Why does the current macro-environment benefit the risk asset

Multi-risk assets are seen in the short term, but the structural risks embedded in sovereign debt, demographic crises and geopolitical reshaping must be observed in the long run. 。

original by: ardxt_xo

Original: AididiaoJP, Foresight News

IN SUMMARY, I LOOK AT MULTIPLE-RISK ASSETS IN THE SHORT TERM BECAUSE AI CAPITAL SPENDING, WELL-OFF-DRIVEN CONSUMPTION AND STILL HIGH NOMINAL GROWTH ARE STRUCTURALLY BENEFICIAL TO BUSINESSES。

More simply: "risk assets" usually perform well when borrowing costs get lower。

At the same time, however, I am deeply sceptical about what we are telling about what this means for the next decade:

- Sovereign debt problems cannot be resolved without a combination of inflation, financial repression or contingencies。

- Fertility and population structures will invisibly limit real economic growth and implicitly magnify political risks。

- Asia, and China in particular, will increasingly be the core definition of opportunity and tail risk。

So the trend is going on, and we keep holding those profitable engines. However, a portfolio is to be built on the understanding that the path to currency devaluation and demographic restructuring will be full of setbacks rather than one-sided。

An illusion of consensus

If you read only the views of the major institutions, you think we live in the perfect macroworld:

Economic growth is “resilient”, inflation is sliding towards targets, artificial intelligence is a long-term windfall, and Asia is a new diversified engine。

HSBC’S LATEST OUTLOOK FOR THE FIRST QUARTER OF 2026 IS A CLEAR MANIFESTATION OF THIS CONSENSUS: STAYING IN STOCK MARKET CATTLE MARKETS, OVER-ALIGNING TECHNOLOGY AND COMMUNICATION SERVICES, BETTING ON AI WINNERS AND ASIAN MARKETS, LOCKING DOWN RETURNS ON INVESTMENT-GRADE BONDS, AND USING ALTERNATIVE AND MULTI-ASSET STRATEGIES TO SMOOTH VOLATILITY。

I agree in part with that view. But if you stop here, you're missing a really important story。

Here, the truth is:

- A PROFIT CYCLE DRIVEN BY AI CAPITAL EXPENDITURE IS FAR MORE INTENSE THAN ONE COULD IMAGINE。

- A monetary policy transmission mechanism that partly lapses due to the accumulation of large public debt on private balance sheets。

- Some structural time bombs — sovereign debt, collapse of fertility, geopolitical restructuring — are irrelevant for the current quarter, but crucial for what the “risk asset” itself means after a decade。

This is an attempt to reconcile the two worlds: a luminous, easy-to-market "resilient" story, and a macro-realistic, complex and path-dependent reality。

Market consensus

Let us start with the general view of institutional investors。

Their logic is simple:

- Stock market bulls continued, but volatility increased。

- Industry styles need to be decentralized: over-equipment technology and communications, with utilities (power demand), industry and financial units to achieve value and diversity。

- Alternative investments and multi-asset strategies are used to cope with declines — such as gold, hedge funds, private credit/equity, infrastructure and volatility strategies。

Focus on revenue opportunities:

- Because of the narrow spreads, funds were shifted from high-yield to investment-grade debt。

- Increase in hard currency corporate debt and local currency bonds in emerging markets to capture spreads and gains associated with low equity markets。

- Using infrastructure and volatility strategies as a source of revenue for inflation。

Asia at the core of diversity:

- China, Hong Kong, Japan, Singapore, South Korea。

- Subjects of concern: Asian Data Centre boom, China’s innovative lead firms, Asian firms’ increased returns through buybacks/ splits/mergers, and high-quality Asian credit debt。

In terms of fixed earnings, they clearly value:

- Global investment-grade corporate debt, as it provides a higher spread and has the opportunity to lock in the rate of return before policy interest rates decline。

- Over-alignment of emerging market local currency bonds to capture interest differentials, potential exchange rate gains and low relevance to equities。

- A small amount of low-cost high-yielding global debt is attributable to its high valuation and individual credit risk。

IT'S A TEXTBOOK-STYLE "END-OF-CYCLE" CONFIGURATION: ON THE MOVE, DIVERSIFICATION, ALLOWING ASIA, AI, AND REVENUE STRATEGIES TO DRIVE YOUR COMBINATION。

I think for the next 6-12 months, this strategy is basically right. But the problem lies precisely in the fact that most macro-analysis is here, and the real risks start here。

2. Fragments under the surface

Macro:

- In the United States, nominal spending grew by about 4-5 per cent, directly supporting corporate income。

- But the point is: who is consuming? Where does money come from

The mere discussion of the decline in savings ( "consumer's lack of money") is a missing point. If well-off households use their savings, increase credit and realize asset gains, they can continue to consume even if wage growth slows and the job market weakens. The excess of consumption over income is supported by a balance sheet (fortune) rather than a profit/loss statement (current income)。

This means that a large proportion of marginal demand comes from wealthy households with large balance sheets, rather than from widespread real income growth。

This is why the data seems so contradictory:

- Overall consumption remained strong。

- The labour market has gradually weakened, especially in low-end jobs。

- This pattern is further reinforced by rising income-to-asset inequalities。

Here, I parted from the mainstream narrative of resilience. Macro aggregates look good because they are increasingly dominated by minorities at the top of income, wealth and capital acquisition。

This is still good for the stock market (profits do not care whether income comes from one rich or ten poor). But this is a slow-burning hazard to social stability, the political environment and long-term growth。

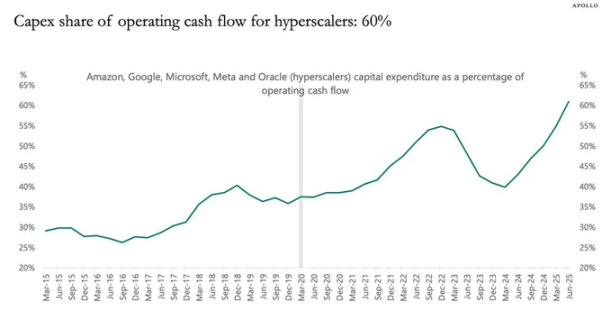

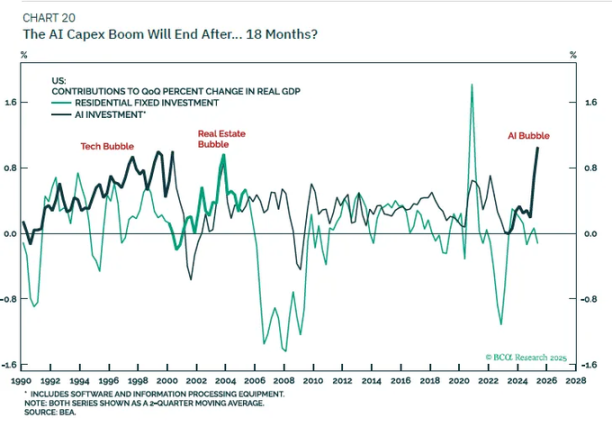

3. AI STIMULUS EFFECTS OF CAPITAL EXPENDITURES

The most undervalued dynamic at present is artificial capital expenditure and its impact on profits。

In short:

- Investment expenditure is the income of others today。

- Related costs (depreciation) will be slowly reflected in the coming years。

THUS, WHEN AI MEGA-ENTERPRISES AND RELATED COMPANIES SUBSTANTIALLY INCREASE THEIR TOTAL INVESTMENT (E.G. BY 20 PER CENT):

- Revenues and profits can be boosted by a huge and pre-eminent boost。

- Depreciation increases slowly over time and is roughly synchronized with inflation。

- The data show that the best single indicator to explain profit at any given point is total investment minus capital consumption (depreciation)。

THIS LEADS TO A VERY SIMPLE BUT DIFFERENT CONCLUSION FROM THAT OF CONSENSUS: IT STIMULATES BUSINESS CYCLES AND MAXIMIZES BUSINESS PROFITS DURING THE PERIOD OF THE AI CAPITAL EXPENDITURE BOOM。

Don't try to stop this train。

THIS COINCIDES WITH THE SUBJECT OF HSBC AND ITS "AI ECOSYSTEMS IN EVOLUTION" AND THEY ARE IN ESSENCE SETTING UP THE SAME PROFIT LOGIC IN ADVANCE, ALBEIT IN DIFFERENT WAYS。

I am more skeptical about the narrative about its long-term effects:

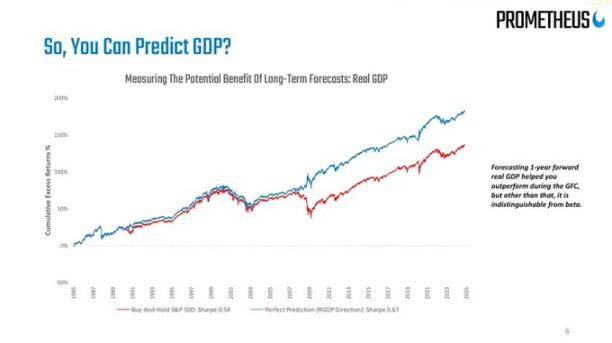

I DON'T BELIEVE THAT AI CAPITAL SPENDING ALONE WILL BRING US INTO A NEW ERA OF REAL GDP GROWTH OF 6 PER CENT。

Capital expenditure slows once the enterprise ' s free-flow financing window is narrow and its balance sheet saturated。

When depreciation catch up, the "profit stimulus" effect recedes; we return to the potential trend of population growth + productivity growth, which is not high in developed countries。

So my position is:

- TACTICALLY: AS LONG AS TOTAL INVESTMENT DATA CONTINUE TO SOAR, THERE IS OPTIMISM ABOUT THE BENEFICIARIES OF AI CAPITAL EXPENDITURE (CHIPS, DATA CENTRE INFRASTRUCTURE, ELECTRICITY GRIDS, NICHE SOFTWARE, ETC.)。

- Strategic: Consider this a cyclical profit boom rather than a permanent replacement of trend growth rates。

Bonds, liquidity and semi-defunct transmission mechanisms

This part becomes a little weird。

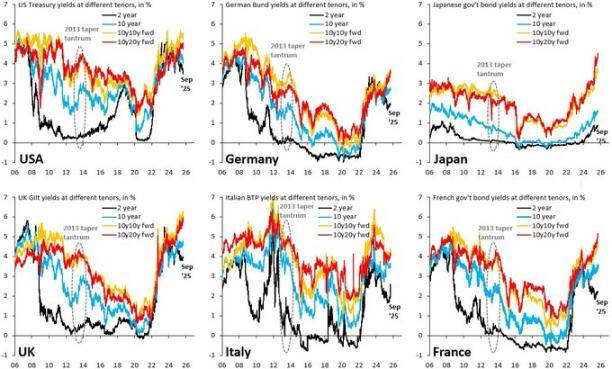

A historical increase of 500 basis points would severely undermine net interest income in the private sector. But today, trillions of public debt lie as security assets. On the private balance sheet, this relationship is distorted:

- Higher interest rates mean that holders of national debt and reserves receive higher interest income。

- Many enterprises and households are indebted at fixed interest rates (especially mortgages)。

- Final result: The net interest burden on the private sector has not deteriorated as macro-projected。

So we face:

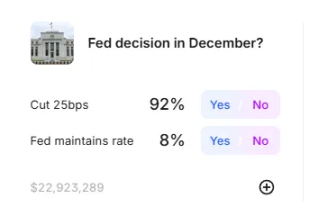

- A hard-on Fed: inflation is still higher than the target, while labour force data are softening。

- A volatile interest-rate market: The best course of dealing this year is a return to the average value of bonds, a panic sale, and a sharp rise in sales, because the macro-level environment is not always clear enough to translate into a clear trend of “severe drops” or “renewal increases.”。

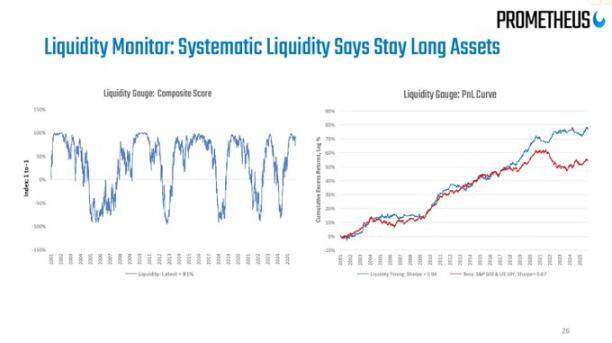

On "mobility," my point is very straightforward:

- The Fed ' s balance sheet is now more like a narrative tool; its net change is too slow and too small to be an effective trading signal relative to the financial system as a whole。

- Real liquidity changes occur in the private sector balance sheet and buy-back markets: who is borrowing, who is lending, and at what margin。

5. Debt, population and the long-term shadow of China

Sovereign debt: the outcome is known, the path is unknown

The issue of international sovereign debt is the defining macro-issue of our time, and everyone knows the solution. Nothing:

BY DEVALUATION (INFLATION), THE DEBT/GDP RATIO IS BROUGHT BACK TO MANAGEABLE LEVELS。

What remains is the path:

Orderly financial repression:

- maintaining nominal growth & gt; nominal interest rates

- It's just a little bit higher than the target

- The real debt burden has been slowly reduced。

Disturbing crisis events:

- The market panics because the financial trajectory is out of control。

- The term premium suddenly surged。

- There was a currency crisis in the weaker sovereign countries。

Earlier this year, we had the taste of markets that had led to a sharp rise in the rate of return on long-term United States national debt due to fiscal concerns. HSBC itself pointed out that the narrative on the "deterioration of fiscal trajectory" peaked during the budget discussion period and then receded as the Fed turned to fear of growth。

I believe that the play is far from over。

Fertility: slow-moving macro-crisis

Global fertility has fallen below replacement levels, not only as a problem in Europe and East Asia, but now also in Iran, Turkey and gradually in parts of Africa. This is essentially a far-reaching macro-impact that has been masked by population statistics。

Low fertility means:

- Higher dependency ratio (increasing proportion of dependents)。

- Lower real economic growth potential in the longer term。

- Long-term social distributive pressures and political tensions resulting from continued higher returns than wage growth。

WHEN YOU COMBINE AI CAPITAL SPENDING (A SHOCK OF DEEPENING CAPITAL) WITH FERTILITY DECLINE (A SHOCK OF LABOUR SUPPLY)

You'll get a world like this:

- Capital owners have performed well in nominal terms。

- The political system has become more unstable。

- Monetary policy is in a dilemma: both to support growth and to avoid causing wage-price spiralling inflation when the labour force finally gains bargaining power。

This will never appear in the institutional vision slide for the next 12 months, but it is absolutely critical for a 5-15-year asset allocation horizon。

China: Key neglected variables

THE VIEWS OF HSBC ASIA ARE OPTIMISTIC: LOOK AT POLICY-DRIVEN INNOVATION, AI CLOUD COMPUTING POTENTIAL, GOVERNANCE REFORMS, HIGHER CORPORATE RETURNS, LOW-COST VALUATION, AND THE WINDFALL OF THE GENERAL INTEREST RATE DECLINE IN ASIA。

My opinion is:

- In terms of dimensions of 5-10 years, the risk of zero allocation to China and the North Asian market is greater than the risk of modest allocation。

- In terms of the dimensions of 1-3 years, the main risks are not macro fundamentals, but policy and geopolitics (sanctions, export controls, restrictions on capital flows)。

THE COMBINATION OF CHINA'S AI, SEMICONDUCTOR, DATA CENTRE INFRASTRUCTURE-RELATED ASSETS, AND HIGH DIVIDENDS AND HIGH-QUALITY CREDIT DEBT COULD BE CONSIDERED, BUT YOU HAVE TO DETERMINE THE SIZE OF THE CONFIGURATION BASED ON A CLEAR POLICY RISK BUDGET, NOT ON HISTORICAL SHARP RATIOS ALONE。