The Hyperliquid Crossroad: Follow Robinwood or continue the NASDAQ economic paradigm

Ten times the difference between the trade volume and NASDAQ?

original by shaunda devens

This post is part of our special coverage Syria Protests 2011

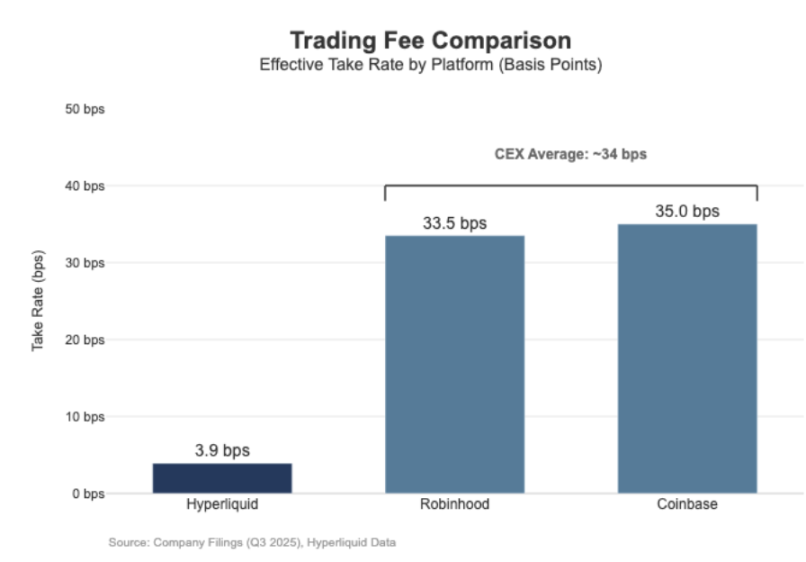

Hyperliquid's sustainable contract settlement has been at the Danasdac level, but the economic benefits have not been matched. Over the past 30 days, the platform has been liquidated with a nominal value of $20.56 billion (quarterly converted to an annualized scale of $61.7 billion), but only $8.03 million has been generated for handling fees at a rate of approximately 3.9 basis points。

It has a profit model similar to the "port of wholesale trading"。

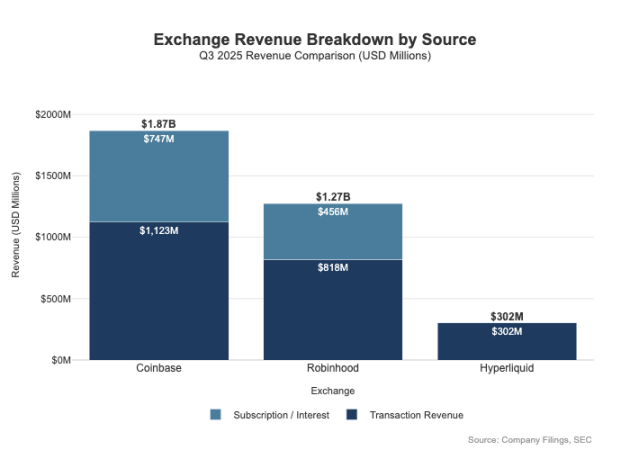

By contrast, Coinbase reported a total of $29.5 billion in transactions in the third quarter of 2025, with a turnover revenue of $1,046 million and an implied processing rate of 35.5 basis points. Robinhod shows a similar "retail-for-profit" pattern in encrypted money operations: 80 billion dollars in notional transactions in encrypted money generates $268 million in revenue from encrypted money transactions, with an implicit process rate of 33.5 basis points; at the same time, the platform’s stock transactions in the third quarter of 2025 amounted to $64.7 billion in nominal terms。

The difference between the two is not only reflected in the rate - retail platforms have more diversified profit channels. In the third quarter of 2025, Robinhood received $730 million in transaction-related income, in addition to $456 million in net interest income and $88 million in other income (mainly from Gold Subscription Services). In retrospect, Hyperliquid is still highly dependent on transactional fees and, at the protocol level, has been structurally maintained at the level of a single-digit base point。

This difference is essentially a result of "differing": Coinbase and Robinwood are "brokers/distributors" that make profits through balance sheets and subscriptions; and Hyperliquid is closer to the "exchange level". In traditional market structures, profit pools are distributed at these two levels。

Separation of brokering and exchange models

The central difference between traditional finance (TradFi) is the separation of the "distributional" and "market" ends. Retail platforms such as Robinhod and Coinbase are on the "distribution level" and occupy the high-māori domain; exchanges like NASDAQ are on the "market level" - and they are on the market level. At this level, pricing rights are structurally limited, and competition in the transaction enforcement chain is gradually moving towards a “big commercial economic model” (i.e., the profit space is being significantly reduced)。

1 Broker = Distribution + Customer balance sheet

Brokers control customer relations. Most users do not enter the market directly with the acceptance of Stark, but rather through brokers: brokers are responsible for opening accounts, hosting assets, deposit/risk control, customer support and processing of tax documents, and then direct orders to specific trading sites. This "customer relationship ownership" creates a profit-making space beyond the transaction:

- (a) Related fund balances: cash toll spreads, interest on finance coupons, proceeds from securities lending

- Service packaging: subscription services, bundled products, banking card services/advisory services

- Order route economy: Brokers control the flow of transactions and can embed payment share or benefit-sharing mechanisms in the route chain。

This is the central reason why brokers can make profits beyond where they trade: profit pools are concentrated at the "distributional" and "fund balances" ends。

Exchange = order matching + rule system + infrastructure, process rates subject to ceiling

Exchanges are responsible for operating trading premises, with core functions including order matching, setting market rules, safeguarding certainty enforcement and providing trade links. Its sources of profit include:

- (a) Transaction fees (in highly mobile products, fees continue to be kept low due to competition)

- Re-entry/mobility incentive schemes (most of the public fees are often returned to market vendors to attract liquidity)

- Market data services, trade connections/server hosting services

- Listing fees for services and indexing。

The order route model of Robinhod clearly reflects this structure: the broker (Robinhod Securities) controls the user, directs the order route to the centre of the third-party market, where the proceeds of the route are shared. Among them, the “distribution level” is a high-māori link - it controls access by users and develops multiple profit channels around transaction execution (e.g. order stream payments, financing operations, securities lending, subscription services)。

NASDAQ is a "low Māori layer": its core product is "Most commoditized transaction execution" and "order queue access", and pricing rights are subject to three-fold institutional constraints - the return of fees to marketers to attract liquidity, regulatory caps on access fees, and highly flexible order routes (users can easily switch to other platforms)。

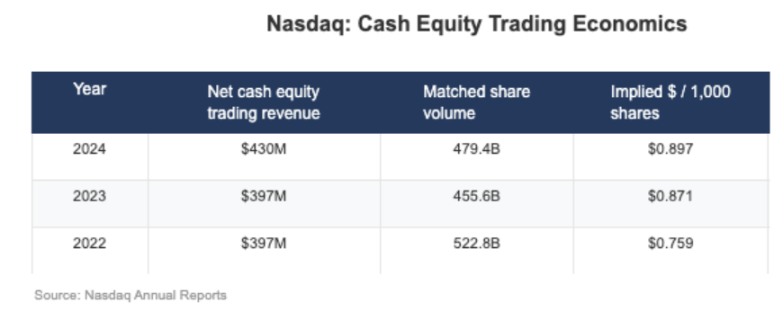

As can be seen from NASDAQ's disclosures, the “implied net cash gain” in its equity business is only US$ 0.001 per share (i.e., one in 1,000 dollars/equity)。

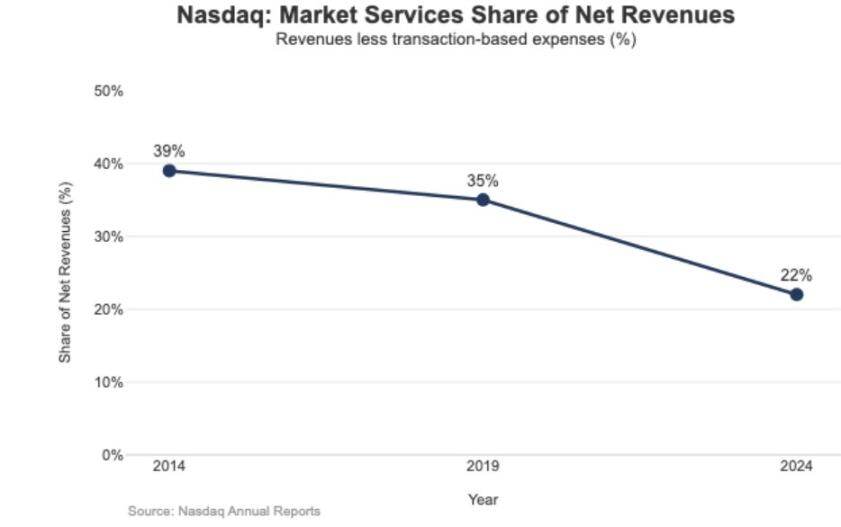

The strategic impact of low Maori is also reflected in the income structure of NASDAQ: In 2024, "market services" revenue amounted to $102 billion, representing only 22 per cent of total receipts of $4,649 million; this proportion was 39.4 per cent in 2014 and 35 per cent in 2019. This trend suggests that NASDAQ is moving from "business operations relying on market transactions" to "software/data operations that are more sustainable."。

Hyperliquid

The actual processing rate for the 4 base points of Hyperliquid is consistent with its strategy of "active choice of market-level positioning". The platform is building "Nasdak on the chain": using a "marketer / sole-employer" pricing model through high-volume order matching, bond calculation and clearing technology (HyperCore) -- its core optimization is "quality of transaction execution" and "liquidity sharing" rather than "retail user profit."。

This position is reflected in the separate design of two “traditional finance” types, which are not used in most encrypted money trading platforms:

1. Unlicensed Brokers / Distribution Level

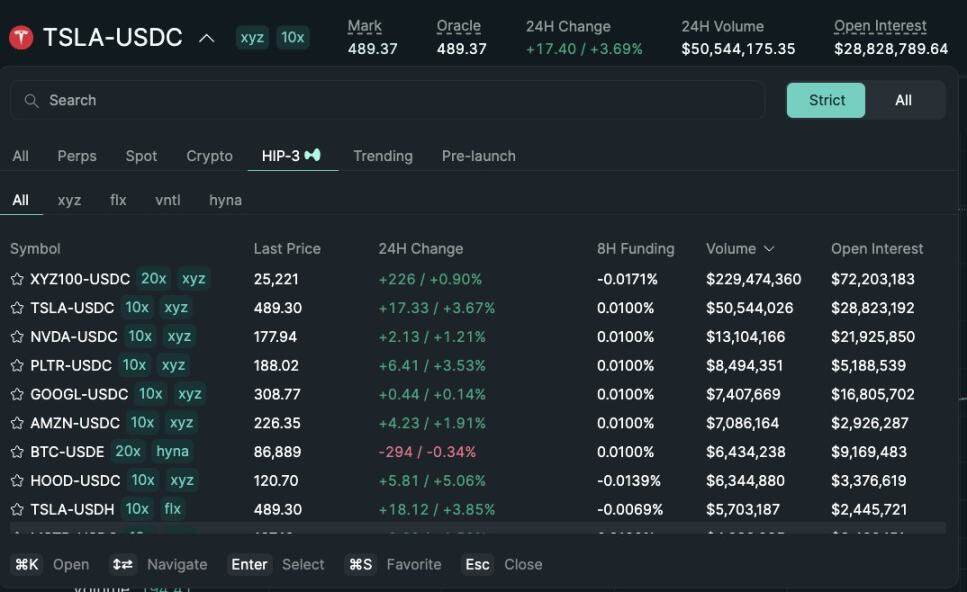

“Builder Codes” allows third-party interfaces to access core trading sites and to set their own rates. Of these, the maximum third-party handling fee for a lasting contract is 0.1 per cent (10 basis points) and the spot is 1 per cent, and the fee can be set separately by order - The design created a "distribution competition market" rather than a "single APP monopoly"。

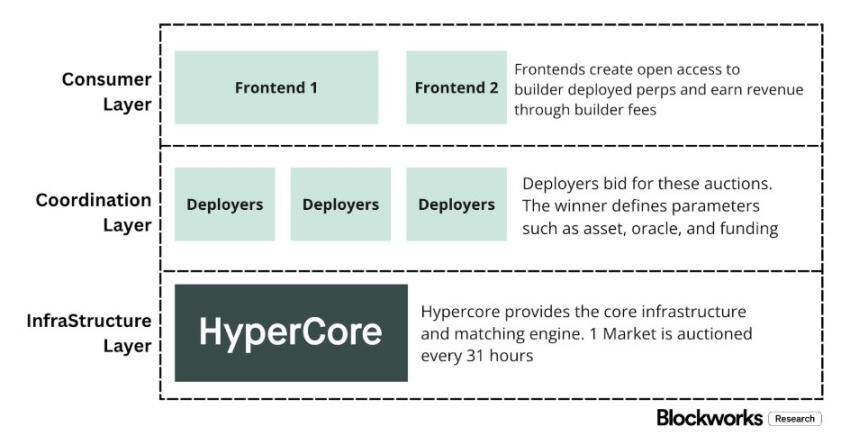

UNLICENSED LISTING / PRODUCT LAYER (HIP-3)

In traditional finance, the exchange controls listing powers and the creation of products; while HIP-3 "externalizes" this function: developers can base their contracts on the deployment of the HyperCore technology warehouse with the API, and define and operate the trading market autonomously. From an economic point of view, the HIP-3 formalizes the mechanism for sharing the proceeds between the trading site and the producer - the deployment party of the spot and the HIP-3 contract for renewal will receive 50 per cent of the transaction fee for the assets deployed。

"Builder Codes" has been effective at the distribution end: as of mid-December, about one third of users were trading through the front end of a third party rather than the official interface。

This structure, however, also puts a predictable strain on the revenue generated from the fees at the place of trading:

- Pricing compression: multiple front-end sharing of back-end liquidity, competition pushing down the "comprehensive cost" to a minimum; and handling fees that can be adjusted to order, further driving pricing closer to the bottom

- (a) Loss of profitability: the front-end controls the process of opening accounts, packaging services, subscriptions and transactions and occupies the high Maori space of the "brokers" while Hyperliquid retains only the low Maori income of the "places of dealing”

- Strategic route risk: If the front end develops into a "cross-platform order router", Hyperliquid will be forced into a "spread-through competition" - to keep the flow of transactions by cutting fees or increasing the number of returning domestic workers。

Hyperliquid, through HIP-3 and Builder Codes, took the initiative to position the "low Māori market" while allowing the "high Māori broker" to form on top of it. If the front end continues to expand, they will gradually take control of "user-end pricing", "user retention channels" and "routing voice" and will, in the long run, place structural pressure on the service rates of Hyperliquid。

Defense of distribution rights and expansion of non-exchange profit pools

The central risk facing Hyperliquid is the "Commodization Trap": If the front end of a third party continues to attract users at a price lower than the official interface, and eventually achieves a "cross-platform route", the platform will be forced to shift to a " wholesale implementation economic model" (i.e., the profit space continues to shrink)。

In the light of recent design adjustments, Hyperliquid is trying to circumvent this result while broadening its sources of income beyond transactional fees。

1. Distribution defence: maintaining economic competitiveness at the official interface

Earlier, Hyperliquid had proposed that "the pledge HYPE token would receive a maximum 40% fee discount" -- a design that would have made the front end of a third party structurally "lower than the official interface." With the elimination of the proposal, external distribution channels lost direct subsidies to "pricing below official interfaces". At the same time, the HIP-3 markets were initially distributed only through "developmenters" and were not displayed at the official front end; they are now included in the official front-end "strict list". This series of actions sends a clear signal that Hyperliquid still retains an unlicensed character at the "developmental level" but does not wish to compromise on the "core distribution rights"。

USDH: FROM "TRADING FOR PROFIT" TO "FUND FOR PROFIT"

The central purpose of the USDH roll-out is to recover the "stabilized currency reserve gains" that had been drained. According to the open mechanism, the reserve proceeds are allocated 50% to Hyperliquid and 50% to USDH ecological development. In addition, the design of the USDH trading market to benefit from fee discounts further reinforces this logic: Hyperliquid is willing to offer a "merger of profit from a single transaction" at the expense of a "larger and more stable pool of capital" - essentially by adding an "annual income stream" whose growth depends on the "monetary base" (rather than relying on trade volumes)。

3. Portfolio deposits: introduction of an "institutional brokering finance economy"

The Portfolio Guarantee mechanism harmonizes the cash with the guarantee of a lasting contract, allowing for risk-exposure hedges and introducing a "gen-born lending cycle". Hyperliquid will charge 10% of the borrower's interest. This design has gradually linked the economic model of the agreement to the “leverage rate” and “interest rate”, which are closer to the profit logic of “broker/institutional broker” rather than a purely exchange model。

Hyperliquid, the path to a broker economic model

While Hyperliquid’s trade volume has reached the “mainstream place” level, the profit model remains at the “market level”: nominal transactions are large, but the actual processing rate is a single-digit base point. The gap with Coinbase, Robinhood is structural: retail platforms are at the "brokers' level" to control user relations and fund balances and achieve high levels of Māori through multiple profit pools such as "financing, idle funds, subscriptions" ; pure trading places are based on "transaction execution as a core product", while "transaction execution" is bound to commercialize due to fluid competition and road elasticity, and profit space continues to shrink — NASDAQ is a typical example of this constraint in traditional finance。

Hyperliquid's initial depth coincides with the "Prototype Place of Exchange": by separating "Builder Codes" and "product creation" (HIP-3), eco-extension and market coverage are being promoted quickly. But the price of such a structure is "economic spillovers": if the front end of a third party controls "integrated pricing" and "cross-platform router rights", Hyperliquid risks "being part of a wholesale route to clear the flow of transactions at a low level for Māori."。

HOWEVER, RECENT ACTIONS SUGGEST THAT THE PLATFORM IS CONSCIOUSLY TURNING TO “DEFENDING DISTRIBUTION RIGHTS” AND “BROADENING REVENUE STRUCTURES” (NO LONGER DEPENDENT ON TRANSACTION FEES). FOR EXAMPLE, THE "OUTSIDE FRONT-END LOW-PRICE COMPETITION" IS NO LONGER SUBSIDIZED, THE HIP-3 MARKET IS INTEGRATED INTO THE OFFICIAL FRONT, AND THE BALANCE SHEET POOL IS ADDED. THE INTRODUCTION OF USDH IS A TYPICAL CASE OF INTEGRATING "RESERVES" INTO THE ECOLOGY (WITH 50% SPLIT AND FEE DISCOUNTS); THE COMBINATION BOND INTRODUCES THE "FINANCING ECONOMY" BY "COLLECTING 10% OF THE BORROWER'S INTEREST"。

At the moment, Hyperliquid is moving towards a “mixed model”: based on a “transaction execution route”, superseding “distribution defense” and “fund pool-driven profit pool”. This transition both reduces the risk of being caught in a "distributive low-māori trap" and aligns itself with the "brokers' income structure" without abandoning the "central advantage of uniform enforcement and liquidation"。

In 2026, Hyperliquid faced the central question of how to move towards a “brokering economy” without breaking the “outsourcing friendly model”. USDH is the most direct test case - its current supply is about $100 million, a scale that suggests that if the platform does not control the "distribution rights" it will expand very slowly. A more obvious alternative would have been the "official interface default settings", such as the automatic conversion of some $4 billion of USDC base funds into primary stable currencies (similar currencies that translate USDC automatically into BUD models)。

If Hyperliquid wants to acquire a “broker-level profit pool”, it must take “broker-like action” to strengthen control, deepen integration of self-employed products with official interfaces, and clarify boundaries with ecological teams (avoiding internal consumption on “distribution rights” and “fund balances”)。