I'm sorry. Five encryption agencies have the key to the direct Fed payment system.

Why is a federal trust bank license so valuable

Original Odaily Daily@OdailyChinaI'm not sure

Author Ethan@ethanzhang_web3I'm not sure

December 12, 2025, Office of the Control of the Currence, OCCPublication of bulletinsI don't knowConditional approval of five digital asset agencies, namely Ripple, Circle, Paxos, Bitgo and Federal Digital Assets, converted into federally licensed National Trust Bank。

This decision was not accompanied by sharp market fluctuations, but was generally seen as a watershed in the regulatory and financial circles. For the first time, encrypted businesses that have long been on the margins of traditional financial systems and are frequently disrupted by banking services have been formally incorporated into the regulatory framework of United States federal banks as “banks”。

Change is not sudden, but thorough enough. Ripple plans to create the "Ripple National Trust Bank", which will operate the "First National Digital Bank". The names themselves have sent a clear signal of regulatory release: digital asset-related operations are no longer merely “high-risk exceptions” to passive scrutiny, but are allowed to enter the core of the federal financial system under clear rules。

THIS SHIFT CONTRASTS SHARPLY WITH THE REGULATORY ENVIRONMENT THAT PREVAILED SEVERAL YEARS AGO. ESPECIALLY DURING THE BANKING TURMOIL OF 2023, THE ENCRYPTION INDUSTRY WAS ONCE CAUGHT IN THE SO-CALLED “DEBANKING” TRAP AND SYSTEMATICALLY CUT OFF FROM THE UNITED STATES DOLLAR SETTLEMENT SYSTEM. WITH THE SIGNING OF THE GENIUS ACT BY PRESIDENT TRUMP IN JULY 2025, FOR THE FIRST TIME, THE STABILIZATION CURRENCY AND RELATED INSTITUTIONS WERE PLACED IN A CLEAR FEDERAL LEGAL POSITION, WHICH ALSO PROVIDED THE INSTITUTIONAL PRECONDITIONS FOR OCC TO ISSUE THE CARDS。

This paper will be structured around the four dimensions of “What is the Federal Trust Bank” “Why is this license important” “the regulatory shift of the Trump era” and “the response and challenges of traditional finance” in order to streamline the institutional logic and practical implications behind this approval. The core judgement is that:The encryption industry is shifting from relying on “external users” of the banking system to becoming part of the financial infrastructure. This changes not only the cost structure of payments and liquidation but also the definition of “bank” in the digital economy。

What is the Federal Trust Bank

IF YOU WANT TO SEE THE REAL WEIGHT OF THIS OCC APPROVAL, YOU NEED TO FIRST CLARIFY AN ISSUE THAT IS EASILY MISUNDERSTOOD:This is not the case that five encryption companies have traditionally obtained “commercial bank licence plates”。

OCC APPROVES THE ELIGIBILITY OF THE NATIONAL TRUST BANK. THIS IS A TYPE OF BANKING CONCESSION THAT HAS LONG EXISTED IN THE UNITED STATES BANKING SYSTEM BUT HAS PREVIOUSLY SERVED MAINLY IN THE FORM OF ESTATE MANAGEMENT, INSTITUTIONAL TRUSTEESHIP, ETC. ITS CORE VALUE IS NOT HOW MUCH BUSINESS IT CAN DO, BUT WHAT IT DOESRegulatory hierarchy and infrastructure statusI don't know。

What does federal licensing mean

UNDER THE DUAL-TRACK BANKING SYSTEM OF THE UNITED STATES, FINANCIAL INSTITUTIONS MAY CHOOSE TO BE REGULATED BY STATE OR FEDERAL GOVERNMENTS. THE TWO ARE NOT A SIMPLE PARALLEL IN THE INTENSITY OF COMPLIANCE, BUT RATHER A CLEAR HIERARCHY OF AUTHORITY. FEDERALLY LICENSED BANK LICENCES ISSUED BY THE UNITED STATES MONETARY SUPERVISORY AUTHORITY (OCC) MEAN THAT INSTITUTIONS ARE DIRECTLY REGULATED BY THE TREASURY DEPARTMENT SYSTEM AND ENJOY “FEDERAL PRIORITY” AND ARE NO LONGER SUBJECT TO STATE-BY-STATE REGULATORY RULES AT THE COMPLIANCE AND OPERATIONAL LEVELS。

The legal basis behind this can be traced back to the National Bank Act of 1864. In the following century and a half, the system was an important institutional tool for the formation of a unified financial market in the United States. This is particularly critical for encryption companies。

Prior to this approval, whether Circle, Ripple or Paxos were required to apply for currency transfer licence plates (MTL) in 50 states for compliance across the United States, faced with a “plastic” system with different regulatory calibres, compliance requirements and enforcement scales. This is not only costly but also severely constrains the efficiency of business expansion。

WITH THE TRANSFER TO THE FEDERAL TRUST BANK, THE SUBJECT OF SUPERVISION WAS UPGRADED FROM THE CANTONAL FINANCIAL REGULATORS TO OCC. FOR AN ENTERPRISE, THAT MEANSHarmonization of compliance paths, national business passes and structural enhancement of regulatory credibilityI don't know。

Trust Bank, not "Shrink Commercial Bank"

It is particularly important to emphasize that the Federal Trust Bank is not equivalent to a “full-purpose commercial bank”. Five of the institutions that were approved this timeNOT BEING ALLOWED TO ABSORB PUBLIC DEPOSITS INSURED BY FDIC, NOR TO MAKE COMMERCIAL LOANSI don't know. This is also one of the central reasons why traditional banking organizations (e.g. Bank Policy Institute) have challenged the policy, which they consider to be “unequal rights and obligations”。

However, this limitation is highly compatible in terms of the business structure of the encryption enterprise itself. In the case of the issuer of the stable currency, whether it's USDC from Circle or RLUSD from Ripple, the business logic itself is based on100 per cent reserve asset supportUP. THE STABILIZATION CURRENCY DOES NOT EXTEND CREDIT OR DEPEND ON A PARTIAL RESERVE LENDING MODEL, SO THERE IS NO SYSTEMIC RISK ASSOCIATED WITH A “LENDING MATURITY MISMATCH” OF TRADITIONAL BANKS. IN THIS CONTEXT, THE INTRODUCTION OF FDIC DEPOSIT INSURANCE IS NEITHER NECESSARY NOR SIGNIFICANTLY INCREASES THE COMPLIANCE BURDEN。

And more importantly, the core of trust bank licences isTrusted responsibilityI DON'T KNOW. THIS MEANS THAT LICENSED INSTITUTIONS MUST LEGALLY STRICTLY SEGREGATE THE ASSETS OF THEIR CLIENTS FROM THEIR OWN FUNDS AND GIVE PRIORITY TO THE INTERESTS OF THEIR CLIENTS. THIS IS A MATTER OF GREAT RELEVANCE TO THE ENTIRE ENCRYPTION INDUSTRY AFTER THE MISAPPROPRIATION OF FTX ASSETS, AND ASSET SEGREGATION IS NO LONGER A CORPORATE COMMITMENT BUT A MANDATORY OBLIGATION UNDER FEDERAL LAW。

From “trustee” to “payment node”

Another implication of this change is that there has been a critical shift in the regulatory interpretation of the scope of the “trust banks”. OCC Head Jonathan GouldIt was made clearNew federal banking access “provides consumers with new products, services and sources of credit and ensures a dynamic, competitive and diversified banking system”. This provides a policy basis for the admission of encryption agencies。

In this framework, the strategic value of the “transformation” from the state-level trust to the Federal Trust Bank, completed by Paxos and BitGo, has changed far beyond name. The central point is that the OCC system gives the Federal Trust Bank a key right:Eligibility for access to the Federal Reserve payment systemI don't know. Therefore, their real objective is not to be called a bank, but to competeAccess to the central bank's core settlement systemI don't know。

In the case of Paxos, although it had previously become a compliance bar under the strict supervision of the New York State Financial Services Agency, there were natural limitations to state licences:It can't be directly integrated into the federal payment networkI DON'T KNOW. THE OCC APPROVAL DOCUMENTS MAKE IT CLEAR THAT THE CONVERSION OF THE NEW ENTITY CAN CONTINUE ITS OPERATIONS SUCH AS STABILIZATION CURRENCY, ASSET MONETIZATION AND DIGITAL ASSET HOSTING. THIS AMOUNTS TO FORMAL RECOGNITION AT THE INSTITUTIONAL LEVEL OF:Stable coins and asset monetization issued as legal “banking”I don't know. This is not a breakthrough for individual companies, but a substantial expansion of the scope of “bank” functions。

Once finally landed, these institutions are expected to be directly linked to central bank payment systems such as Fedwire or CHIPS, which no longer have to rely on traditional commercial banks as intermediaries. The most structural breakthrough in the transition from a “trustee asset manager” to a “direct node in the payment network” is that。

Why is this license plate so valuable

The real value of the Federal Trust Bank licence is not in the identity of the bank itself, but it may openA door to the direct route to the Fed's liquidation system。

And that's why Ripple CEO Brad Garlinghouse called this approval “a great advance”, while the traditional banking lobby (BPI) was very upset. For the former, this is an increase in efficiency and certainty; for the latter, it means that long-standing monopolies of financial infrastructure are being redistributed。

What does that mean

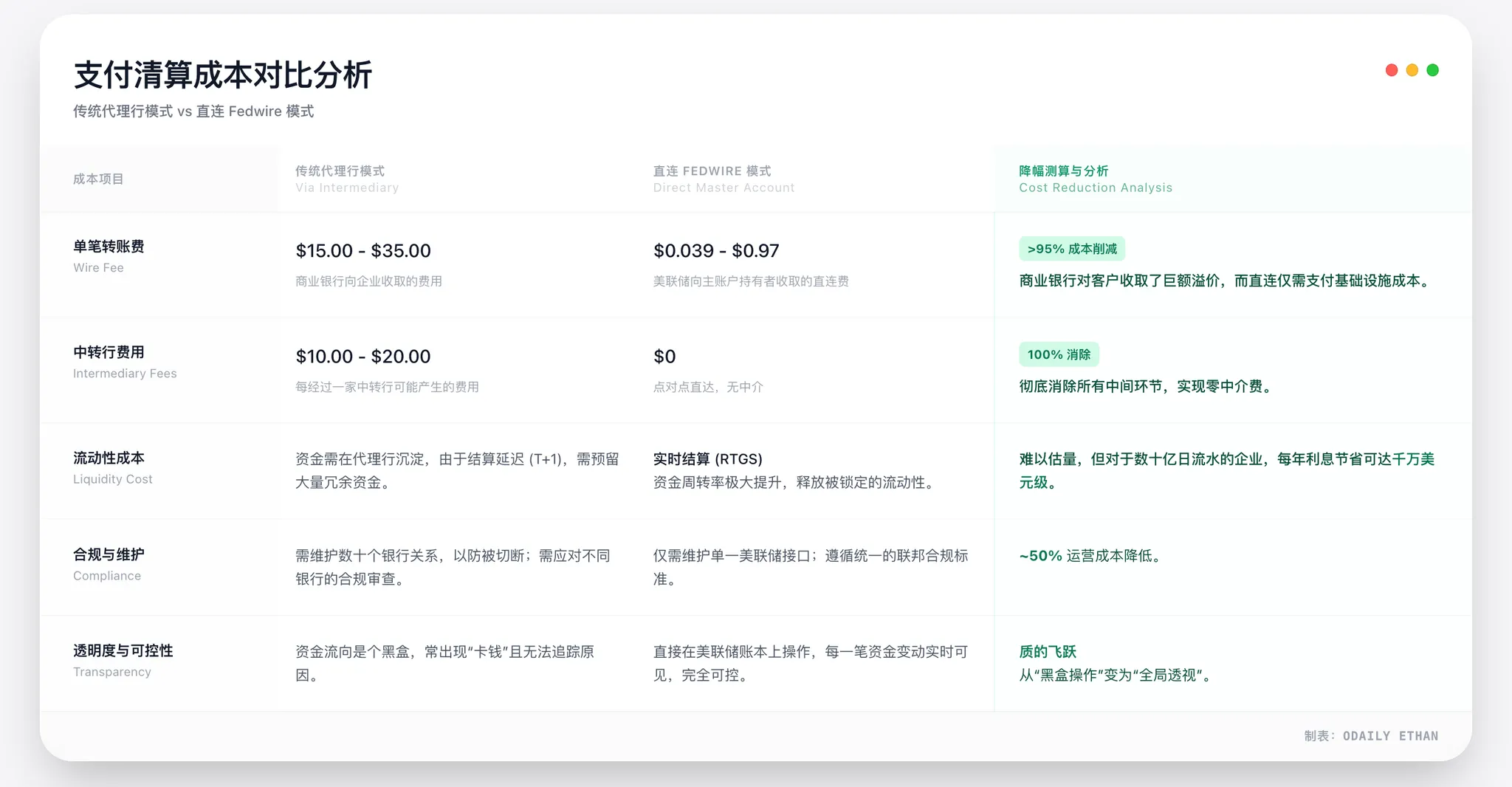

Previously, encryption companies had been at the “outside” of the United States dollar system. Whether Circle issues USDC or Ripple provides cross-border payment services, the final settlement involving the United States dollar must be done through commercial banks. This model is referred to in financial terms as the “agent bank system”. On the face of it, it is a longer process, which in essence poses three long-standing problems for the industry。

First of allUncertainty about the right to lifeI don't know. In the past few years, the encryption industry has repeatedly experienced unilateral terminations by banks. Once the correspondent bank exits, the penitentiaries of the encrypted enterprise will be cut off in a very short period of time, which will bring business to a standstill. This is what the industry calls the risk of “debanking”。

NextCost and efficiency issuesI don't know. The correspondent bank model means that every money flow is liquidated through multiple layers of banks, each with a delay in processing fees and time. This structure is naturally unfriendly for HF payments and stable currency settlement。

Number three:Clearing riskI don't know. The conventional banking system has generally adopted the T+1 or T+2 settlement rhythm, with funds not only taking up liquidity but also being exposed to bank credit risk during their journey. When Silicon Valley Bank closed down in 2023, Circle had an appointmentUS$ 3.3 BILLION US$A brief stay in the banking system is still considered a warning case for the industry。

This structure has changed the status of the Federal Trust Bank. At the institutional level, licensed institutions are eligible to apply for the Fed's “owner account”. Once approved, they have direct accessFedwireThe federal-level liquidation network completes a real-time, irrevocable final settlement in the United States dollar system and no longer relies on any commercial banking intermediary。

This means that, at this critical point in the liquidation of funds, institutions such as Circle and Ripple are for the first time at the same “system level” as Morgan Chase, Citibank。

Extreme cost advantage, not marginal optimization

The reduction in the payment of costs by acquiring the main account is structural and not marginal. Its core rationale is that the Fed’s payment system (e.g. Fedwire) completely bypasses the multilayered middlemen of traditional correspondent banks, thereby eliminating the corresponding intermediate costs and price increases。

We can build on industry practice andFederal Reserve Open Rate Mechanism 2026Go ahead. It was found that in high-frequency, large-volume scenarios such as stable currency issuance and agency payments, this direct-link model could reduce overall settlement costs by about30-50 per centI don't know. Cost reductions arise mainly at two levels:

- Direct rate advantage: The Fed paid large single charges to Fedwire well below the commercial bank ' s electricity reporting prices。

- Simplification of structures• Elimination of various handling fees, maintenance of accounts and liquidity management costs for the agency。

HereCircleFOR EXAMPLE, IT MANAGES NEARLY $80 BILLION IN USDC RESERVES, WHICH FACE HUGE FINANCIAL FLOWS ON A DAILY BASIS. IF THE DIRECT CONNECTION IS ACHIEVED AND ONLY ONE ITEM OF ACCESS COSTS IS PAID, THE ANNUAL SAVINGS COULD BE AS HIGH ASHundreds of millions of dollarsI don't know. This is by no means a micro-optimization, but a fundamental re-costing at the commercial model level。

Thus, the cost advantage of being eligible for the main account is defined and substantial, which will be translated directly into a core moat of stable currency issuers in terms of tariff competition and operational efficiency。

The legal and financial attributes of the stable currency are changing

WHEN THE ISSUER OF THE STABLE CURRENCY OPERATES AS THE FEDERAL TRUST BANK, THE ATTRIBUTES OF ITS PRODUCTS CHANGE. UNDER THE OLD MODEL, USDC OR RLUSD ARE CLOSER TO “DIGITAL VOUCHERS ISSUED BY TECHNOLOGY COMPANIES” WHOSE SECURITY IS HIGHLY DEPENDENT ON THE FIRM'S GOVERNING AND COOPERATING BANKS. AND IN THE NEW STRUCTURE, STABLE CURRENCY RESERVES WILL BE PLACEDOCC TRUST SYSTEM UNDER THE FEDERAL REGULATORY FRAMEWORKIt is also legally mandatory to separate from the issuer ' s own assets。

THIS IS NOT THE SAME AS THE CENTRAL BANK’S DIGITAL CURRENCY (CBDC), NOR DOES IT HAVE FDIC INSURANCE, BUT UNDER A COMBINATION OF “100% FULL RESERVE + FEDERAL LEVEL REGULATION + FIDUCIARY RESPONSIBILITY” ITS CREDIT RATING IS SIGNIFICANTLY HIGHER THAN MOST OFFSHORE STABLE CURRENCY PRODUCTS。

The more realistic impact is at the payment level. In the case of Ripple, its ODL products have long been limited to the opening of banking hours and the opening of the French-currency corridor. Once in the federal liquidation system, the switch between French currency and chain assets will no longer be subject to the time window, and continuity and certainty in cross-border settlements will increase significantly。

Market reaction is more rational

ALTHOUGH THIS PROGRESS WAS SEEN AS A MILESTONE WITHIN THE INDUSTRY, THE MARKET RESPONSE DID NOT FLUCTUATE SHARPLY. PRICE CHANGES ARE RELATIVELY LIMITED FOR BOTH XRP AND USDC-RELATED ASSETS. BUT THIS DOES NOT MEAN THAT THE LICENCE IS UNDERVALUED, MORE LIKELY:The market has seen it as a long-term institutional change rather than a short-term transactionI don't know。

Ripple CEO Brad Garlinghouse defines this progress as “the highest standard on the path to stable currency compliance”. Not only did he emphasize that RLUSD is now under the dual supervision of the Federation (OCC) and the State (NYDFS), but it goes more directly to the traditional banking lobby, “Your anti-competitive methods are already visible. You complain about the encryption industry's non-compliance, but now we're under OCC's direct regulatory standards. What are you afraid of?"

At the same time, it was noted in the relevant statement that the concession of the National Trust Bank would fundamentally restore institutional trust and enable distributors to provide digital asset hosting services to institutional clients with more fiduciary responsibilities。

The difference between the two is:From being “banked” to “becoming part of a bank”, encryption finance is entering a completely new phase. The Federal Trust Bank licence, on the other hand, is not only a paper licence, but also a secure gateway to the encrypted market for the capital of institutions that are waiting for uncertainty about compliance。

THE GOLDEN PERIOD OF THE TRUMP AGE AND THE GENIUS ACT

It is hard to imagine a encryption company getting federal approval as a “bank” by the end of 2025, three or four years back. This shift is not driven by technological breakthroughs, but by fundamental shifts in the political and regulatory environment。

THE RETURN OF THE TRUMP GOVERNMENT AND THE LANDING OF THE GENIUS ACT PAVED THE WAY FOR ENCRYPTED FINANCIAL ACCESS TO THE FEDERAL SYSTEM。

From "debanking" to institutionalization

DURING THE BIDEN ADMINISTRATION, THE ENCRYPTION INDUSTRY HAS LONG BEEN IN AN ENVIRONMENT OF STRONG REGULATION AND HIGH UNCERTAINTY. IN PARTICULAR, FOLLOWING THE FALL OF FTX IN 2022, THE MAIN TONE OF SUPERVISION SHIFTED TO “RISK SEGREGATION”, AND THE BANKING SYSTEM WAS ASKED TO STAY AWAY FROM ENCRYPTION。

This stage is referred to as “debanking” within the industry and is also described by some parliamentarians as “Operation Choke Point 2.0”. According to the House Committee on Financial ServicesFollow-up investigationsMany banks have cut off their cooperation with encryption enterprises under informal regulatory pressure. The successive exits of Silvergate Bank and Signature Bank are a central manifestation of this trend。

The regulatory logic was clear:Rather than trying to regulate encryption risks, they should be isolated from the banking system。

This logic was fundamentally reversed in 2025。

Trump has repeatedly publicly supported the encryption industry during the campaign, emphasizing the need for the United States to become a “global centre for encryption innovation”. Upon re-emergence, encrypted assets were no longer viewed as mere sources of risk but were incorporated into broader financial and strategic considerations。

The key shift is that the stability coin is beginning to be seen asExtension of the United States dollar systemI DON'T KNOW. ON THE DAY OF THE SIGNING OF THE GENIUS ACT, THE WHITE HOUSE NOTE MADE IT CLEAR THAT A REGULATED DOLLAR STABILIZATION CURRENCY WOULD HELP TO EXPAND THE DEMAND FOR UNITED STATES DEBT AND CONSOLIDATE THE DOLLAR ' S INTERNATIONAL STANDING IN THE DIGITAL AGE. THIS ESSENTIALLY REDEFINES THE ROLE OF STABILIZERS IN US FINANCE。

INSTITUTIONAL ROLE OF THE GENIUS ACT

IN JULY 2025, TRUMP SIGNED THE GENIUS ACT. THE PURPOSE OF THE ACT IS TO ESTABLISH FOR THE FIRST TIME, AT THE FEDERAL LEVEL, A CLEAR LEGAL IDENTITY FOR THE STABLE CURRENCY AND RELATED INSTITUTIONS. THE BILL EXPRESSLY ALLOWSNon-banking institutionsOnce the conditions have been met, they can be subject to federal supervision as “settled issuers of eligible pay-type stable currency”. This provides institutional access to the federal framework for companies that were originally outside the banking system, such as Circe and Pacos。

More importantly, the Act imposes mandatory requirements on reserve assets: a stable currency must be a highly liquid asset such as United States dollar cash or short-term United States Treasury bonds100% full supportI don't know. This, in essence, excludes the space for algorithm stabilization and high-risk configurations and is highly compatible with the “no-sustained-no-lending” trust banking model。

In addition, the Act establishes stable currency holdersPriority claimsI don't know. Even if the issuing agency went bankrupt, the relevant reserve assets would have to be used as a priority for the payment of the stabilization currency. This provision significantly reduces regulatory concerns about “moral hazard” and enhances the institutional credibility of the stability currency。

IN THIS FRAMEWORK, OCC ISSUED A FEDERAL TRUST BANK LICENSE TO AN ENCRYPTION FIRM, WHICH BECAME A LOGICAL ONEFollow the rulesand institutional implementation。

Defense of traditional finance and challenges for the future

For the encryption industry, it was a late system break-up; for Wall Street vested interests, it was more like a territorial invasion that had to be countered. The OCC, which approved the transformation of five encryption agencies into federal trust banks, did not speak out in a unanimous manner, but quickly triggered a violent defence by the traditional banking union, represented by the Bank Policy Institute, BPI. This war of “new and old banks” has just begun。

BPI'S STRONG BACK: THREE CORE ALLEGATIONS

BPI REPRESENTS THE INTERESTS OF THE GIANTS MORGAN CHASE, AMERICAN BANKS, CITIGROUP. AT THE VERY FIRST MOMENT WHEN OCC PUBLISHED ITS DECISION, ITS TOP LEVEL RAISED ACUTE QUESTIONS, WITH THE CORE ARGUMENT POINTING DIRECTLY TO THE DEEP CONFLICT IN THE PHILOSOPHY OF REGULATION。

First of all, about..It's a regulatory arbitrageI DON'T KNOW. ACCORDING TO BPI, THESE ENCRYPTION AGENCIES APPLY FOR “TRUST” PLATES, WHICH ARE ACTUALLY A CORE BANKING BUSINESS, SUCH AS PAYMENT AND LIQUIDATION, AND ARE EVEN MORE IMPORTANT THAN MANY MEDIUM-SIZED COMMERCIAL BANKS。

However, through trust licences, its parent company (e.g., Circle Internet Financial) has tactfully circumvented the Fed, which must accept as a “bank holding company”Combined ControlI don't know. This means that regulators do not have the right to review parent company software development or outward investment - if the parent company's code loophole leads to loss of bank assets, this creates an enormous risk exposure in the regulatory blind。

Second, yesThe breakdown of the sacred principle of “bank-business separation”I don't know. BPI warns that allowing such technology companies as Ripple and Circle to own banks essentially breaks the firewall against the use of bank funds by business giants. What's more, traditional banks are dissatisfiedUnfair competitionTECHNOLOGY COMPANIES CAN USE THEIR MONOPOLISTIC ADVANTAGE OVER SOCIAL NETWORKS AND DATA FLOWS TO CROWD OUT BANKS WITHOUT ASSUMING COMMUNITY REINVESTMENT (CRA) OBLIGATIONS THAT TRADITIONAL BANKS HAVE TO FULFIL。

And finally, about..Lack of systematic risk and safety netPANIC. SINCE THESE NEW TRUST BANKS DO NOT HAVE A FDIC INSURANCE COVER, TRADITIONAL DEPOSIT INSURANCE CANNOT ACT AS A BUFFER ONCE THE MARKET PANICS ABOUT THE ANCHORAGE OF A STABLE CURRENCY. BPI ARGUED THAT THE DEPLETION OF THIS UNPROTECTED MOBILITY WOULD SPREAD RAPIDLY INTO A SYSTEMIC CRISIS SIMILAR TO THAT OF 2008。

The Fed's Last Level

OCC ISSUED THE LICENSE PLATE, WHICH DOES NOT MEAN ANYTHING. FOR THESE FIVE NEW FEDERAL TRUST BANKS, THE LAST AND MOST CRITICAL ENTRY POINT TO THE FEDERAL PAYMENT SYSTEM -Right to open the main accountStill in the hands of the Fed。

Although OCC has recognized their banking identity, the Fed has independent discretion under the dual banking system of the United States. Previously, the encryption bank of Wyoming, Custodia Bank, had been..The Fed refused to open the main account and initiated a lengthy lawsuitThis precedent shows that there is still a huge gap between getting a license and getting real access to Fedwire。

THIS IS ALSO THE NEXT MAJOR BATTLEGROUND FOR TRADITIONAL BANKING (BPI) LOBBYING。SINCE IT IS IMPOSSIBLE TO PREVENT OCC FROM ISSUING CARDS, TRADITIONAL BANKING FORCES ARE BOUND TO PRESSURE THE FED TO SET A VERY HIGH THRESHOLD WHEN APPROVING THE MAIN ACCOUNT – FOR EXAMPLE, BY REQUIRING THEM TO PROVE THAT THEIR AML CAPABILITIES ARE AT THE SAME LEVEL AS THOSE OF ALMIGHTY BANKS LIKE MORGAN CHASE, OR BY REQUIRING THEIR PARENT COMPANIES TO PROVIDE ADDITIONAL CAPITAL GUARANTEES。

For Ripple and Circle, this game has just entered the second half: If they have a license and cannot open the Fed’s main account, they will still be able to operate through the correspondent bank model, and the gold brand of “national banks” will be significantly reduced。

Conclusion: The future, not just regulating the game

It can be expected that this future game around encrypted banks will clearly not remain at the licence level。

ON THE ONE HAND, THE ATTITUDE OF CANTONAL REGULATORS REMAINS UNCERTAIN. STRONG STATE REGULATORS, REPRESENTED BY THE NEW YORK STATE DEPARTMENT OF FINANCIAL SERVICES (NYDFS), HAVE LONG PLAYED A LEADING ROLE IN ENCRYPTION REGULATION. WITH THE EXPANSION OF FEDERAL PRIORITY, WHETHER OR NOT THE CANTONAL REGULATORY AUTHORITY HAS BEEN WEAKENED MAY GIVE RISE TO NEW LEGAL DISPUTES。

ON THE OTHER HAND, WHILE THE GENIUS ACT HAS ENTERED INTO FORCE, A LARGE NUMBER OF IMPLEMENTING REGULATIONS REMAIN TO BE DEVELOPED BY THE REGULATORY BODIES. SPECIFIC RULES, INCLUDING CAPITAL REQUIREMENTS, RISK SEGREGATION AND CYBERSECURITY STANDARDS, WILL BE THE FOCUS OF POLICY OVER TIME. THE GAME OF DIFFERENT STAKEHOLDERS IS LIKELY TO TAKE PLACE IN THESE TECHNICAL PROVISIONS。

In addition, changes at the market level are equally noteworthy. As encryption agencies acquire banking identity, they can become both a partner of traditional financial institutions and a potential subject of mergers and acquisitions. Whether traditional banks complete their technical skills through the acquisition of encryption agencies or whether encryption companies enter banking in reverse, the financial chart may be restructured as a result。

IT IS CERTAIN THAT THIS RATIFICATION BY OCC IS NOT THE END OF THE DISPUTE BUT A NEW STARTING POINT. ENCRYPTED FINANCE HAS ENTERED THE SYSTEM, BUT FINDING A BALANCE BETWEEN INNOVATION, STABILITY AND COMPETITION WILL REMAIN A QUESTION THAT UNITED STATES FINANCIAL REGULATION MUST ANSWER IN THE COMING YEARS。