Early British Wida investor Gavin Baker ' s investment philosophy: making multi-AI infrastructure bottlenecks and empty overall market risk

AI IS NOT IN THE BUBBLE; ON THE CONTRARY, IT IS IN A SUPERCYCLE。

What the Best AI Investments Are Buying Right Now

Source: Limitless Podcast

Original language: Deep tide TechFlow

Edit Guidance

The podcast focused on the investment philosophy of the founders of Atreides Management, long-term bets on Nvidia and Cerebras investors, Gavin Baker。

HIS CORE JUDGMENT IS THAT AI IS NOT A BUBBLE, BUT A CYCLE OF INFRASTRUCTURE SUPERCYCLES DRIVEN BY POWER, CRYSTAL CIRCLE AND COMPUTING; REAL EXCESS RETURNS ARE NOT IN LARGE MODELS OR CHAT ROBOTS, BUT IN GPU CONNECTIONS, MEMORY, REASONING CHIPS, ADVANCED PROGRAMMING AND POWER SUPPLY LINKS。

Gavin Baker, while guarding against the fall of the entire market through QQQ put, focuses on Astera Labs, Unity, Micro, Nvidia, Cerebras, Positron, etc。

AS LONG AS TSMC, ASML, HIGH BANDWIDTH MEMORY AND ELECTRICITY GRIDS ARE NOT QUICKLY SURPLUS, AI CAPITAL SPENDING IS NOT NECESSARILY A RE-EMERGENCE OF THE INTERNET BUBBLE IN 2000。

Expensive Notes

AI FOAM OR SUPER CYCLE

• "AI IS NOT IN THE BUBBLE; ON THE CONTRARY, IT IS IN A SUPERCYCLE."

• "The greatest return is not in SaaS, not in chat robots like OpenAI or Anthropic, but in electricity, computing and silicone."

• “This is not an Internet bubble, because buyers are mainly the smartest and most cash-flowing companies in the world, and they do not rely on debt leverage for their credit”

• “If the entire market cannot be oversupplyed, it will be difficult for it to collapse like the traditional bubble”

real bottlenecks: electricity, crystal circle, token

• “Gavin’s theory is simple, looking only at the infrastructure bottlenecks of AI, who can do high per watt and lower the cost of token.”

• "AI Labs are increasingly concerned about one thing: how much token can be generated per watt."

• “ELECTRIC POWER AND THE CRYSTAL CIRCLE ARE TWO BRICK WALLS AND TWO KEY CONSTRAINTS LIMITING THE FAST PACE OF AI”

From pre-training to reasoning and post-training

• “The fact that the model has been pre-trained does not mean that it will be a genius throughout its life; it will also need to absorb new information at the post-training stage”

• “The essence of reasoning requires extensive computation, which is why the reasoning chip and the reasoning infrastructure will be the focus of the next phase”

• “Only the costs or income opportunities associated with reasoning may be 5 to 10 times the input of pre-training capacity”

Small vertical models, end-end models and sovereign infrastructure

• "You don't have to interact with Claude every day in the future; what you might really need is an AI proxy based on your own data training."

• “The pace of infrastructure deployment is itself a moat, and the digital world is more iterative than physical infrastructure is built”

"WHOEVER CAN COMPRESS THE PHYSICAL DEPLOYMENTS THAT CAN BE DONE FOR MONTHS OR YEARS TO WEEKS, CAN SELL HIGH PRICES IN AI CAPITAL."

Gavin ' s investment approach: making many bottlenecks and emptying overall market risk

• “He strongly believes that the AI winner will come, but that does not mean that he is optimistic about the whole market; QQQQ put is his hedge against the overall downside risk.”

• “TSMC ACTUALLY LIMITS THE SPEED AT WHICH FOAMS ACCELERATE; CAPITAL EXPENDITURE IS NOT EASILY OUT OF CONTROL AS LONG AS THE CAPACITY OF CHIPS CANNOT EXPAND IN AN INSTANT”

• “Gavin is like an older, more stable, more cyclical Leopold: the former is a decade of success, while the latter is now more quarterly.”

AI SUPER-CYCLE ASSETS WORTH BETTING

EJ:Gavin Baker is an AI investor who is extremely productive, but hardly ever heard of by the public. Over the past 20 years, he had started investing in some of the then known AI companies before they went into circles. He was in early Nvidia (in Weida, AI GPU and the Accelerator Nucleus) and Cerebras (AI Chip) and had a very clear idea that AI was not a bubble, but rather a supercycle。

In his view, critical bottlenecks and constraints could be identified by observing the bottom infrastructure of Watts, waffers and token, i.e. AI. His conclusion is simple: the biggest returns in AI come from power, energy and silicon manufacturing, not much to do with SaaS software or service, not much to do with chat robots like Anthropic and OpenAI。

In the end, the entire industry will be sent downstream to semiconductors, i.e. the picks and hovels that support the entire AI industry。

WHEN A LOT OF PEOPLE SAY THAT THE AI INDUSTRY IS ALREADY A BUBBLE, HE THINKS IT IS PRECISELY AN INTERGENERATIONAL BUY-IN OPPORTUNITY, ESPECIALLY FOR AI INFRASTRUCTURE. HE EXPRESSED THIS JUDGEMENT IN THE FUND ON A SCALE OF ABOUT $4.1 BILLION。

And if you hear the constraints he's talking about, especially the AI infrastructure, you'll find this theory familiar. We've talked about this many times before on the show about an investor, Leopold Aschenbrenner, who has made a lot of arrangements in the same direction. The difference is that Leopold has been doing it for about three years, and Gavin has been doing it for over 20 years。

Leopold's management assets are about three times as large as Gavin's, but the producer, Luke, warned me that: You might be able to beat Warren Buffett in a year, but can you run him for decades? Gavin Baker ' s historical record suggests that he may have a different perspective on this investment theory。

Those who don't know Gavin Baker can first know that he is the founder of the Atereides Management (Investment Fund) and has been investing in Nvidia for the past 20 years. If you hold Nvidia for 20 years, it's already incredible, because it's supposed to be very impressive。

Some of his recent successes include Cerebras and Astera Labs. Cerebras is an AI chip company whose post-IPO valuation was mentioned as alarmingly high. And there are companies that you may not have heard of, and we'll follow his combination and judgment in this set and see where he thinks AI's investment opportunities are。

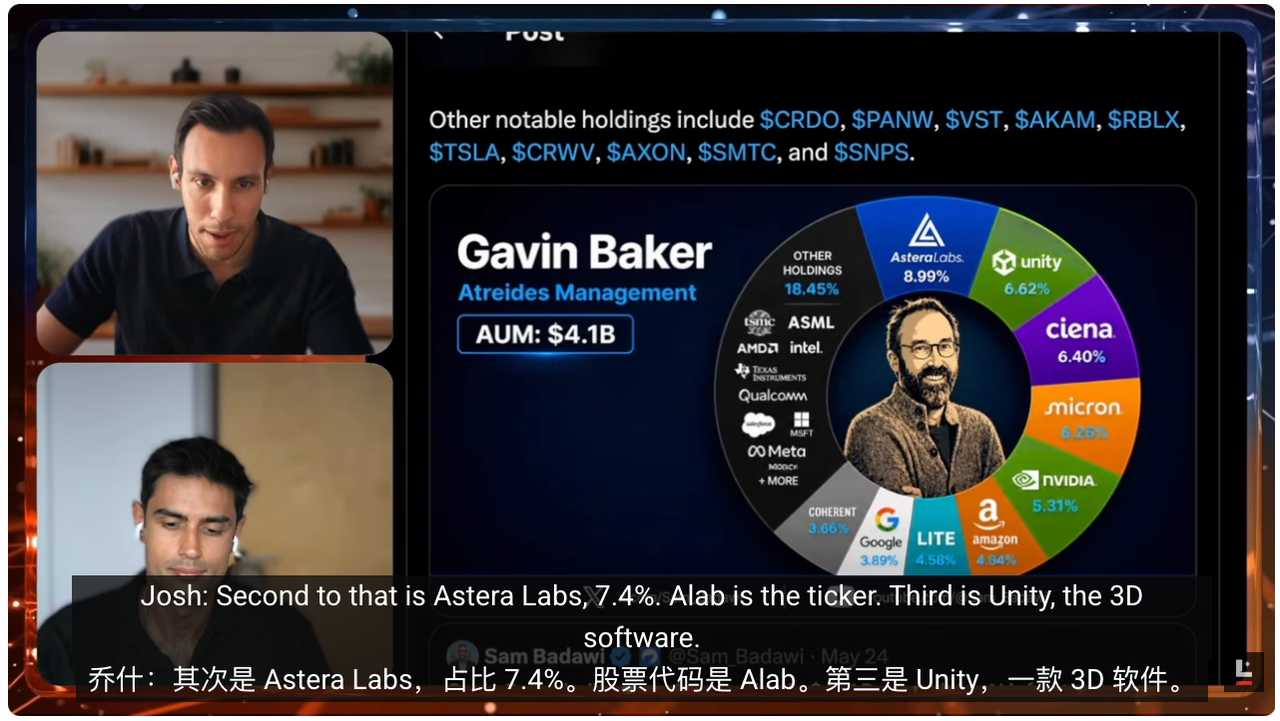

Then the question becomes, what did he vote for, why? If you look at the latest 13F (quarterly warehoused disclosure by United States institutional investors), the fund is approximately $4 billion AUM (asset management scale). Dismantling some of its biggest holdouts will reveal that these companies point to the AI development bottlenecks that Gavin has repeatedly mentioned。

He's got a lot of space in companies that aren't sexy and many people haven't even heard of. Astera Labs, for example, accounts for almost 9 to 10 per cent of the fund. You can interpret Astera Labs as a connection layer between GPUs。

If a data centre is conceived as a system, GPU is an engine responsible for pre-training, post-training and inference of models. For GPU to work, however, it has to transfer a large amount of data between them and access the memory chips (RAM chips) where the data are stored。

To do that, we need a pipe system. I'm talking high-level, because I don't pretend I know all the bottom details. Astera Labs solved the problem. When AI clusters extend to hundreds of thousands of chips, bottlenecks are no longer just GPU itself, but data transfer windows, how to send correct data at the right time and access correct data. Astera Labs built a plumbing system like this。

I've never heard of Astera Labs before I studied this episode. But I remember Cerebras was in a similar situation. Gavin spoke about Cerebras about six months ago, and given the timescale of AI, six months is long. Then it was IPO, and the show mentioned an estimate of about $60 billion, and IPO went up by 40 per cent. This suggests that Astera Labs may be an important name in a similar trend。

Josh:Cerebras is his very early investment. He entered Cerebras early in the company ' s life cycle, meaning that he had been betting on the theory for many years. Several other companies were also on his long-term bets, of course Nvidia。

It's amazing to be involved in Nvidia for more than 20 years and to stay on the road. I recently listened to two podcasts from Gavin, and he clearly expressed a judgment when he spoke about Nvidia's position that he believed that Nvidia could continue to maintain its current profitability and demand. That means that he thinks that Nvidia has the chance to move closer to the market value of $10 trillion, and it's only halfway through。

Another noteworthy development is Micron. We talked about the AI Investment Bank in the last episode, and the position of these companies in it, and we strongly recommend that you go back. Micron is one of the biggest memory makers。

an amazing figure is mentioned in the show: it was worth less than $100 billion a year ago, and it was recorded as having surpassed the market value of $1 trillion 10 times a year. this shows how important it is for memory program。

There are companies that are not so visible but interesting. EJ, I'd particularly like to bring you one: Unity Software. People who are familiar with games know about Unity, it's a game engine, and many hot games are made with 3D rendering software。

So why would an AI investor vote for Unity, this "a video game thing"? The answer is a 3D game engine. Unity, a world model builder, has a deep understanding of physics, the way the world operates, materials and light。

When AI is going to build AGI and Humanoid robots, an important link is the simulation of virtual environments and virtual data sets, where robots are trained. Unity happens to be one of the strongest tools。

So, as a world model believer, you're going to like this example of a company that's known as an engine, with a clear path to becoming an important player in the AI world。

Gavin ' s investment theory and strategy

EJ:the theory of world models is simple: the current AI model or LLM understand the world mainly through text and books, like a student sitting in a library, but it has no real world experience。

That's what the world model wants to unlock: put a game role in the simulation environment and make it understand how physical reality works。

Like, what happens when I throw my phone down or kick a ball? What's next? What should you do? The world model solves this problem。

At present, there are not many players who can do this on a large scale. Now the lead might be Google, which has a model like Genie 3 (Google's Generable Interactive World Model project). The program also mentions Google's recent release of Gemini Omni, but these models have yet to really reach their ChatGPT moment。

What I like about Gavin is that he's like a barbell. On the one hand, it's tradition, you need GPU, you need storage, so he's throwing the biggest players, Micron and Nvidia. The other side was forward, and he thought puck would go there, so he voted Cerebras, because he thought reasoning was important; and Unity, because he thought that the world model would be the way to train robots and the next generation of LLM in the future。

He also has Positron, which does inference chips. If it sounds like Cerebras, yes, they all revolve around reasoning. Gavin recently spoke repeatedly in interviews about the trend that the infrastructure warehouse of the AI model, especially the training warehouse, is shifting from pre-training to more emphasis on post-training。

If you're in the AI circle, you'll know this turn has happened. Gavin's very focused on this. A model still needs to understand new information, new data and to update itself. It can't be considered a genius for life because it's pre-trained on a data set. It also requires learning new information, which takes place at the post-training level and which requires extensive computing。

Second, if you need an AI model to really think about it, just like we'll think when we get the new information, does this angle work? Is there another theory to explain? This is resoning. The reasoning also needs to be calculated extensively. It is now estimated that the cost or income opportunities associated with the reasoning alone may be between 5 and 10 times the input of the pre-training calculator。

So both AI Labs and Chip Mackers have made a major shift. You've seen Nvidia put out a lot of reasoning-oriented GPUs to support the application of intelligence. Gavin also expressed a note to reasoning through a series of investments。

Last thing I thought was fun was Gavin talking about China. In the AI competition, narratives have always been China versus US. There is a unique configuration in China, where energy is relatively adequate, and the ability to expand the production of chips. The United States is currently struggling in this area, which is why many links are being outsourced to TSMC (the world's most important state-of-the-art crystal circle plant) in Taiwan, China。

His explanation was that China had a unique opportunity to create an AI infrastructure or chip that was very different from that of the United States, because they would be very focused on reasoning. You can say that Gavin is taking the lead in building the infrastructure of American reasoning through his investment in America. I think this future may be a great opportunity。

Josh:It is worth noting that this bet is not only on top. He also holds a large QQQ put position. QQQ is the ETF that tracks the Nasdaq 100, a basket of stocks and the second largest trade in the United States. It performed very well: 55 per cent in 2023, 25 per cent in 2024, 20 per cent in 2025 and 17 per cent to date in 2026。

In other words, QQQ was very good as an index fund, and it was easy to buy it, and it was the top 100 baskets of stocks. And Gavin is making a reverse hedge with it. He is not saying that AI will not win, but that he will vote for the key maker of the real bottlenecks, but he is not very optimistic about the overall market sentiment。

QQQ put is downside protection: if the whole market collapses in an unfavourable way, even if AI wins for a long time, he has this layer。

Four types of investmentable directions

Josh:we can break down what he considers to be the most important investment bottlenecks. the first is the verticalized small language model。

Ordinary LLMs, such as Claude and ChatGPT, are basically LLM, which have a broad understanding of the world and can answer specific questions. But training models around a particular vertical area or a particular problem are another matter。

These particular problems usually exist in enterprises, especially those that are deep-growing on a particular issue, or those that form niche (Liki) in a particular subdivision. Verticalized SLMs (Postal Small Models) solves the problem: They are front-line models, but highly optimized to operate efficiently on enterprise-specific data or locally in device (equipment)。

we talked about on-device or local run models. the reason is that there is a lot of very personal data on your cell phone or other devices, and you may not be willing to hand it over and the company may not be able to access it. for example, medical records, financial details。

I saw OpenAI issue a financial AI agent that can access your bank account, but can't really operate on your behalf, because there's a lot of personal information, such as social security numbers, bank details。

Local models or SLMs can solve such problems. Gavin is a big bet that they will become important in the future. There's a company he really likes: Apple. While he may not have expressed a clear interest in investment, he believes that Apple would be one of the main factors that would allow local models to operate on equipment。

If this is the future, we may not think that Claude must be your interactive model every day. What you might need is a personalized AI agent, which is trained on your own data, and that's what SLM could eventually become。

the generic version can run on your mobile phone, and a large number of companies can run highly optimized, specialized models and train on their own proprietary data to better sell or market products。

EJ:Apple's great at this position. I look forward to WWCC, which is almost there。

Josh:Yeah。

EJ:JUST A FEW WEEKS BEFORE THE APPLE DEVELOPER CONFERENCE, THEY WILL RELEASE NEW AI SOFTWARE AND HOW IT IS INTEGRATED WITH HARDWARE. IT WILL BE VERY IMPORTANT, AND WE WILL CONTINUE TO COVER IT, AND I LOOK FORWARD TO DISCUSSING IT。

Josh:The second pillar is sovereign infrastructure. We often say that bits (bits) are much faster than atoms. See, AI infrastructure is clear: model quality is almost exponential, and every watt generates intelligence, every token's corresponding intelligence, only up。

But the pace of physical deployment did not rise at the same pace, which is itself moat. Hardware is extremely complex and transistor accuracy is near the atomic stage; it is not easy to deploy on a large scale in a world where existing infrastructure is already under pressure. With the accelerated spread of electric vehicles, the electricity grid has become more stressful and in many places is approaching full capacity. Now AI also brings in energy problem and chip problem。

Gavin has a strong stake in the fact that infrastructure is difficult and that construction takes many days, months and even years. He's betting on people who can compress the cycle to weeks. So the speed of physical deployment is itself a moat. He was narrowing the target and looking for companies that could deploy as soon as possible。

The first example I'm thinking about is SpaceX, and the speed at which they built and leased Colossus to Anthropic, possibly to other companies in the future. This infrastructure pillar is one of Gavin's key concerns。

If you look at Leopold's combination, this is the core. The reality is that building is very difficult and those who can build it can sell it very expensive. It says that SpaceX is now the biggest source of income for renting data centres, not rockets. This illustrates how important this pillar is。

EJ:He's concerned with speed, but he's also concerned with costs. He repeatedly referred to one indicator: per watt performance. What he's really trying to say is that AI's lab is increasingly concerned about how much tokens are produced per watt。

If you want to think that only about five companies spend billions or even trillions of dollars on GPU, compute and the power that drives these systems this year, you'd want bang for duck to be high enough. In particular, costs are at the heart of the problem when hypers (super-large cloud manufacturers) expand to this scale。

Hypothetically: I asked Claude a question, and it gave me two cents to answer; I asked ChatGPT a question, and it gave me a dollar to answer. Even if Claude had only ChatGPT 95% intelligence, I would probably use Claude. Because I can ask more questions and eventually get answers at lower cost。

So the cost of accessing this intelligence is very important. Just this week, Microsoft and Uber announced that they were actually reducing the use of Claude Code, because the annual budget was about four months old。

You can see this in Gavin's portfolio: Cerebras, Positron, Astera Labs. He identified very disaggregated infrastructure bottlenecks and then made a simple bet: If this company solves this bottleneck, reaches a certain level, token costs drop to a certain level, then AI Laboratories buy more GPUs, more products or more of this kind。

So his theory is really simple, despite the complexity of the technology: I'm only concerned with the infrastructure bottlenecks at the AI level. If we can find a company that can improve each watt's performance and make tokens cheaper, I'll bet it's worth a lot of money in the future, either IPO or bought it at a high price。

Josh:In this section, if anyone wants to copy Gavin's deal, several names need to be known: Astera Labs, Cerebras, SiFive (RISC-V Chip Design Company) and Positron. These four companies are key in this plate。

the fourth and last direction is the combination of energy and space. as we said earlier, there is a great deal of constraint on energy supply, and new energy is very difficult. the show mentions a statistic that about 40 percent of the new data centres will encounter very strong opposition to lobbying, protesting and not wanting to land them。

There are two types of solutions. One type is out-of-the-box energy, that is, portable energy. You can take the data centre and power it with a small energy device. Leopold's pretty good at Blue Marble。

The other is the orbital computer, which is the direction Gavin is now very concerned about. The largest and most central company in this field is, of course, SpaceX. It is the only company that has the capacity to become a highway to space, to put the Payload (load) in orbit, to put the racks and data centres on low-orbit and to generate sufficient intelligence and power back。

I think SpaceX means more than SpaceX itself. I'm a little surprised that Gavin's combination doesn't have more space stocks configuration, considering that he thinks it's a huge industry. Maybe the reality is it's too early, and SpaceX is the linchpin that unlocks the industry。

Next, watch closely the Starship V3 launch. We just saw a Starship launch last week, doing well. If Starship can't really work, there's no space energy, no racks to orbit. It is a necessary condition because the payload to launch is very large. So SpaceX must be the company that has to focus on, although there'll be a lot of second-class companies that will be affected。

Why not another Internet bubble

Josh:Then you'll have to ask why this is not just another dot-com bubble? Gavin was asked this question many times, and he gave a very strong answer, and I basically believe him and his argument is convincing。

his logic is that the internet bubble in 2000 was debt-fueled. many have borrowed large amounts of money to invest in untested theories and products that no one really uses or cares about。

If it compares it to what Gavin now calls the AI Super Cycle, it is expected that only OpenAI and Anthropic companies will reach $200 billion this year. And it's not fake money, it's money that's been signed through a contract, and a large part of it, the show says 40 to 60 percent, has been prepaid by businesses and retail customers。

In other words, real money is moving。

And look at GPU algorithms, don't look at model laboratories, see who's buying products from Nvidia. Google, Microsoft, Amazon and Meta are all paying from their own cash reserves without borrowing. Amazon just went to the end of the free cash flow, and if they start borrowing money, we can worry. But the point is that they are not leveraged。

And these are one of the top five companies in the world, and in a sense one of the smartest because of their market value, size and status. Compared to the Internet bubble, a large number of anonymous companies were able to melt money and then burn it in a very unreasonable way. In this cycle, it is the smartest group of companies in the world that spend with no leverage。

The quarterly reports that we have given on the programme in recent weeks also show that profits are optimizing around these moves, and models are advancing and becoming smarter. So Gavin's central argument is: it's not an Internet bubble, because it's not leveraged; at the same time, the bottlenecks we're talking about are bound by physical atoms。

It's one thing to buy a bunch of memory chips and GPUs, but Nvidia can't oversell GPU, and Micron can't oversell AI storage chips because they don't have enough chip production facilities. So his simple argument is, if you can't oversupply the whole market, it's not a bubble. We're limited to not having enough picks and shots to do this, and that's what he's voting for。

And a good point: Gavin thinks that if TSM could supply, Nvidia would have sold $2-3 trillion GPU this year and next year. In other words, TSMC is a key link in the foam boundary。

The reason is that if TSMC could meet the needs of these companies and provide them with so many chips, it would cost them a lot of money. There is no significant disconnect between CapEx (capital expenditure) and operating cash flow, and the cash generated by the enterprise is still sufficient to support construction。

But if TSMC says to Nvidia tomorrow, we can triple the capacity overnight, and Nvidia won't refuse, it'll start spending a lot of money buying chips. Other companies will also be forced to borrow money to purchase the chips, when CapEx Bubble (capital-expenditure bubble) becomes larger and separates the cash flow from business operations。

BUT BECAUSE OF SUPPLY CONSTRAINTS, STORAGE RESTRICTIONS, CHIP MANUFACTURING RESTRICTIONS, ENERGY CONSTRAINTS, ESPECIALLY ON ADVANCED CHIPS, WE CAN'T ACTUALLY MAKE CONSTRUCTION AS FAST AS POSSIBLE. SO, TSMC BLOCKED THE BUBBLE ACCELERATION。

Growth is relatively sustainable as long as the capacity of TSMC chips remains limited and as long as Samsung and other chip manufacturers do not exceed their market share. It seems fast, but there is still a great deal of need that cannot be met, because we are not built fast enough. As long as this dynamic exists, I don't think it's a big deal。

EJ:AND ONE MORE THING, YOU CAN'T ASSUME THAT NEEDS ARE STILL, BECAUSE IT WON'T. AI DEMAND IS GROWING EXPONENTIALLY AND FASTER THAN THE PRODUCTION OF THESE CHIPS。

I can think of only two ways to prove this theory. First of all, there's a miracle of replicating ASML, and suddenly there's a bunch of ASML competitors. People who don't know ASML can understand that it produces machines worth about $400 million, which are needed by TSMC and all major chip fabs。

According to the show, only one team made these things in Norway (Norway) and had a very long cycle, and the order backlog had been scheduled for about five years。

SECONDLY, WE CREATE A COMPLETELY DIFFERENT TYPE OF LLM, WHICH DOESN'T NEED SO MANY GPUS OR SO MUCH STORAGE. BUT WE HAVE NOT SEEN SUCH SIGNS AT ALL。

I saw a story today about SK Hynix. It is the Nvidia GPU's number-one store manufacturer and supplier, and almost top dog in the AI storage area。

It is now receiving about $50 billion to $100 billion from Google and Microsoft, two companies that want to pre-lock supplies to be produced over the next three years to pay for the equipment it needs to expand its production。

This shows how hungry these big companies are for storage, which is just a track in the AI component. SK Hynix said instead, "I don't want to give you security, I'll just raise the price." Its operating margin is about 70 percent, almost incredible in the semiconductor industry。

So Gavin all-in makes sense. It doesn't look like a bubble. Maybe the market will react in the short term. We opened the stock portfolio today, almost all down, but that was more emotional。

THE POINT IS THAT WE ONLY NEED MORE GPUS AND MORE SEMICONDUCTOR CHIPS, AND NOT ENOUGH SUPPLIES AND NOT ENOUGH MANUFACTURERS。

Gavin portfolio

Josh:The conclusion is: electricity and crystal. Just those two. They are two brick walls and two constraints that prevent us from speeding too fast. As long as power and round power remain valuable, demand is strong and supplies are limited, there are good days ahead。

If you want Gavin's TLDR, I can read his biggest holder. Once again, this is not an investment proposal. That's Gavin holding what, doesn't mean we holding what. I don't know if these stocks will go up, fall or turn around。

His largest position is a little anti-intuitive, and it's QQQ put position. On the whole, his market bias is noteworthy. The second largest is Astera Labs, which is about 7.4 percent of the warehouse, and the picker is ALAB. Third is Unity, which is 3D Software。

There are many others behind this: Ciena (light network equipment), Microon, Nvidia, Amazon, Lumentum (light communications and laserware), Alphabet (Google parent), Coherent (photoelectronics and materials), Roblox (play platform), EchoStar (satellite communications), Twilio (twilight communications platform) and Wayfair (turbator). This man casts everything。

If you're interested, you can see his 13F. That's Gavin's point of view, the bottlenecks in electricity and the crystal round. As long as these constraints remain, they are essentially unilateral increases. EJ, how do you absorb this information? What will you do

EJ:The market has been very volatile since Leopold's 13F came out. When I recorded this episode, I became increasingly aware that Gavin was kind of like an older, smarter Leopold. He's been in this business for a long time. Maybe he didn't have $13 billion AUM, but I feel like he'll be in 10 years。

If you hear this, I don't want to follow AI every minute, every hour, every day, I just want to put the money there and see how it grows in the months or years ahead. That Gavin combination might be useful. Of course, this is not an investment proposal。

He has taken a more cautious, longer-term and future-oriented approach. If his trend judgement finally materializes, as he did in Nvidia and Cerebras in his early days, there may be exponential gains in the coming years. But it's all based on one of his core points: we're not in the bubble。

I wonder if the audience agrees. Apparently, most people don't go down to the bottom like Gavin. But after listening to this episode, do you think we're in the bubble? Or not? What are the grounds for support and objection? Anything we missed? Josh, do you think it's foam till we're done

Josh:I think we're in a bubble of course. The question is, at what stage of the bubble we are at, it can also be discussed. It now looks more like an early stage, so it is hoped that it will continue in that state. According to Gavin, we're fine as long as TSMC continues to limit the capacity of the chip。

That's the whole outlook. We have already spoken of Leopold, whose success is now measured on a quarterly basis; now we speak of Gavin, whose success is measured on a decades-long basis. Many people may have their own answers between them。

Original Link