Oil prices are approaching the threshold, what will happen in mid-April

Time is the determining factor, with oil markets moving three paths

Original title: (WCTW) The Oil Market Breaking Point

Original by HFI Research

Photo by Peggy Block Beats

Editor: It is argued that the real driving force of oil prices is not just the end of the conflict, but "when across the threshold"。

The oil market is experiencing a typical "time-pricing" during the Iranian conflict, which lasted nearly four weeks. The release of strategic reserves has slowed the shock but has not been able to close the supply gap; the disruption of tanker transport and the lag in the recovery of capacity have kept stock pressure on the future. Once this key node has been crossed in mid-April, the price mechanism will shift from "buffered volatility" to "deficit-led heavy pricing"。

More notably, the game structure itself is changing. The conflict no longer presents a path of "upgrading to downgrading" but instead turns to the endurance test of market critical points. Those who manage supply-demand imbalances are market-pricing, the bargaining power is vested in them. This means that even if the conflict ends in the short term, it will be difficult for oil prices to return to their original zones. Current supply losses are reshaping the global oil balance for some time to come。

The following is the original text:

In this article, I will decipher for you the circumstances that may arise. How will the situation affect the oil market as the conflict in Iran continues for nearly four weeks

On 9 March, we published an open article entitled " My latest judgement on the oil and gas market in the context of the Iranian conflict " , which reads:

The following is the effect on oil prices in unsympathetic circumstances (the “bunk loss” already covers the time required to restore capacity):

Situation I: Tanker transport resumes the day after

• The average annual price of Brent crude oil will rise to a low range of $70 to $80 (about 210 million barrels lost)

Situation II: Tanker transport resumed by March 15th

Brent's average annual price will be high at $80

Situation III: Tanker transport resumed by 22 March

Brent's average annual price will be below $90

Situation IV: Tanker transport resumed before March 29th

Brent's average annual price will be high at $90

If the tanker transport could not return to normal by March 29th, the situation facing the oil market would not even be envisaged. The only way out would be for demand to contract and prices to be pushed to extreme levels。

SHORTLY AFTER THE RELEASE OF THE REPORT, THE INTERNATIONAL ENERGY AGENCY (IEA) ANNOUNCED THE COORDINATED RELEASE OF A TOTAL OF 400 MILLION BARRELS OF GLOBAL STRATEGIC OIL RESERVES (SPR). THIS WILL MITIGATE, TO SOME EXTENT, THE IMPACT OF SUPPLY LOSSES. BUT AS WE STATED IN OUR FOLLOW-UP ARTICLE, "IEA CO-RELEASES THE SPR, DELIVERING THE BIGGEST GIFT TO MULTIPLE HEADS:

FROM A TRADE POINT OF VIEW, TRADERS WILL NOT RUSH TO PUSH UP OIL PRICES UNTIL THIS LAYER OF “BUFFER PAD” IS EXHAUSTED. THE CENTRALIZED RELEASE OF THE SPR DOES ALLEVIATE SHORT-TERM SUPPLY ANXIETY, BUT IT IS ONLY A TEMPORARY SOLUTION. MARKETS WILL REMAIN TENSE AND OIL PRICES WILL GRADUALLY RISE AS LONG AS TANKER TRANSPORT DOES NOT RESUME。

On the other hand, if the situation is eased rapidly — for example, by an immediate ceasefire or agreement — oil prices will fall rapidly. For example, if a peace agreement is reached by March 15, there will be a net increase in global stocks of 110 million barrels (400 million barrels released - 290 million barrels lost)。

This could repressurize Brent prices to a median of $70。

On the contrary, in the absence of a peace agreement and in the absence of supply disruptions until the end of March, there will be a net reduction of 50 million barrels in global stocks, and the gap will increase by about 8 million barrels every week。

THEREFORE, THE SPR'S ROLE IS MERELY TO BUY TIME AND DOES NOT SOLVE THE CORE PROBLEM. TANKER TRANSPORTATION MUST RETURN TO NORMAL. HOWEVER, IT DID AVOID CATASTROPHIC PRICE HIKES IN THE SHORT TERM, THUS PREVENTING A MASSIVE COLLAPSE OF DEMAND。

The time has moved on, and we have entered the "March 29" scenario that was set at the beginning of the month. Next, we'll judge the direction of the oil market based on the latest facts。

Facts

The total cut-off from Saudi Arabia, the United Arab Emirates, Kuwait, Iraq and Bahrain reached 1.09 million barrels per day:

Iraq: 36 million barrels/day

Kuwait: 235 million barrels/day

United Arab Emirates: 1.8 million barrels per day

Saudi: 30.5 million barrels per day

Bahrain: 18 000 barrels per day

Saudi Arabia has exhausted its capacity to transport its goods to the pipeline and is currently exporting about 4 million barrels per day through the Red Sea. The United Arab Emirates also transports by-pass through the Habshan-Fujairah pipeline, whose capacity of approximately 1.8 million barrels per day has reached the ceiling. Tanker traffic in the Strait of Hormuz remains completely disrupted. Indeed, even if the war ended tomorrow, it would take months to restore production and rebuild normal transport。

A scenario

I'll give you three possible paths:

1) War ended this week and transport resumed this weekend

2) The war ended in mid-April

The war ended at the end of April

IT NEEDS TO BE NOTED THAT THE RELEASE OF 400 MILLION BARRELS OF SPR BOUGHT MORE TIME FOR THE MARKET THAN OUR INITIAL JUDGEMENT OF MARCH 9. THIS CHANGE HAS BEEN TAKEN INTO ACCOUNT IN THE OIL PRICE SITUATION DESCRIBED BELOW。

Situation I: End of week

IMPACT ON GLOBAL STOCKS: -50 MILLION BARRELS (INCLUDED IN SPR)

Impact on Brent: Short-term return to low of $80, with average annual prices high of $80

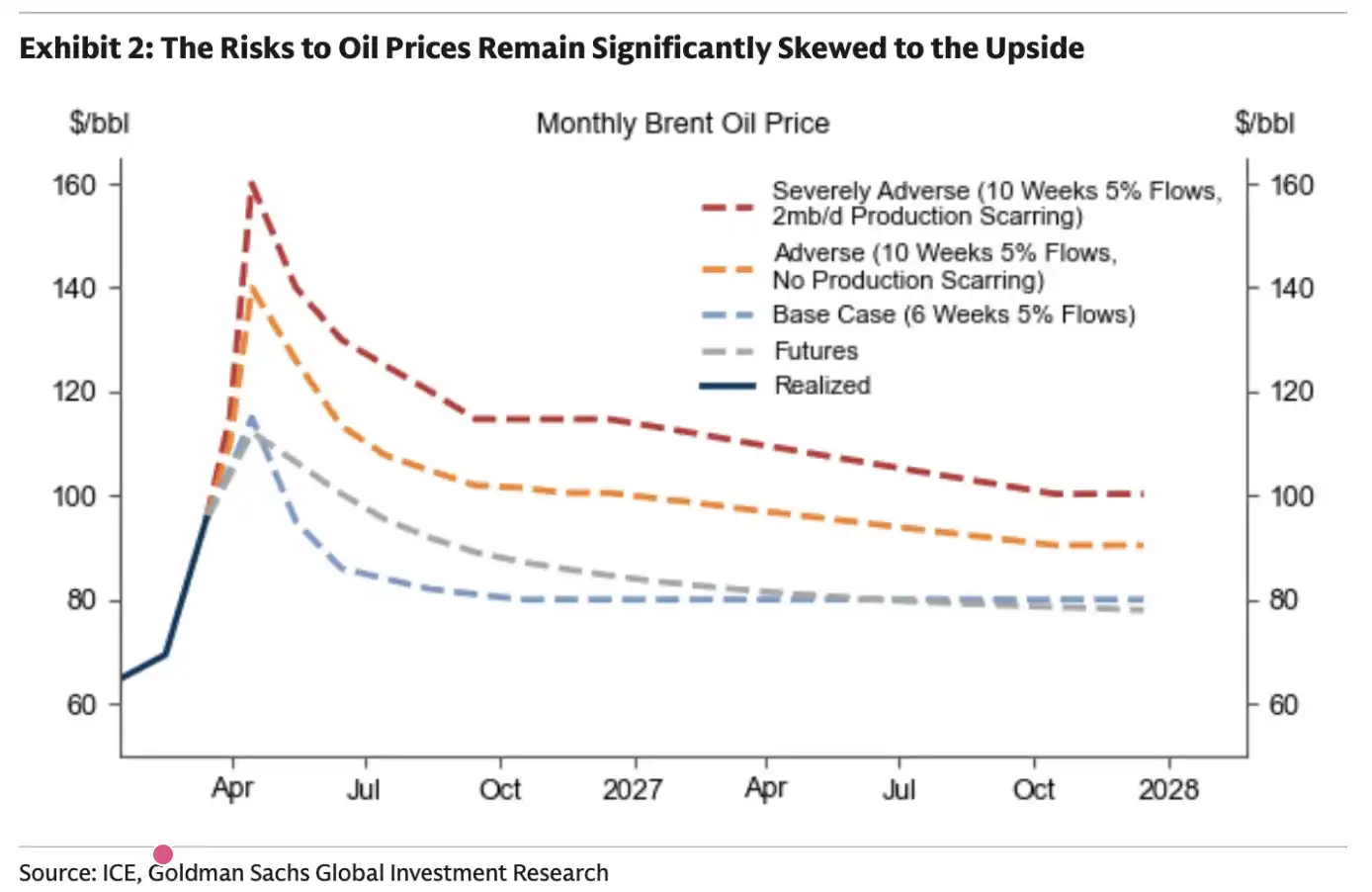

Situation II: End in mid-April

Impact on global stocks: -2.1 billion barrels

Impact on Brent: short-term return to low $90, with average annual prices high at $90

Situation 3: End of April

Impact on global stocks: -37 billion barrels

Impact on Brent: Short-term push up to $110 with an annual average of $110-120

Key turning point: mid-April

For the oil market, there is a clear “critical point”. The prevailing expectation in the market that the conflict will end by mid-April is crucial for price pricing。

Oil prices are the product of "marginal pricing". As long as the market believes that the supply is still "hard enough", there will be no panic. The current state of oil markets is exactly that — lack of panic。

THE POLICY OF THE TRUMP GOVERNMENT, THE EASING OF SANCTIONS ON IRANIAN AND RUSSIAN CRUDE OIL, AND THE RELEASE OF THE SPR HAVE TOGETHER SUPPRESSED OIL PRICES。

But once this threshold has been crossed, these factors will not work。

At present, the evaporation effect of global "in transit oil" has not been truly transmitted to land-based stocks. But our judgment is that by mid-April, this impact will be fully felt。

IF THE CONFLICT REMAINS UNRESOLVED BY MID-APRIL, THE INTERNATIONAL ENERGY AGENCY (IEA) WILL HAVE TO ONCE AGAIN COORDINATE THE RELEASE OF SOME 400 MILLION BARRELS OF STRATEGIC OIL RESERVES (SPR). IF NOT, OIL PRICES WILL RUN UP TO "DEMAND DAMAGE" (OVER $200)。

Long-term impact

In its latest weekly report, Energy Aspect measured cumulative market losses of approximately 930 million barrels. Of these, cumulative production losses between May and December were approximately 340 million barrels。

This judgement is clearly more radical than we are. In our stockpile sensitivity analysis, the reality that restoring production capacity in countries such as Iraq and Kuwait may take three to four months has not been fully taken into account. This means that our previous estimates may have been too conservative。

For Goldman Sachs, the conclusion is straightforward: the longer the conflict lasts, the longer the high oil prices last。

In these circumstances, Goldman Sachs also gave the assumption that if the conflict continued for another 10 weeks, what would the market look like? Its judgement is largely in line with the evolution we have seen before。

In essence, there is a critical point in the oil market. Once that line is crossed, there is no turning back。

Readers need to anticipate that there will be structural increases in oil prices in the future. Even if the war ended this week, the current supply losses that have already occurred will have a substantial impact on the future global oil supply and demand balance。

How long will it last

so far, i have avoided judging when the conflict will end. on the one hand, it's not a "flag," and on the other hand, it's impossible to predict。

it is clear, however, that this time is different from previous conflicts. in the past, the strategy of "escalate to de-escalate" was common, and there are few signs of this。

Retributive strikes took place without warning; the scope of Iran's attacks seemed to be no longer confined to Israel but extended to the Gulf States. It was that response that made me realize at the outset — this time, things are different。

As the conflict has lasted nearly four weeks, I am increasingly concerned that the probability of reaching an agreement is significantly reduced every additional day that it is delayed. As we have analysed in Time Under Exhaustion, Iran is well aware of the logic of operating the oil market. All it has to do is wait for the market to reach that “threshold point” so that it can make the biggest concessions to the US in the negotiations. From a tactical point of view, an agreement at this time would not be advantageous to it. This card has been played in the Strait of Hormuz and it will be difficult to repeat it in the future。

In the case of the Gulf States, if the current Iranian regime is not overthrown, this situation will be repeated in the future. This uncertainty remains unacceptable even if some kind of "passage fee" mechanism is established。

Thus, logically, the dominant power is not in the hands of the United States, but on the Iranian side. Under the circumstances, Iran is more motivated to push the situation to a “critical point” in the oil market to test America’s affordability. All it had to do was "hold on" for three weeks until the market began to crack。

It needs to be stressed, however, that I am not a geopolitical expert and that I am not fully confident of such judgements. What I can provide is a judgement based solely on the current situation under a basic analysis。

[ Chuckles ]Original Link]