demand in the chainI don't know。

When the supply of a commodity (stable currency liquidity) in the market increases significantly and demand weakens, its prices (interest rates) inevitably fall. That is the rationale of economics, and DeFi cannot be exempted。

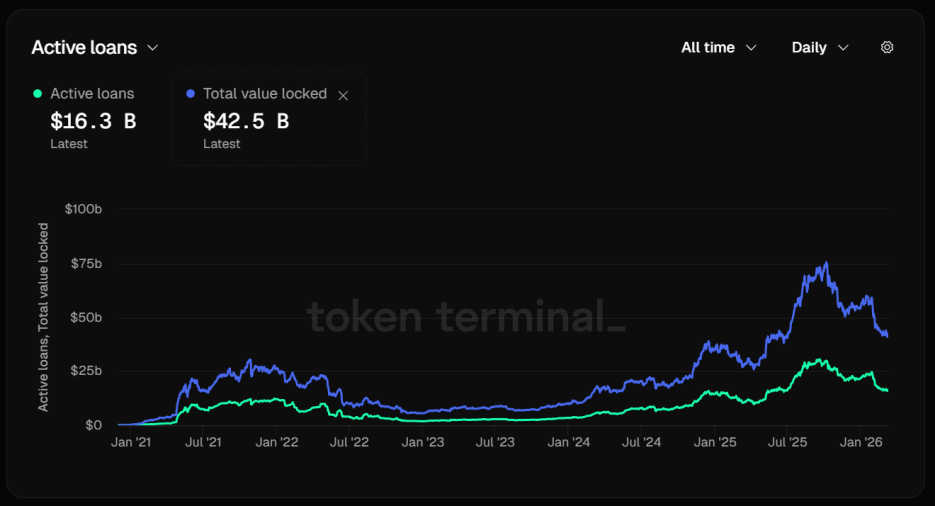

In the case of Aave, the head of the borrowing track, the use of its stable currency is declining significantly. As at 12 March, Aave ' s total warehouse capacity (TVL) had reached $42.5 billion。

A disturbing figure emerges: active loans amount to only $16.3 billion. More than 60 per cent of the assets deposited were inactive, and the supply-demand imbalance directly led to a rapid decline in interest rates。

This meansThe funds were not available, liquidity was severely silt and the protocol algorithm had to automatically adjust the interest rate curve in an attempt to attract more borrowers。

However, such efforts have yielded little. The base interest rates of USDC and USDT on Aave V3 and USDT have fallen by 2 per cent in the context of the Taipei Master Network, which contrasts sharply with the double-digit returns during the cattle market。

However, such efforts have yielded little. The base interest rates of USDC and USDT on Aave V3 and USDT have fallen by 2 per cent in the context of the Taipei Master Network, which contrasts sharply with the double-digit returns during the cattle market。

The stable currency market has fallen into a “liquidity trap”. When low-cost finance is abundant in the market, but high-return investment opportunities are lacking, they accumulate in the pool of loan agreements。

The collapse of financial rates, the cooling of revolving borrowing caused the leveraging to slow down

DeFi's interest rate stability boom is essentially driven by “leverage”. When arbitrage activity in the sustainable contract market cools, the demand for sequestered currencies shrinks rapidly, leading to a sharp drop in interest rates。

In cattle markets, where the high rates of money are positive and high as a result of high emotional growth, arbitragers are able to earn financial costs by risk-free hedges through the Delta’s neutral strategy of “to buy cash in stable currency + sell durable contracts”. In this process, stability is fuel。

HOWEVER, THE DERIVATIVES MARKET HAS RECENTLY PERFORMED POORLY. AT THE MAINSTREAM CENTRALIZED EXCHANGE (CEX), BTC AND ETH HAVE EXPERIENCED NEGATIVE OR EXTREMELY LOW POSITIVE FINANCIAL RATES ON SEVERAL OCCASIONS. THIS REFLECTS THE DOMINANCE OR EXTREME CAUTION OF EMPTY FORCES IN THE MARKET。

Either way, it points to the same result:Lack of motivation for arbitragersI don't know。

The annualized capital rate fell significantly and the net profit of the arbitragers would be significantly reduced, taking into account borrowing costs and transaction charges. Their borrowing demand for a stable currency fell off the cliff。

Another major source of stable demand for currency borrowing is revolving borrowing. The typical path of this revenue enhancement strategy is to deposit in Aave such income-type assets as sUSDE, lend stable currencies such as USDC, and exchange the borrowed USDC for more sUSDE。

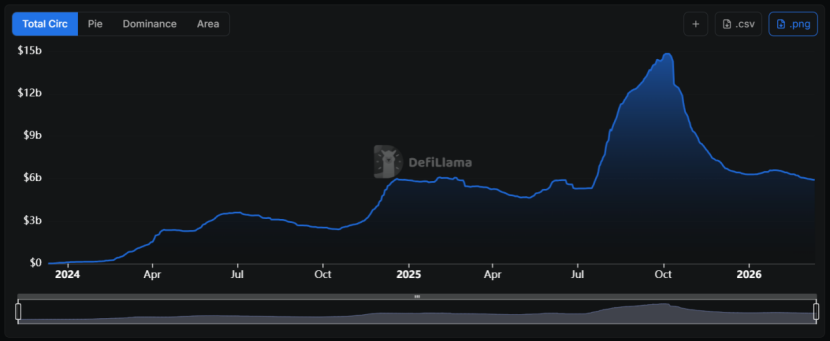

This strategy was followed at one point, because USDe earned as much as 30 per cent, while the cost of borrowing was about 10 per cent, with a 20 percentage point arbitrage gap。

However, after the events of 1011, there was a catastrophic contraction of the spreads and USDe ushered in the “extensibility” ceiling, which went down from close to $15 billion to the current $6 billion。

The USDE rate of return is highly dependent on the size of the market. Since the total holding stock of the market for a lasting contract (Open Interest) is limited, when the size of USDe expands to a certain degree, the empty space it needs to flush itself will lower the market-wide financial rate, thus squeezing the sous-de yield。

The USDE rate of return is highly dependent on the size of the market. Since the total holding stock of the market for a lasting contract (Open Interest) is limited, when the size of USDe expands to a certain degree, the empty space it needs to flush itself will lower the market-wide financial rate, thus squeezing the sous-de yield。

For ordinary traders, a reduction in the sUSDe rate of return would reduce their strategic spreads. Their reduced demand for leverage positions will also further reduce their demand for stable currency collateral。

This is a self-reinforcing negative cycle:There was a further contraction in demand as interest rates declined。

Encryption market risks shift and funds seek certainty

The decline in the overall risk bias in the encrypted market is another important factor contributing to the lowering of interest rates on stable currencies。

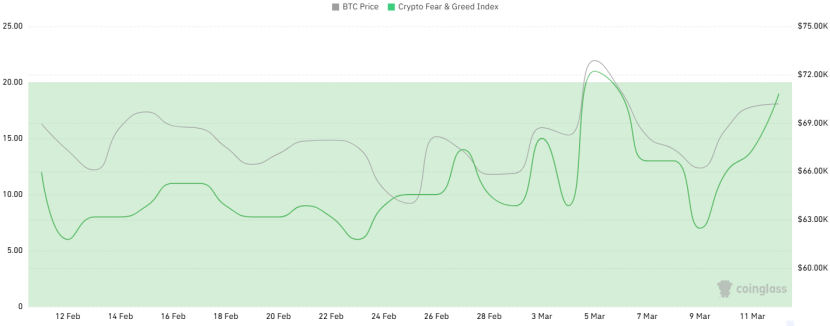

Over the past month, the Encrypted Fear and Greed Index (Fear & Greed Index) has frequently touched the “extreme panic” zone, and even as the BTC price stands at $70,000, there has been no sustained improvement。

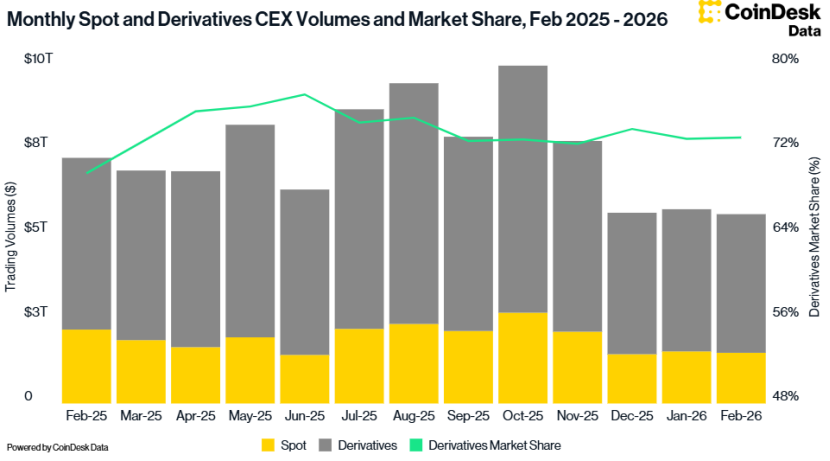

CoinDesk Data also shows that in February the total CEX trade volume declined by 2.41 per cent to $5.61 trillion, the lowest since October 2024。

The decline in risk preferences has led investors to shift to more definitive sub-markets。

The decline in risk preferences has led investors to shift to more definitive sub-markets。

Since January 2024, the effective interest rate of the Federal Fund of the Federal Reserve has remained at over 3.6 per cent. Real interest rates remain relatively high, although the market expects a moderate rate-down path in the future。

This macro-environment has also had a far-reaching deterrent effect on DeFi ' s interest rates for currency stabilization. When risk-free US debt yields are higher than DeFi’s deposit rate, and without risk premium compensation, rational investors will choose to withdraw money from the chain agreement or invest it in an agreement supported by RWA (real world asset)。

This macro-environment has also had a far-reaching deterrent effect on DeFi ' s interest rates for currency stabilization. When risk-free US debt yields are higher than DeFi’s deposit rate, and without risk premium compensation, rational investors will choose to withdraw money from the chain agreement or invest it in an agreement supported by RWA (real world asset)。

In the cold winter of interest rates, not all agreements are shrinking. Sky (formerly MakerDAO) built a unique “revenue moat”。

Sky's earnings also come from a $1.5 billion mature RWA target, which is more dependent on the chain's borrowing needs than Aave's. These assets include United States debt, 3A-class enterprise debt, etc., which are not affected by the volatility of the encrypted market and provide a stable base cash flow。

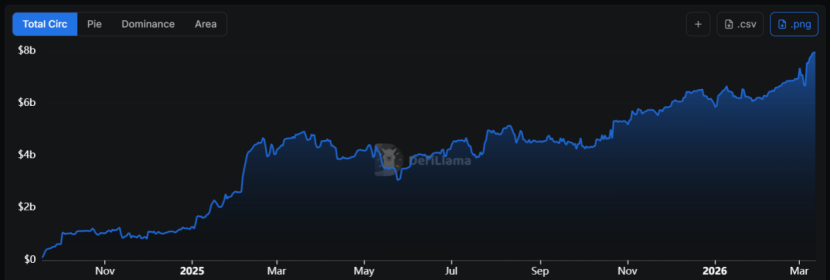

THIS PATTERN OF TRANSFORMING RWA INTO A BOTTOM MORTGAGE HAS CONTRIBUTED TO A 68 PER CENT MONTHLY INCREASE IN THE SUPPLY OF USDS, WITH A MARKET VALUE OF NEARLY $8 BILLION。

So far, the SUSDS interest rate has remained around 3.75 per cent and has become the “factual floor” of the chain rate of return. In the USDC, USDT-related treasury, the interest rate on deposits could be over 5 per cent。

So far, the SUSDS interest rate has remained around 3.75 per cent and has become the “factual floor” of the chain rate of return. In the USDC, USDT-related treasury, the interest rate on deposits could be over 5 per cent。

This led Sky to assume a role similar to that of the "base rate platform". In contrast, interest rates on assets of the same kind in Aave are hardly competitive。

In this waySky is moving from a simple currency stabilization agreement to a "fixed income management" agreementUse its huge RWA combination to hedge down the encryption market. When there is a lack of internal demand within DeFi, it is able to reap benefits from external sources (traditional financial markets)。

FOR INVESTORS, LEARNING TO LOOK AT THE BOTTOM LOGIC OF THE ASSETS BEHIND THE RATE OF RETURN, WHETHER IT COMES FROM THE DIVIDENDS OF NATIONAL DEBT OR FROM THE VOLATILE PREMIUMS OF FUTURES MARKETS, WILL BECOME MANDATORY FOR THE CYCLE. THERE IS ALSO A NEED TO MOVE FROM “CATCHING ASY” TO “SEEKING DIFFERENTIATED RISK EXPOSURES”。

The “cold winter of interest rates” is not only the result of periodic fluctuations, but also the inevitable pain of dehydration of the DeFi “foam”。

Perhaps, just as the 2023 low valley gave birth to the 2024 boom, the bottom of the interest rate may be DeFi is saving energy for the next jump。