Thirty minutes to crash 45%. SpaceX took a punch before he got on the market

The median bond for liquidated warehouse positions is only $31, three times leveraged, and is almost one-size-fits-all. 。

Original by ChandlerZ, Foresight News

On the evening of May 28th, there was a sharp collapse of the SPACEX-USDH contract on Hyperliquid, the price of which fell from $2277 to $1254 within 30 minutes, a decline of nearly 45%, and then rebounded to approximately $2169。

The crash resulted in the liquidation of 405 users and 1393 warehouses, with a cumulative amount of $1.51 million。

The data show that the total trade volume of the contract over the past 24 hours was only about $4.87 million, the unsettled contract was under $2.9 million and the market depth was extremely low. A large bill of sale almost directly pierced mobility, triggering a step-down. The bomb shelter users were mainly dispersed, with a median bond of about $31 and a common leverage of about 3 times。

The team has noticed a crash in the SPACEX market. The incident was due to the return of erroneous data by the chain data provider, one of the component components of the prognosis machine price, which led to sharp fluctuations in the prognosis and tagging prices in the market, thereby triggering a high level of silo levels among some users。

The team has taken steps to prevent a similar situation from recurring. In addition, the team is assessing the impact of the incident on affected users with a view to developing an appropriate compensation programme. The affected users will be compensated within the next 48 hours。

A weak pricing chain

SPACEX-USDH is a "SpaceX Valuation" encrypted and lasting contract that allows users to pledge changes in market valuations before SpaceX IPO, but does not represent real shares and does not confer equity rights on any shareholders。

On Ventuals, 1 SPACEX represents a valuation of SpaceX $1 billion, which means that the market value to SpaceX is $426.69 billion if the SPACEX price is $420.69。

The central challenge for such contracts is how to price an undisclosed company

The Ventuals programme, which splits pricing into two parts, with one third of its weight coming from the private market data provider under the chain, Notice, combines financing rounds, 409A valuations, mutual fund tags, secondary market transactions and quotations, and comparable listed companies。

Two thirds of the weight comes from the index-weighted moving average of the price of the last 2 hours mark on the contract itself. Notice data are rotated at least once a minute, predicting machine prices updated every 3 seconds。

This design is ideally designed to balance external information and price on the chain, but it has a fatal single-point failure. If the data returned by Notice were per se wrong, one third of the external anchorage became a force to pull prices in the wrong direction。

THE OTHER TWO-THIRDS OF THE AVERAGE CHAIN PRICES CAN HEDGE THE ERROR WHEN THERE IS SUFFICIENT LIQUIDITY, BUT ON A DAILY TRADE VOLUME OF $4.87 MILLION IN SPACEX CONTRACTS, THE CHAIN PRICE ITSELF IS FRAGILE, AND TWO VULNERABLE COMPONENTS ARE STACKED TOGETHER, RESULTING IN A PRICE COLLAPSE。

Zero arbitrage, low mobility under fragmentation

SPACEX flashes out more than just the Ventuals. The entire pre-IPO synthetic product class faces the same dilemma with regard to pricing mechanisms, namely, the absence of a unified spot market and a cross-platform arbitrage route。

In traditional finance, the difference between the price of the same stock at New York and NASDAQ is almost non-existent, as high frequency marketers move bricks at millisecond level. However, in the pre-IPO synthetic product market, such arbitrage is structurally impossible because each platform contract is an asset or derivative issued in accordance with its own rules and cannot cross the platform。

The SPACEX on Hyperliquid and the SAPX on Binance tracked the same company, but there was no mechanism to guarantee price consistency between them, with the result that each platform formed a small closed price-fixing pond, which was dispersed to a number of unconnected sites, each of which was much lighter than the whole。

For Ventuals, the SPACEX-day trade volume of $4.87 million would vary in depth if the existing platform were concentrated in one location, but fragmentation exposed each platform to the risk of low mobility。

the essence of the pre-IPO synthetic product is that a group of people place their bets around a number without open price benchmarks. The price per platform found to reflect only the consensus of the small group of traders on that platform and there was no rigid link to the firm ' s real valuation。

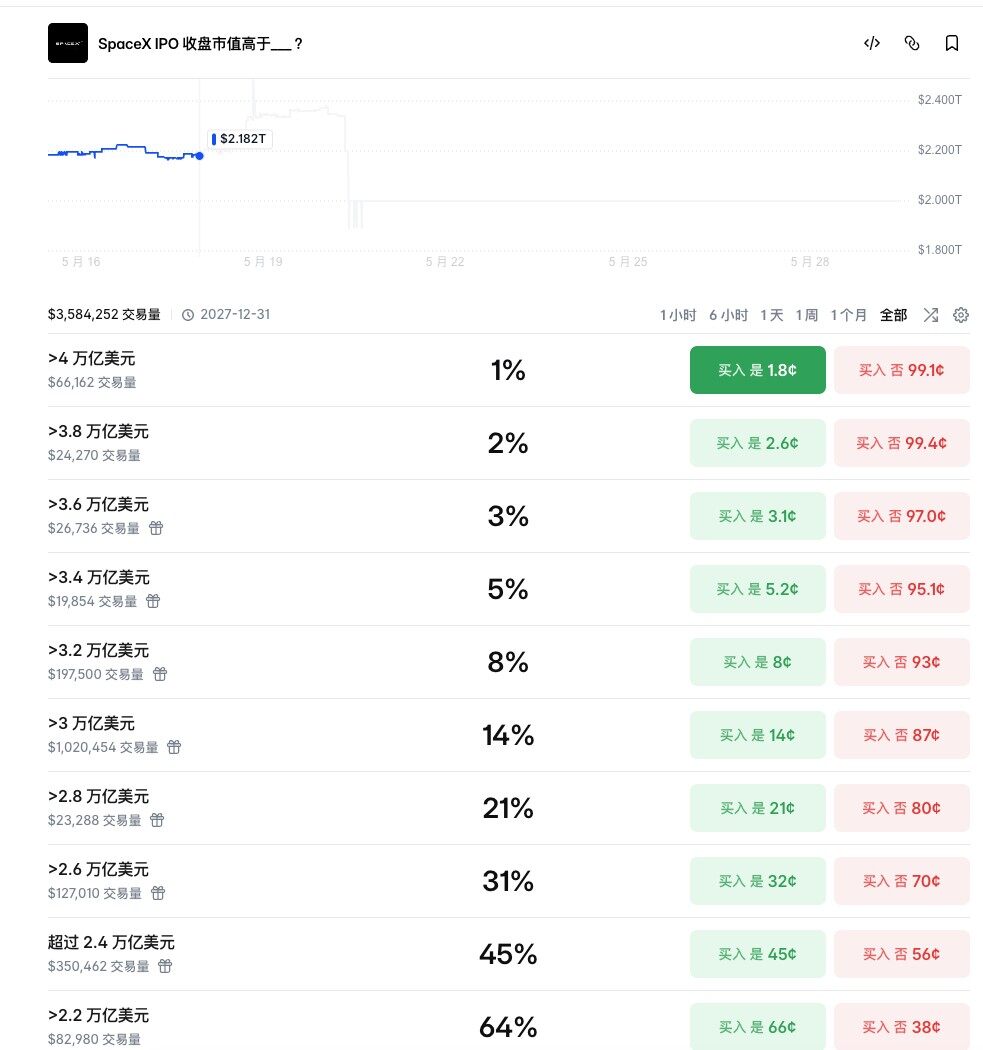

Notice-like sources of data are private market information, with low frequency, narrow coverage and non-transparentity. No one really knows how much SpaceX is worth, and the valuation distribution of SpaceX IPO on Polymarket is equally dispersed, exceeding the inter-zone probability of 2.4 trillion dollars by 45 per cent, and the inter-district probability of 2.6 trillion dollars by 31 per cent。

The mystery is coming to light

SpaceX submitted a confidential S-1 document to the SEC on 1 April, targeting 11 June for pricing in Nasdaq, 12 June for trading and 1.75 trillion to 2 trillion dollars in valuation areas。

In the Ventuals file, the settlement mechanism for the contract was written, the IPO was opened on the first day, the financial rate was zero, the machine price was set to mark the price, and valuation in real-time stock prices was introduced as an external price constraint. Upon receipt, the tag price was overwritten as a valuation based on the closing price at which all unwinded positions were compulsorily settled。

THIS MEANS THAT ON THAT DAY, ALL SPACEX CONTRACTORS WILL BE SETTLED AT REAL STOCK PRICES. IF THERE IS A LARGE GAP BETWEEN CHAIN PRICES AND NASDAQ PRICING, THE SETTLEMENT IS AN INSTANT ONE-WAY SETTLEMENT。

Analysts estimate that the current gap is about 60 per cent, and the condensation rate will not be smooth, because there was no way before IPO could use SpaceX's real stock to hedge up the chain, and the arbitrage mechanism was structurally broken. Depression rates are expected to occur dramatically in the last 72 hours。

The crash of this price comes from a predictional data error, while the build-up in June of IPO comes from the calibration of real prices, and the extent of the impact depends on the overall size of the open contracts on multiple platforms at that time. The closer SpaceX is to the IPO, the more speculative funds are flowing, the more fragmentation fluidity and the price of distortion will expand simultaneously。

The median margin of $31 will not disappear, they will return with more $31。