HOW THE CLARITY ACT WILL RESHAPE A STABLE ECONOMY

The entire stable currency-receiving economy has been forced to replace “observe” with “use of interest-bearing”, while the monetized currency market fund, as a bottom reserve asset, has become one of the most robust revenue-receiving infrastructure in the new paradigm。

Original by: @BlazingKevin , Blockbooster Fellow

ON 14 MAY 2026, THE UNITED STATES SENATE BANKING COMMISSION PASSED THE CARITY BILL BY A BIPARTISAN VOTE OF 15-9。

The most important element of this “legislative progress” is section 404 of the text. This section was redrafted by Senator Thom Tillis and Angela Alsobrooks in a compromise text released on May 1st

First, put an embargo on stable currency gainsExtension to all digital asset service providers (DASPs) and related parties— Includes the Centralized Exchange, the Broker, the Dealer, the Host. GENIUS Act, when signed in July 2025, was bound only by the issuer of "stabilized currency" (PPSI/FPSI). Coinbase, Anchorage Digital Neo Ltd. & nbsp; etc. continued to provide users with 3.5%-5% compliance circuits of proceeds via the "non-issuer" route, all closed by Section 404。

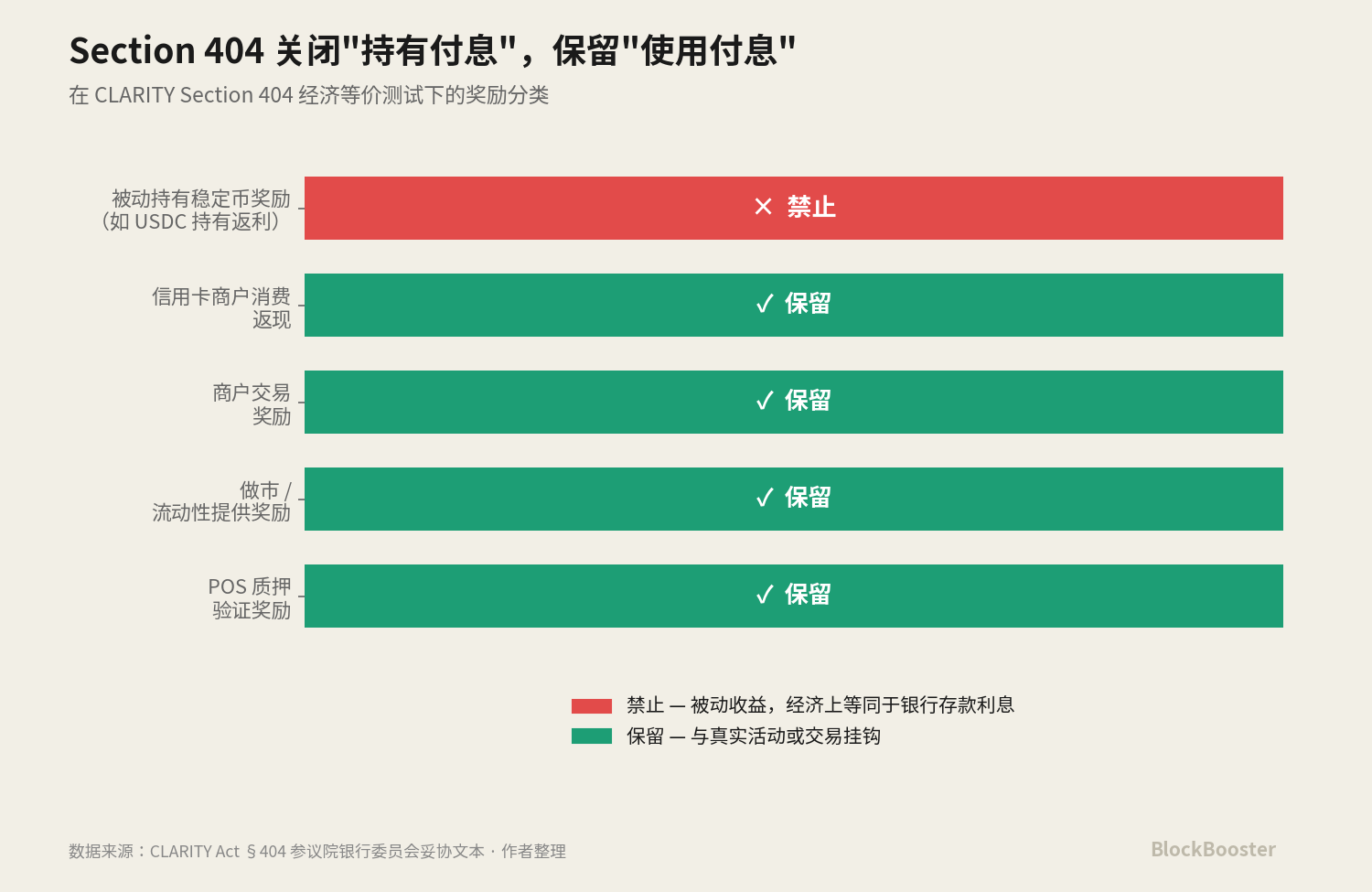

Second, the explicit introduction of the legal dichotomy of “passive proceeds vs activity incentives”. Section 404 prohibits incentives that are “functionally or economically equivalent to interest on bank deposits” — that is, those that are based solely on holding the proceeds that are automatically generated — but retain incentives that are “based on real activity or transaction”, such as pledge, market, credit card consumption return, business transaction incentives。

Together, these two changes make up oneModel conversionI don't know. The stable currency industry is shifting from an interest-bearing market to an interest-paying market。

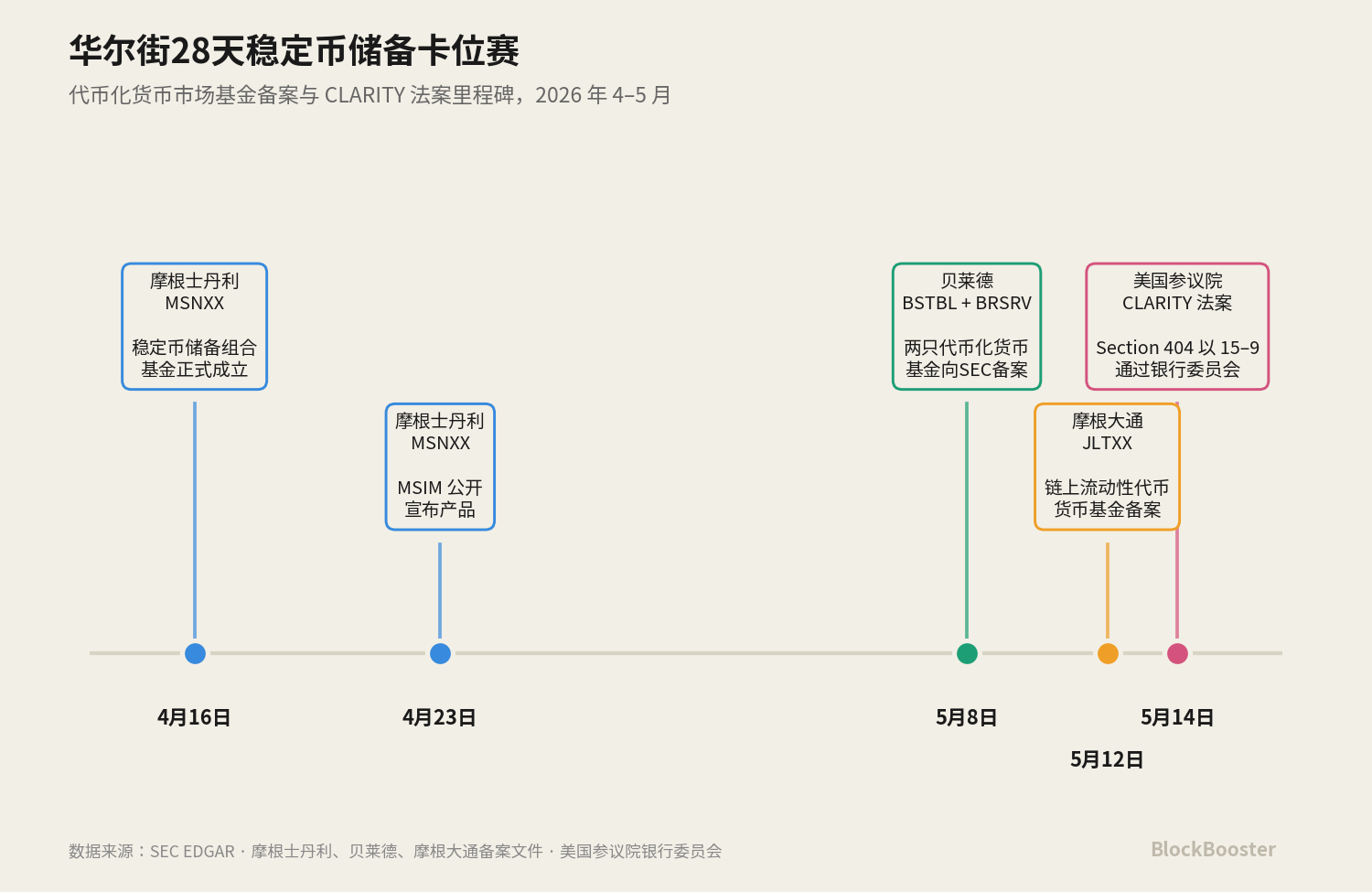

Meanwhile, in the past month, the three largest management agencies on Wall Street (Morgan Stanley, BlackRock, JP Morgan) have almost synchronized the introduction of a currency market fund product tailored to stabilize the demand for currency reserves. Morgan Stanley's MSNXX was founded on April 16, publicly announced on April 23; BlackRock filed two coins at the same time on May 8; and JP Morgan filed on May 12. Three are almost synchronized to launch a similar function within 28 days。

This is certainly not a coincidence. We believe that:CLARTY Section 404 is about to adopt the expectation that the economy of stable currency gains is being pushed to a new paradigm — the hold-to-earn path is being narrowed, the use-to-earn path is being kept, and the monetized money market fund, as a compliance-paying tool for stable currency reserves, is the most robustly benefiting from compliance returns in this new paradigm。

WALL STREET'S CAPITALIST CENTRALISED THE PRODUCT IN APRIL-MAY AS THE INDUSTRY CARD FOR THIS PARADIGM SHIFT. IT NEEDS TO BE MADE CLEAR THAT, CURRENTLY, THROUGH THE SENATE BANKING COMMISSION ONLY, THERE IS STILL A DISTANCE FROM THE PRESIDENT'S SIGNATURE, BUT THE MARKET IS EXPECTED TO BE REORGANIZED IN THIS DIRECTION。

THIS PAPER WILL BEGIN WITH A TIME LINE TO DISMANTLE THE GENIUS-CLARITY RELAY LEGAL STRUCTURE AND ANALYSE WHY THE MONETIZED RESERVE ASSET LAYER IS THE MOST ROBUST COMPLIANCE REVENUE CHANNEL IN THE NEW PARADIGM。

1. 30-day industry Card

1.1 April 16: The opening of Morgan Stanley

Let us go back to the earliest events。

On April 16, 2026, Stablecoin Reserves Portfolio (ticker: MSNXX), Morgan Stanley, was officially established。

23 APRIL MSIM PUBLICLY ANNOUNCED THE PRODUCT。

THE MSNXX PRODUCT IS VERY PRECISE. THE OFFICIAL STATEMENT STATES: “THE FUND PROVIDES A QUALIFIED CURRENCY MARKET FUND OPTION FOR ISSUERS OF COMPLIANT AND STABLE CURRENCY THAT ALLOWS THEM TO INVEST IN THE RESERVE ASSETS NEEDED TO SUSTAIN THE STABLE CURRENCY IN CIRCULATION.”

MSNXX IS A TAILOR-MADE PRODUCT REQUIRING RESERVE ASSETS — INVESTMENT IN CASH, UNITED STATES TREASURY BONDS DUE WITHIN 93 DAYS, AND OVERNIGHT BUYBACKS OF BONDS。

BUT MSNXX IS NOT A MONETIZED PRODUCT, NOT TRADED ON THE CHAIN. MORGAN STANLEY'S PRODUCT STRATEGY IS CONSERVATIVE — PROVIDING ONLY TRADITIONAL MMF PACKAGING, ALLOWING STABLE CURRENCY ISSUERS TO INVEST THROUGH TRADITIONAL FINANCIAL CHANNELS。

This was the first publicly announced “products specially designed for stable currency reserve requirements” of Wall Street’s management giant. It is not revolutionary in itself, but it sends a clear signal that the demand for stable currency reserves is so large that the capitalist is willing to set up a special fund for it。

1.2 8 May: “Dual filing” by Belet

Twenty-two days later, Belet submitted two simultaneous registration declarations to the SEC: BlackRock Securet Treasury Based Limited Fund (BSTBL) and BlackRock Daily Revesment Stablecoin Reserve Vehicle (BRSRV)。

THESE TWO PRODUCTS ARE DESIGNED IN STARK CONTRAST TO MSNXX. BSTBL IS A MONETIZED VERSION OF THE EXISTING SELECTED NATIONAL DEBT LIQUIDITY FUND IN BELED. IT SERVES TRADITIONAL INSTITUTIONAL CASH MANAGERS — CLIENTS HAVE BOUGHT THE FUND, BUT NOW HAS AN ADDITIONAL CHAIN DISTRIBUTION CHANNEL。

BRSRV is a newly created monetized money market fund, distributed by Securitize multi-chain, targeting only one customer group: a stable issuer。

The key difference between Bellad and Morgan Stanley is..CurrencyizationI don't know. Belet chooses to issue the same asset (short-term national debt + cash + overnight buy-back) through a chain share to the issuer of the stable currency, giving the reserve assets themselves the potential to be chain-portfolio, 24/7 flow capacity and integration with the DeFi agreement. This is a customized product form for encrypted original customers (e.g. Ethena, Jupiter)。

The BSTBL + BRSRV file is an extension of the existing product matrix in Beled, extending the monetization infrastructure from the BUILL “DeFi collateral” to the BRSRV “stable currency reserve asset”。

1.3 May 12: Morgan Chase Second Entry

Four days later, Chase Morgan submitted to the SEC a file for JP Morgan On Chain Liquidity-Token Money Market Fund (JLTXX)。

The Fund itself invests in United States Treasury bonds and overnight buy-back agreements that are mortgaged on national bonds or cash, and the bottom assets are fully consistent with BUIDL, BSTBL, BRSRV. Token Class Shares indicates 13 May。

LTXX is not the first chain of JP MorganI don't know. As early as December 15th, 2025, JP Morgan Assembly Management was launched at the Ether HouseMy Onchain Net Yield FundI don't know. MONY is a 506 (c) private fund for only eligible investors。

This means that Morgan Chase has nearly five months of business experience on the monetization MMF track. JLTXX is not a catch product, it's a JP Morgan chain MMF policyStep two• extension of products originally limited to 506 (c) eligible investors to registered funds for a wider group of customers, specifically targeting the specific use of stable currency reserves。

CHASE MORGAN, ON THE ONE HAND, AND BANK OF AMERICA, BANK OF RICH COUNTRIES, CITIGROUP, ON THE OTHER HAND, EXPLORED THE RELEASE OF THE UNITED CONSORTIUM STABILIZATION COIN IN 2025, WHILE, ON THE OTHER HAND, DEEP-SEATED THE MONETIZATION RESERVE ASSET TRACK THROUGH THE MONY →JLTXX PRODUCT MATRIX. WHATEVER OCC ULTIMATELY DECIDES, MORGAN CHASE HAS A PRODUCT IN PLACE — THIS “SIDE DOWN” IS A UNIQUE STRATEGIC SPACE FOR MORGAN CHASE AS A GSIB BANK AND REGULATOR。

1.4 MAY 14: CLARITY BILL SEALS THE ENTIRE TRACK

ON 14 MAY, THE SENATE BANKING COMMISSION VOTED IN BIPARTISAN VOTES ON THE CLARITY BILL。

IT'S WORTH CAREFUL TASTE: MORGAN STANLEY'S MSNXX, BELED'S BSTBL/BRSRV, MORGAN CHASE'S JLTXX - ALL THESE PRODUCTSBefore the CLARTY Section 404 compromise text is made publicStart preparing。

In fact, since January 2026, when Clarity was put on hold for the first time, two things have become clear to the management industry: first, the “hold-to-earn” stable-currency incentive path will sooner or later be closed down. Secondly, there must be a stable currency reserve asset that exists, that must be compliant and that must necessarily pay interest。

Put those two together:when the hold-to-earn path is narrowed, one of the most robust "indirect gains" routes is through the reserve asset layer• The issuer of a stable currency does not pay interest per se, but its reserve is legally paid to the issuer by the monetized money market fund, who decides how to transmit this share of the proceeds to the users within the framework of compliance。

The product of the capital master is the infrastructure for this “most robust line of compliance gains”。

WHY IS CLARITY MORE IMPORTANT THAN GENIUS

2.1 Limited scope of GENIUS Act

To understand the paradigm conversion effect of Section 404, it is necessary to understand precisely the object it expands - GENIUS Act 4(a)(11)。

GENIUS Act, which entered into force in July 2025, provides that the issuer or issuer of a stable currency abroad shall not pay any interest or gain to the holder of the stable currency。

In other words, GENIUS Act itselfNo distinction“Positive proceeds” and “active incentives”, all forms of interest or proceeds are prohibited as long as they are paid by the issuer to the holder。

Second, it's..Only the issuer itselfDoes not include third parties such as exchanges, wallets, trustees, related parties, etc。

this second restriction creates a regulatory loophole — what industry calls “pass-through evasion”. the whole stable currency industry of 2025-2026 is essentially looking for an innovative space for compliance in this loophole:

- Coinbase / Kraken Mode: Exchange awards. USDC is issued by Circle, but Coinbase awards USDC holders about 4% through Coinbase One subscription mode。

- Gemini credit card mode: Trigger incentives through outside commercial transactions. GUSD is issued by Gemini Trust Company, but Gemini credit card holders receive GUSD returns for commercial consumption。

- Techorage Digital Neo mode: Payment through separate related legal entities. USDtb was published by the Angelage Digital Bank, but paid an award by the Angelage Digital Neo Ltd. (independent legal entity)。

THESE THREE MODELS TOGETHER FORM THE "INDIRECT DEBT" ECOLOGY OF THE GENIUS ERA。

But the basis for compliance is GENIUS ActOnly issuersThis is a limited scope。

2.2 Substantive extension of the CIATY Section 404

Clarity Act Section 404 did two things GENIUS Act didn't do。

First thing: extend to DASPs and related parties

Section 404 is no longer limited to the issuer of a stable currency, but extends to the “covered digital asset service provider and its related parties”. This scope clearly covers centralized exchanges, brokers, dealers and trustees。

This extension immediately shut down all compliance pathways such as Coinbase, Kraken, Gemini, Anchorage Digital Neo, which are “interest payments through non-issuers”. Coinbase as the DASP can no longer pay the hold-on-only USDC award; the Techorage Digital Neo can no longer pay the USDtb award。

second thing: introduction of the passive vs activity dichotomy

Section 404 prohibits DASPs from providing incentives “functionally or economically equivalent to interest on bank deposits” (proceeds, but retain) “based on real activities or transactions”。

This means that any incentive linked to “consumer, transaction, pledge, transfer” will survive, and no incentive to increase linearly with idle balances。

These two things come togetherFull pattern conversionI DON'T KNOW. ALL "INDIRECT INTEREST PAYMENTS" TEMPLATES OF THE GENIUS ERA WERE EITHER CLOSED OR RE-ENGINEERED DURING THE CLARITY ERA。

The stable currency industry is shifting from an interest-bearing market to an interest-paying market。

2.3 Winner path in paradigm transformation

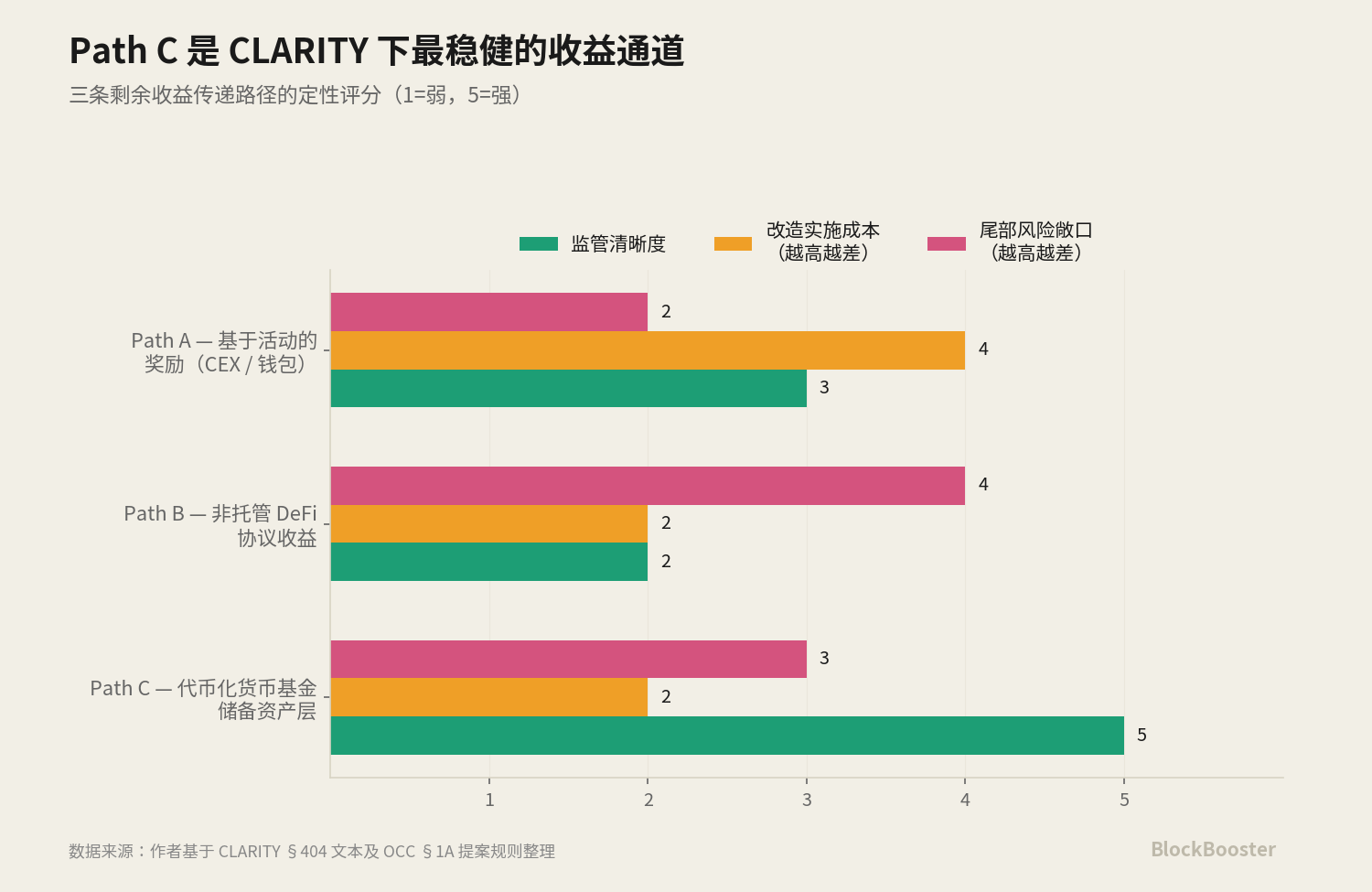

in the use-to-earn paradigm, there are three possible paths for passing the proceeds to the user。

PATH A: RE-ENGINEERED REWARD TO ACTIVITY-BASED REWARD

Applicable: Exchange, wallet, credit card. Coinbase may replace the USDC incentive with the “transactional frequency/consumption amount”. Gemini is already in a credit card return mode。

The key question is not whether Path A can keep the user alive, but its design costs - Coinbase needs to re-engineer the legal framework and product of the entire incentive system UI, and each active design is tested by the EC/CFTC. This reconfiguration takes 6-12 months, during which the loss of users is a real risk. But in the medium term, Patth A is quite likely to recover even beyond the attraction of the hold-to-earn era。

PATH B: LEAVE THE PROCEEDS ON THE PROTOCOL LEVEL AND PASS THEM TO THE USER THROUGH AN ACTIVITY-BASED OPERATION

Applicable object: DeFi protocol。Section 404 definition of “covered digital asset service provider” is clearly built around a centralized intermediary— The proceeds of non-hosting smart contracts, such as the supply of USDC to Aave for variable interest rate lending, are not designed to fall within this definition。

This means that the user has a variable interest rate for USDC to deposit in the Aave lending pool, which is now in conformity with most legal scholars' interpretation - the CARITY apparently unexpectedly left a revenue channel for non-trustee DeFi。

But there is significant uncertainty about this exemption. If the final rule extends the concept of “economic equivalence” to non-trusted defi, or defines the front end of defi as a related party, the immunity of Path B may be substantially narrowed。

PATH C: INTEREST PAID THROUGH RESERVE ASSET LAYERS

This is the way Wall Street's giant bet. Specific mechanisms: The issuer of the stable currency does not pay interest per se, nor does the DASPs, but the reserve asset of the stable currency is a monetized money market fund, which legally pays interest to its holder (i.e. the issuer of the stable currency). When the issuer of the stable currency receives the proceeds from the distribution of the fund, it is retained as the profits of the company - or partially passed to the user through the design of an active behavioural incentive。

Key compliance advantages of this path: ITS YIELD IS NOT STABLE CURRENCY, NOR IS IT ON DASP, BUT RATHERBase fund level— Not related to the regulatory framework for stable currencies。

The three paths are not mutually exclusive, but they evolve simultaneously。

Path A may gain new lives at the hands of players like Coinbase with retail branding and distribution channels

Path B may yield windfall benefits for agreements such as Aave, Pendle (but with narrow tail risks for the next 12 months)

Path C is the least directly threatened route by Section 404, but requires a 20 per cent cap for the Monetary Supervisory Authority not to pass as a precondition。

PATH C IS THE “MOST ROBUST BENEFIT” COMPLIANCE REVENUE LAYER, BUT NOT THE “ONLY BENEFIT”。

That's why Wall Street's money-control giants centrally filed a monetization fund in April-May. They are providing one of the compliance proceeds infrastructure for the soon-to-be-defined use-to-earn paradigm of the CIA Section 404. Patth C is the most attractive after the risk adjustment - this is the bellards' industry's judgement, given the respective implementation costs and regulatory uncertainties。

2.4 PATH B AND PATH C COLLABORATION

THERE SEEMS TO BE POTENTIAL FOR COLLABORATION BETWEEN PATH B AND PATH C. A COMPLETE CHAIN-BASED REVENUE SYSTEM CAN USE BOTH PATHS:

- USE OF BUIDL - SOURCE OF REVENUE TO SECURE COMPLIANCE

- User-level split with Aave loan or Pendle proceeds - ensure that the "proceeds" that users feel come from active operations

This two-tiered structure of "BUIDL on the ground floor, the DeFi protocol on the surface" can theoretically build a user-to-earn system that is both compliant and user-friendly. It is clear that Beled introduced BUIDL without a specific vision of Section 404, but this product happens to be the best bottom of the use-to-earn system under the new paradigm。

Belet's three-tier product matrix — infrastructure for the new paradigm

3.1 Three products, three clients Group

To read Belet ' s strategy, three of its token fund products need to be compared on the desktop simultaneously:

BUIDL: Launched in March 2024. Original in Ether. The legal structure is the BVI Fund, which is hosted by Securitize。

Target client: DeFi protocol, encrypted parent institution, chain view that needs to be used as collateral. A loan agreement such as Aave has been accepted as a qualified collateral with a minimum investment of $5 million。

BSTBL: filed on 8 May 2026. The legal structure is the United States SEC-registered Government Monetary Market Fund, BNY Mellon Investment Services Services as a transfer agent。

Target client: Traditional institutional cash managers - clients already using the Beled Fund now have access to 24/7 trading capacity through chain shares

BRSRV: filed on 8 May 2026. The legal structure is the newly created money market fund, Securitize multi-chain distribution。

Target clientStable currency issuer - customised for compliance reserve requirements under GENIUS Act。

These three products exist in the market at the same time, but there is no overlap in the customer base at all. This layered product matrix design: the same subject-matter asset (short-term treasury + cash + buy-back overnight) is sold to three completely different customer groups through different legal packagings, different hosting structures and different distribution channels。

More importantly, the three products together constitute oneFull currency reserve asset ecosystem, covering all needs under the use-to-earn paradigm: BUIDL as collateral and portfolio asset on the DeFi protocol level; BSTBL as a chain cash management tool for traditional institutions; BRSRV as the core label for the Stable Currency issuer ' s reserve asset layer. Whatever the specific design of the use-to-earn system, Belet has already prepared the corresponding products for the required monetized reserve assets。

90% CONCENTRATION - NEGLECTED SYSTEMIC RISKS IN THE CLARITY PARADIGM SHIFT

AND THEN WE'RE GOING TO QUANTIFY THE CURRENT CONCENTRATION RISK OF BELET BUIDL。

When USDtb went online on December 16, 2024, the official cooperation announcement of Bethena and Belet clearly stated: “BUIDL accounts for more than 90% of USDtb reserves. This is the maximum configuration of any stable currency for the BuIDL."

Upon coming online on January 6, 2026, Jupusd had a reserve structure of 90% USDtb + 10% USDC liquidity buffer。

The resulting concentration:BUIDL Single Fund supports about 90% of USDtb 's reservesI don't knowIndirectly supports approximately 81% of the Jupusd reserve(90% of USDtb x 90% of Jupusd)。

USDtb has a historical peak of approximately $1.2 billion (data from June 2025), and Jupusd has grown rapidly since its launch in January 2026. This means that the health of the BUIDL Single Fund directly determines the solvency of at least two important stable currencies. If BUIDL undergoes large-scale foreclosure pressure, the downstream USDtb and Jupusd reserve assets will simultaneously expire。

THE CLARITY PARADIGM SHIFT FURTHER MAGNIFIES THIS CONCENTRATION RISKI don't know。

OCC 20% GAME OF RESERVE CAPITAL CAP - A, B, C WHICH WINNER

5.1 Proposal for a ceiling and objection

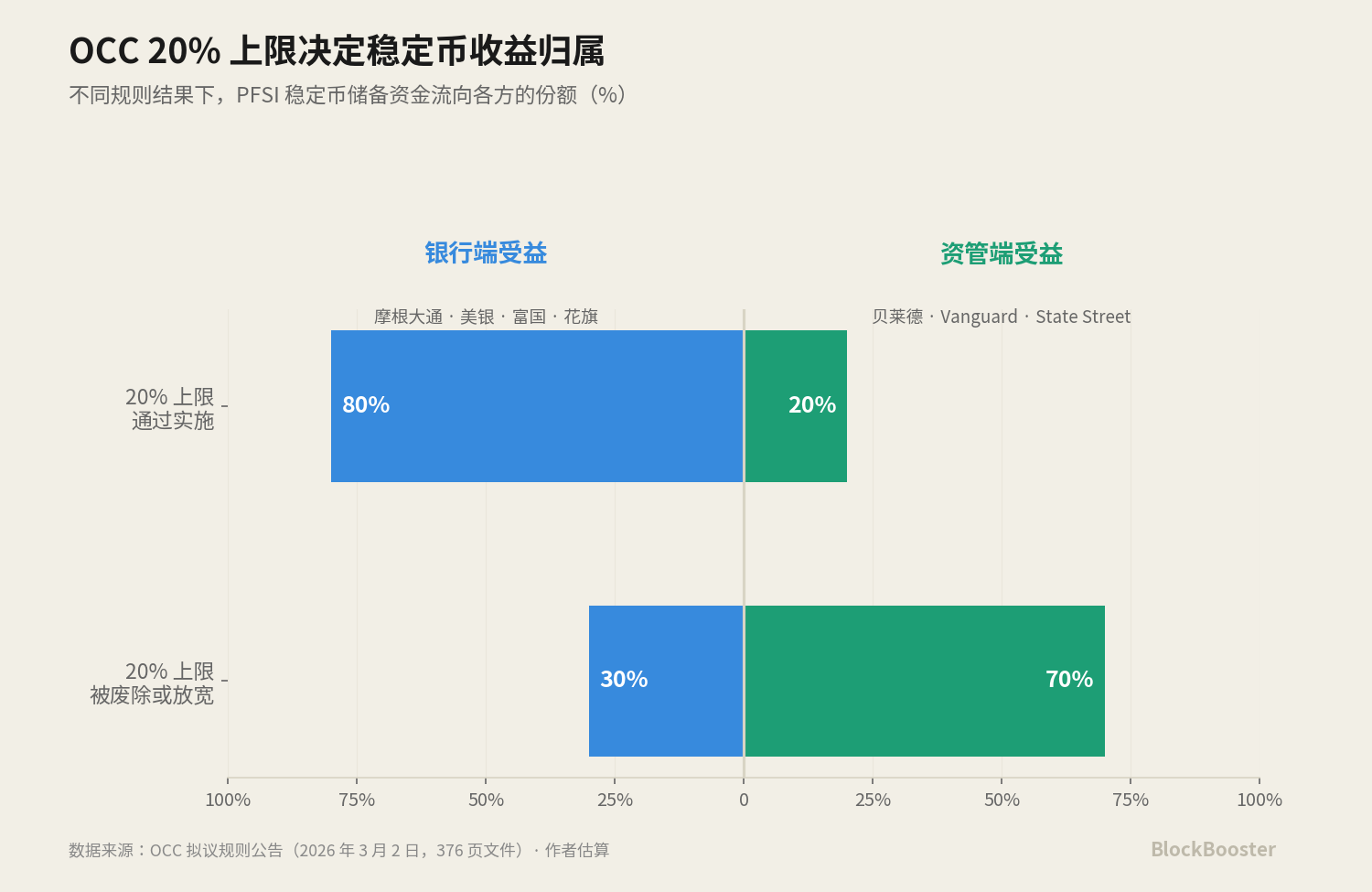

ON 2 MARCH, THE UNITED STATES MONETARY SUPERVISORY AUTHORITY (OCC) PUBLISHED A 376-PAGE PROPOSAL IN THE FEDERAL GAZETTE AS PART OF THE IMPLEMENTING REGULATIONS FOR THE GENIUS ACT. ONE OF THEM TRIGGERED A WHOLE INDUSTRY DISCUSSION:As a possible alternative thresholdThe Superintendence of Money explores whether there is a 20 per cent cap on the share of “currencyized assets” in the reserves of the Federal Chartered Stabilizers (PFSIs)。

Although it's just that the Money Supervisory Authority, in its consultation process, has proposed 20 per cent as a possible solution. But market participants have seen this alternative threshold as a strong signal of regulatory intent。

IF THE CEILING IS IMPLEMENTED, IT MEANS THAT UP TO 20 PER CENT OF THE RESERVE ASSETS CAN BE PLACED IN A MONETIZED FUND (E.G., BUIDL, JLTXX, BRSRV), WHILE THE REMAINING 80 PER CENT MUST BE PLACED IN TRADITIONAL NON-DINETIZED ASSETS。

This 20% cap, if passed, will directly counter the ability to scale the monetized reserve asset layer。

5.2 This is a zero-sum game to determine the path

THE REAL MEANING OF THE 20% CEILING IS:THIS IS THE KEY VARIABLE IN THE CLARITY PARADIGM CONVERSION PATH A, B, C, WHICH DETERMINES WHETHER THE C PATH CAN BE SCALEDI don't know。

THE PROPONENTS OF THE CEILING WERE MORGAN CHASE, THE BANK OF AMERICA, THE BANK OF RICH COUNTRIES, CITIGROUP, WHICH ANNOUNCED IN 2025 THAT IT WOULD EXPLORE THE POSSIBILITY OF A JOINT RELEASE OF A STABILIZATION CURRENCY. IF THE 20 PER CENT CAP IS PASSED, 80 PER CENT OF THE PPSI RESERVE ASSETS MUST BE PLACED IN TRADITIONAL ASSETS, WHICH MEANS THAT MOST OF THE RESERVE FUNDS WILL GO BACK TO THE BANK DEPOSIT SYSTEM, THE FOUR BANKS BENEFITING THE MOST。

The party opposing the ceiling is the giants Belet, Vanguard, State Street. If the ceiling is lifted or significantly eased, 100 per cent of the PPPI reserve assets can be placed in a monetized money market fund (including BUIDL, BSTBL, BRSRV), the largest beneficiaries being these companies. Path C is completely open。

5.3 CHANGE IN GAME AFTER CLARITY

ON MAY 14, THROUGH THE SENATE BANKING COMMISSION, THE CLARTY BILL ADDED A KEY VARIABLE TO THE 20 PER CENT CEILING GAME OF THE OCC。

THE CLARITY ACT PROVIDES A CLEAR LEGAL STATUS FOR TOKENIZED SECURITIES - THIS INDIRECTLY WEAKENS OCC'S ARGUMENT THAT “DINETIZED ASSETS ARE PARTICULARLY RISKY AND REQUIRE ADDITIONAL RESTRICTIONS”. IF CLARITY CONFERS LEGAL STATUS ON THE FUND, OCC CAN NO LONGER JUSTIFY ITS RESTRICTION BY USING THE TERM “SPECIAL RISK PER SE”。

When the CLARITY+GENIUS completes the framework, OCC is expected to have to adjust its 20% alternative threshold. The most likely outcome is that the threshold has been abolished or significantly relaxed. This is part of the victory of BlackRock's preferred "principle-based" route。

But here's the question:Path C's size victory and the concentration systemic risk discussed in Part Four are two sides of the same coinI DON'T KNOW. IF THE 20 PER CENT THRESHOLD OF THE OCC IS EASED, THE BUDIL-TYPE FOUNDATION QUICKLY ABSORBS TENS OR HUNDREDS OF BILLIONS OF DOLLARS IN STABLE CURRENCY RESERVES, AND THE INDUSTRIAL VALUE OF THE BETS MADE BY THE BELEDERS IS REALIZED. AT THE SAME TIME, HOWEVER, THE RISKS OF BUIDL SINGLE-POINT FAILURE, THE RISK OF BACK-TO-BACK TRAMPLING, AND THE RISK OF A “PYRAMID CONCENTRATION” OF THE ENCRYPTED DOLLAR ECONOMY ARE MAGNIFIED SIMULTANEOUSLY。

In other wordsThe victory of Path C is industrially a victory for Belet, but systemicly a birth of new concentration risksI don't know。

Traditional finance uses SIFMU identification, CCAR pressure testing, DTCC disaster preparedness mechanisms to manage this scale concentration. As the chain-based monetized reserve asset layer currently has no equivalent mechanism at all, the victory of Path C could be accompanied by a window of time — a window of time for regulatory frameworks to catch up on concentration risk. Whether or not FSOC started to intervene in this concentration issue in 2027-2028 is a policy variable worth tracking。

Conclusions

The entire stable-currency-receiving economy was forced to replace “observe” with “utilise” and the monetized-market fund, as a bottom reserve asset, became one of the most robust revenue-receiving infrastructure in the new paradigmI don't know。

The layout of Wall Street's management giant products — MSNXX of MSM, BSTBL/BRSRV of BlackRock, JLTXX of JP Morgan — is the industry card for this paradigm shift。

The real protagonist in this direction is a monetized money market fund provider at the bottom of the industrial chain. Visa and Mastercard do not deal directly with consumers, but they have established a high-māori, high-growth, strong-collar business model by charging about 0.1 to 0.3 per cent of each transaction - a combined market value of more than $1 trillion, well above the vast majority of credit card issuances。

The same role is being played in the encrypted US dollar economy by the money reserve asset providers (Beled, Morgan Chase, Morgan Stanley)。

We're witnessing it, onceRegulatoryly driven shifts in financial infrastructureI don't know. Clarity Act closed the GENIUS-era “indirect interest payments” path, but it did not close the proceeds themselves — the proceeds were forcibly repositioned to the reserve asset layer. Visa and Mastercard of the New World are in position。