Why doesn't anyone buy DeFi insurance

DeFi insurance, which was considered to be an intelligent contract to address traditional insurance denials of compensation, has been difficult in practice to create an effective market due to high risk correlations, erosion of premiums, underfunding and deficiencies in compensation mechanisms。

Original title: Nobody Buys DeFi Insurance

Original by Thejaswini M A, Token Dispatch

Original language: Luffy, Foresight News

"Safety is a trick," almost everyone in the market agreed。

This is what everyone thinks. Sinnox has developed an algorithm that allows direct denial without review of medical records. The United Health Insurance Corporation, after the expiry of the period set in the algorithm, stopped paying for the care, completely disregarding the medical advice of the attending physician. The business model of traditional insurance has always been the collection of customer funds, the retention of high shares from them, and the establishment of layers of thresholds that hinder the settlement of claims。

ALTHOUGH BANK DEPOSITS ARE NOW GUARANTEED BY THE FEDERAL DEPOSIT INSURANCE CORPORATION (FDIC), THE MAXIMUM AMOUNT PAID IS ONLY $250,000, A STANDARD THAT HAS HARDLY BEEN ADJUSTED SINCE ITS ESTABLISHMENT IN 1934. THE VOUCHER ACCOUNT IS GUARANTEED BY THE SECURITIES INVESTOR PROTECTION CORPORATION (SIPC) WITH A LIMIT OF $0.5 MILLION, AND ONCE THE ACCOUNT ASSETS HAVE EXCEEDED THAT VALUE, THE GUARANTEE IS VOID. THE LEVEL OF PROTECTION IN THE PUBLIC PERCEPTION IS FAR FROM REAL, AND THE CEILING ON COMPENSATION PAYMENTS IS SET ONLY UNILATERALLY BY INSURANCE COMPANIES。

DeFi insurance would have been expected to address this painful point once and for all: removing intermediaries, provided that the terms of smart contracts are triggered, automatic enforcement of compensation payments, and eliminating the space for artificial malicious denial of compensation。

But the reality is that almost no one pays. Insurance premiums can significantly erode financial gains and, after deduction of premiums, the remaining gains simply do not match the investment risks borne by users。

This paper will explain the current state of the market and why it is difficult to reverse the core causes of the hardship even if everyone wants to address it。

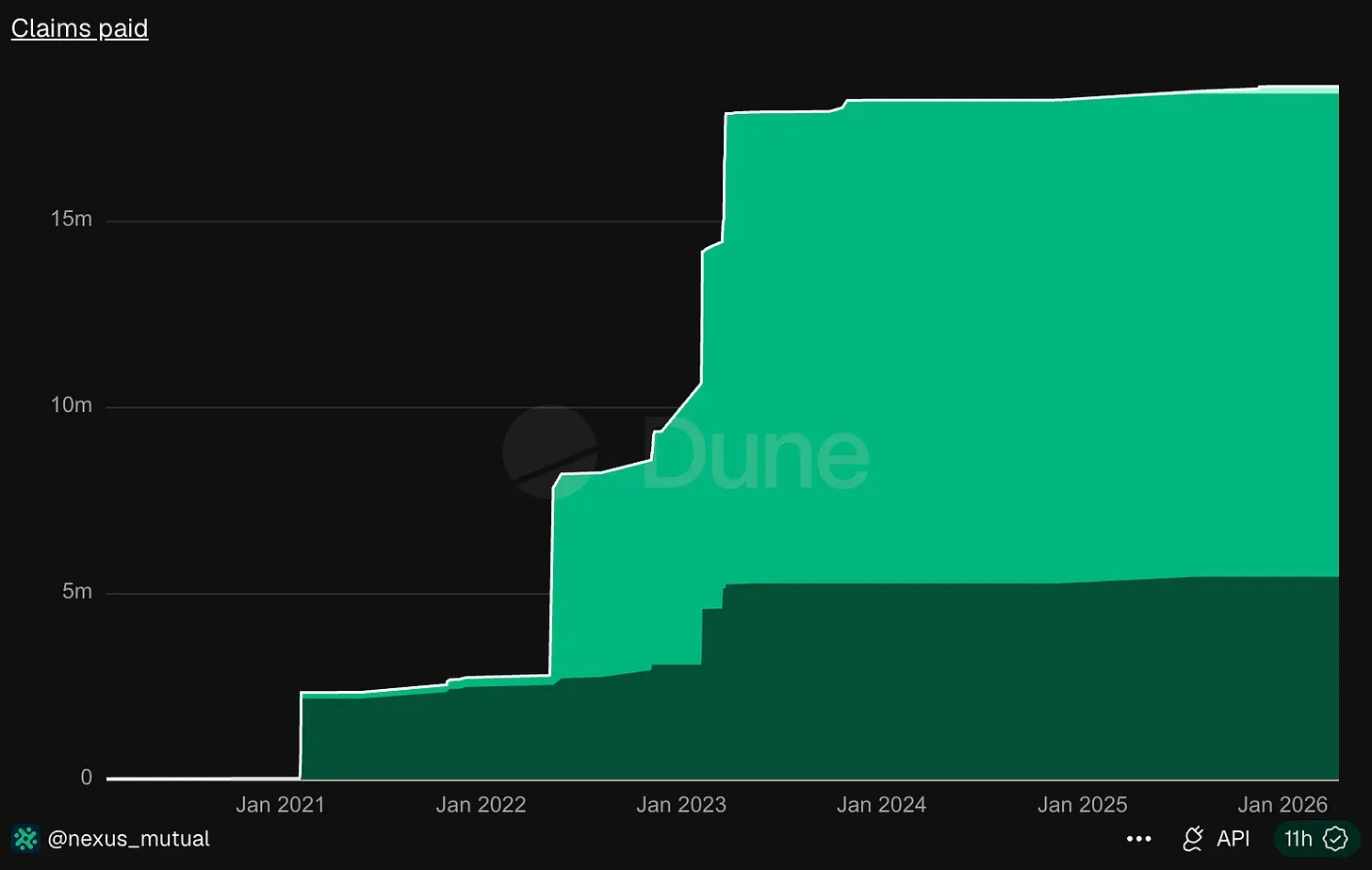

Nexus Mutual is currently the largest DeFi insurance service provider, with a cumulative total of just over $18 million since its inception in 2019。

Source: Dune Analytics

In April 2026, Kelp DAO was subjected to hacker attacks, with losses amounting to $292 million. The amount stolen in this case alone is 16 times the amount of the seven-year Prime Minister ' s compensation for this head insurance institution。

This and the status quo of the crazy denial of compensation by traditional insurance have become extremely different. Traditional insurance collects high premiums, but it does everything in its power to block settlement; and DeFi earns very little, owing to the fact that few investors are willing to take out insurance。

Traditional insurance can operate in a stable manner, with risks at its core not linked to each other. The fire in one house did not cause damage to other homes. Insurance companies can sell insurance policies to 1 million users, and a single fire settlement can be fully covered by full premiums. However, DeFi does not have such a risk-segregation mechanism: predicting a malfunction, security incidents such as a breach of the cross-chain bridge, and then ripping off all the pools and lending agreements that depend on the bottom asset. In March 2023, when the USDC broke down, all agreements to use USDC as collateral were affected. For DeFi, the risks are highly correlated, the insurers can only bet on losses caused by safety incidents, and the pool is sufficiently funded to cover the background。

In March 2023, the Euler Finance stolen $197 million and the chain risk spread rapidly: angle Protocol lost $17 million for holding Euler liquidity tokens, the emergency closure of Yield Protocol and several other platforms, such as Inverse Finance, were also affected。

When security gaps occur in agreements, they tend to spill over to multiple projects, and single-day extreme accidents can even directly exhaust the insurance pool to pay for the entire stock。

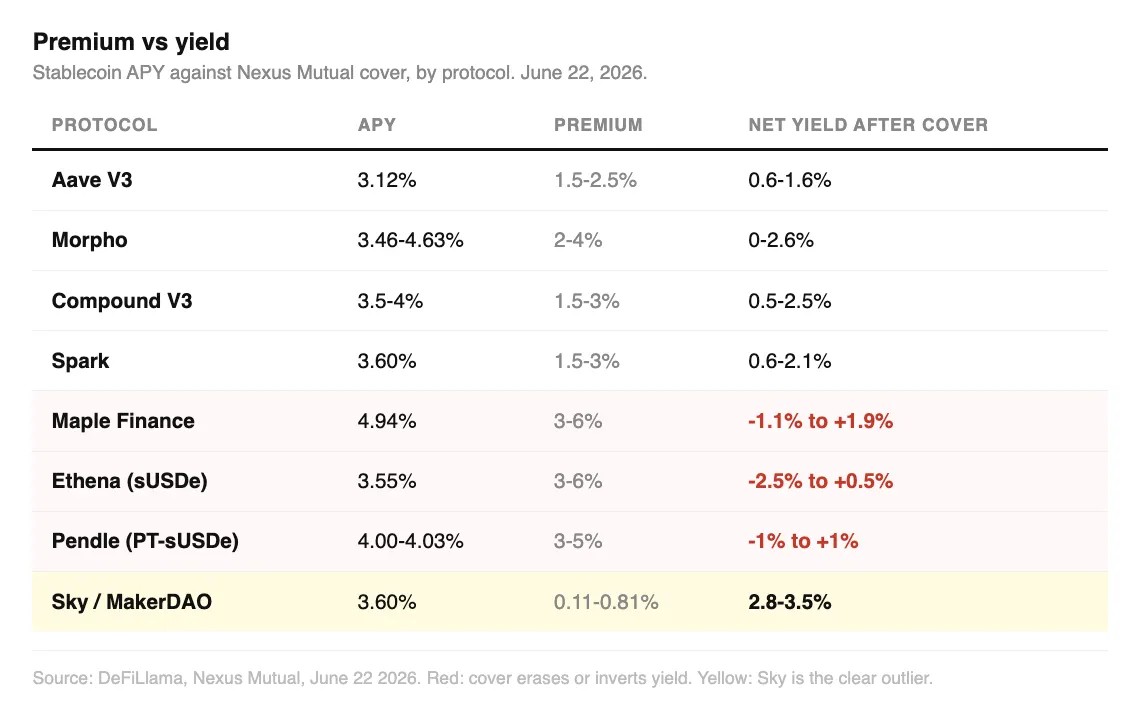

I have collated the current premium rates for Nexus Mutual, InsurAce, compared to the original annual chemicalized benefits of the insurance agreement: USDC annualized earnings from Aave V3 deposits of about 3.14 per cent, the insurance coverage of 1.5 per cent to 2.5 per cent, and net earnings after deduction of premiums of only 0.6 per cent to 1.6 per cent. Investors run the risk of chain security and ultimately earn only slightly more than ordinary bank savings。

Morpho, Compund, Spark earnings are similar, with an annual chemical yield of 3.5 per cent to 4 per cent and a premium of between one third and one half of the earnings, with a very low value for money, although still a small profit。

The annualized earnings of the Maple Finance institution's lending pool are 4.7 per cent - 4.90 per cent, while the insurance rate is as high as 3 per cent - 6 per cent, and net benefits after insurance range - 1.1 per cent - 1.9 per cent. Ethena ' s annualized earnings of 3.6 per cent - 4 per cent, the premium of 3 per cent - 6 per cent, the net earnings - 2.4 per cent - 1 per cent. In these two types of platforms, insurance is purchased and, in extreme cases, the principal of the investor is even lost。

Only the former MakerDao (Sky) was visible. The annualization of savings products is 3.6 per cent, with a minimum insurance rate of 0.11 per cent, which is generally recognized by the market as the lowest risk criterion in DeFi, with net earnings maintained at 2.8 per cent - 3.5 per cent, with the vast majority retained。

While premium pricing strictly corresponds to the level of risk, the emerging platform premium is too high and directly consumes the high returns sought by users。

It is not lazy or reckless for encrypted investors to opt out of insurance, and they know that in most cases the purchase of insurance is equal to zero. Even if all DeFi depositors choose to take full insurance coverage tomorrow, the entire industry will not be able to absorb the demand: the total pool of Nexus Mutual is about $81.56 million, with industry-wide effective insurance coverage at the highest level of $81.5 million, while major agreement lock-in assets are at hundreds of billions of dollars, with a gap between supply and demand。

In the event of a large-scale security accident at the Kelp DAO level, a single settlement would simply empty the vast majority of insurance reserves in the industry。

The total historical settlement of $18 million had exposed the vulnerability of the industry pool, and the market as a whole had never experienced a particularly high-risk event sufficient to penetrate the underwriting reserves。

After the user has filed an application for settlement with Nexus Mutual, it is up to all platform-holders to vote on the award. Members who voted in favour of the settlement would lose their assets directly if the settlement failed. This mechanism is a natural cause of refusal of compensation. Traditional insurance specifically creates a balance between insurers and claims commissioners, while DeFi design combines ownership responsibility with the same group。

PRIOR TO THE 2008 FINANCIAL CRISIS, FINANCIAL RISK-PRICING AGENCIES WERE GENERALLY OF THE VIEW THAT A CRASH IN THE PRICES OF HOMES ACROSS THE UNITED STATES WOULD NOT HAVE OCCURRED, AFTER ALL THEY HAD NEVER EXPERIENCED IT. AIG, THE INSURANCE GIANT, SELLS THE RISK GUARANTEE CONTRACTS ON A LARGE SCALE, AND WHEN THE MARKET CRISIS REALLY BROKE OUT, IT WAS COMPLETELY UNAFFORDABLE。

UNTIL THE UNITED STATES GOVERNMENT INTRODUCED AN INSURANCE POLICY FOR FDIC BANK DEPOSITS, THE GENERAL DEPOSITOR DID NOT HAVE ANY ASSET SECURITY. THE GREAT DEPRESSION HAS FORCED THE GOVERNMENT TO IMPOSE BANK INSURANCE, WHICH IS SET AS THE MANDATORY COST OF OPERATING THE BANK。

In the area of DeFi, no one is able to enforce agreements such as Aave, Morpho to purchase insurance, no smart contract deployment is permitted, and no subject can impose risk security on the project, which also leads to a lack of industry-wide bottom-up mechanisms to counter extremes。

The three largest settlements in the history of Nexus Mutual were approximately $7.3 million in two instalments for the FTX thunderstorm, $5 million for the theft of TribeDAO and $3.4 million for the Euler Finance hacker attack. Together, the three amounts are almost equal to the seven-year cumulative total of $18.6 million for the platform。

The mutual insurance platform has now begun to shift to risk pre-emptive controls, and the joint Immunefi, Cantina, Sherlock and other security audit agencies have launched the gap guarantee product, with only 20 per cent of the key gap bonus on the part of the parties to the agreement, with the remaining funds going under the Nexus Mutual, pre-financed to motivate white hat hackers to clear the breach and avoid theft from the source. At the same time, Nexus Mutual is in the process of deploying a compliance insurance warehouse, attempting to re-insure the encrypted risk to re-insure the pool by introducing a larger volume of external capital to supplement the insurance capacity。

In March 2025, Cantina went a step further by launching the independent original agreement guarantee product, even though the loophole was not detected in advance by the bounty hunters, the user of the agreement could still be compensated after the hacker attack。

Both of the above-mentioned transformational actions essentially recognize a core reality: the lack of ownership of the chain to cover the risks of the chain. The three hard wounds cannot be eradicated because the pool is too small, the risk is highly correlated and the claimant is in the same group as the provider。

Nexus Mutual ' s lockdown at DeFiLlama amounted to $81.56 million, representing 85 per cent of the market share of the entire DeFi insurance track. The remaining peers continue to shrink: the peak locker of InsurAce, $150 million, leaving only $1.32 million, with only one major settlement completed after the fall of the UST in 2022; the Sherlock pool shrinks from $60 million to $505 million a year; and Unslashed Finance, millions of dollars, is trapped in old codes that stopped being updated at the end of 2024. The remaining insurance items were either completely closed or the business track was changed。

The lighthouses, which alert all ships to the reef, are unable to collect user fees from ships passing through, making it difficult to obtain voluntary funding for the construction of the lighthouses. The benefits are shared by all, while the costs are borne by the builders alone。

The value of DeFi insurance is precisely to prevent the chain of accounts from stepping on the spread of the crisis. Encrypted market assets are highly interconnected and overall market stability can be maintained only if the owners are insured simultaneously. But if everyone expects others to take out the insurance, and they are not willing to bear the cost of the premiums themselves, there will eventually be no insurance and a risk protection system will be put in place. No one can protect any assets without a proactive safeguard。

Original Link