The details of the Manus case, the era of offshore arbitrage is over

More than $2 billion in dream bubbles has become the most expensive compliance textbook in China's current history of technology and technology。

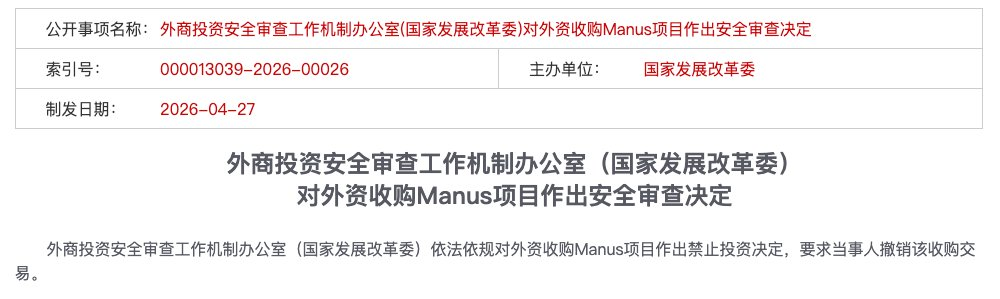

On 27 April 2026, the Office of the Foreign Investment Security Review Mechanism (the National Development and Reform Commission) issued a statutory anti-investment decision on the acquisition of Manus projects by foreign capital, requiring the parties to cancel the acquisition transaction。

Dozens of words have been pressed directly to the end of the $2 billion deal. Over the years, the products of Manus, the cutting of the legal framework, the rags and the effort to finance and exit have all collapsed and been wiped out。

THIS IS THE FIRST FOREIGN INVESTMENT ACQUISITION IN THE AI FIELD THAT HAS BEEN PUBLICLY SUSPENDED SINCE THE IMPLEMENTATION OF THE FOREIGN INVESTMENT SAFETY REVIEW SCHEME IN JANUARY 21。

There is one particular feature of the deal: the parties to the deal are legally offshored: Meta is a United States company, Manus has completed Singapore's relocation and set up a holding structure in Cayman. However, the decision to ban investment was finally taken by Chinese regulators。

THE SPILLOVER EFFECTS OF THIS CASE, AS WELL AS THE DARK SIDE OF THE MONTH, THE BYTE BEAT, THE STEP-GO STAR, ETC., ARE FACING CLEARER COMPLIANCE WINDOW GUIDANCE。

Behind this lies a deeper problem: the traditional offshoring system is becoming completely ineffective. From Day 0, entrepreneurs want to figure out their own line of compliance。

It doesn't tell stories, it's dry -- it regulates what laws and rules; it's where the red wires go out of the shower; and as of today, what are the companies' choices。

1. What laws and regulations are in accordance with the law

Looking back at the Manus case, most of the initial discussions in the industry focused on what happened - displacement, cutting, bans. But as the details of the case gradually surfaced, the legal community's focus went back to a more fundamental question: how can regulation stop the transaction? By what law? By what rules

The answer is not in a single law, but rather a three-tiered incremental regulatory logic. The formation of synergies between the three layers ultimately constitutes an irreconcilable review logic。

First level: determine the basis of the "main Chinese" - the penetrator review

This is the legal starting point for the whole case: which company is Manus

Legally speaking, the answer seems clear - Manus has completed the Singapore roll, with a holding structure in Cayman, butterfly Effect Pte, the parent company, is a Singapore entity in the tunnel. This is also the central legal statement of the Manus team throughout the transaction:

“Our main structure has been transformed into an external structure.”

But the regulatory answer is:

Form does not count, substance counts。

From a legal point of view, the law firm in Jin Tiancheng systematically analysed why “the extraterritorialation of the legal shell” was invalid in the Manus case. The root cause is that AI ' s core assets have a substantial and indissoluble relationship with jurisdictions in China at four dimensions:

- (a) Team dimension: a team of engineers who have mastered the core logic at the bottom, who have long accumulated research and development experience in China, and whose technical skills have been trained and developed in China

- Calculus dimensions: R & D in-country forms the path to technological interfaces and algorithms, and the architecture genes of the core system are labeled in China

- Algorithmic dimensions: The development and training of core model weights has been completed within the country, the most legally significant “technology source”

- DATA DIMENSIONS: TRAINING DATA ACCUMULATED BASED ON INTERACTIVE HUMAN FEEDBACK INTENSIVE LEARNING (RLHF) AMONG BIG USERS, WITH A HIGH CONCENTRATION OF SOURCES WITHIN THE COUNTRY。

These four dimensions point to the same conclusion: Manus' legal form is Singapore, but Manus, as the "technical substance" of a company, has its origins, cores, roots, all within China. According to the principle of "substantive over formality " , such substantive linkages, from a regulatory perspective, are sufficient to form the basis for penetrating scrutiny - the first cornerstone of all subsequent legal actions。

So although Xiao Hong created butterfly effect technology in Beijing in 2022, the "Cayman-Hong Kong-Beijing" Red Financing Structure in 2023, Singapore was relocated in 2025, and team cutting and business segregation was completed. The law, however, determines that it does not look “when” but “where”. Technical assets originating in China do not change nationality by registration on a piece of paper。

Second tier: export restrictions and regulatory circumvention - legal characterization of bathing

Once the first level is established: Manus is recognized as the essence of an "inner enterprise", the second level of legal logic follows. And then you move your core assets abroad, which is in itself an export. Exports are subject to export control legislation。

Manus' three-step move, in the eyes of a regulatory body, constitutes a complete puzzle of "backing export controls":

Step one, main shift. The main company was moved from China to Singapore to establish an offshore entity, Butterfly Electronic Pte, to build the Cayman Islands Holding Structure. The first step of “de-Chinaization” was legally completed。

Step two, team and asset migration. Lightning abolished nearly two thirds of the employees in the China District (80 of 120), retaining more than 40 core technicians to move to Singapore。

STEP THREE, DATA AND BUSINESS CUTTING. IN ADDITION, CHINA'S SOCIAL MEDIA ACCOUNTS ARE CLEARED, CHINA'S IP ACCESS IS BLOCKED, AND COOPERATION WITH ALI THONG YI IS TERMINATED。

Legally, the technical know-how, research and development capabilities, algorithmic experience of the core technical staff to carry out their departure is itself an act of "export of technology" that may be covered by the Directory of Technologies for Export Restrictions. At the same time, under the Data Security Act and the Data Exit Security Assessment Scheme, a large number of user interactive data trainings have been completed prior to the cutting, with a high concentration of origin in China - data genes have been modeled and cutting cannot be retroactively removed。

So the logic of regulatory penetration can be summed up in a cold phrase:

The code is written on Chinese soil, and the data is long among Chinese users -- this is the Chinese asset, the transfer is the export, the export is regulated。

The essence of bathing out is a form of compliance to cover up substantive violations, a systematic circumvention of export control regimes。

Level three: Active declaration mechanism

If the first two levels are “substantiation”, the third level is “procedural irregularities” - and one that is the easiest to be convicted。

Article IV of the Foreign Investment Safety Review Scheme clearly states that foreign investment involving important information technology, key technologies, etc., is “to be declared to the Office of the Working Mechanism on its own initiative prior to the implementation of the investment”. This is a mandatory ex ante declaration obligation, not a “recommendant report” or an “offer”。

Manus and Meta did not make any form of voluntary declaration to the Chinese regulatory bodies throughout the course of the transaction until the delivery was completed. During the months-long cut-off period, Manus and his funders seemed to have reached a dangerous consensus that they would not push windows as long as they did not knock on the door。

In legal practice, “unreported” is itself a serious violation of independence. It sends the signal that it is either knowingly or deliberately circumvented. Either way, regulation cannot be light。

A compliance lawyer concluded:

“The biggest compliance deficiency revealed in the Manus case is not the controversial applicability of a particular regulation, but the fact that the enterprise has simply abandoned its reporting obligations to China. In legal systems, evasion of the procedure itself is more intolerable than physical irregularities.”

When we look back, Manus' end is actually written on the first floor: Once a penetrating review has concluded that you are the “substantive subject of China”, the second-tier export control logic and third-tier reporting obligations automatically unlock the lock. The three layers of jurisprudence are progressive and conjunctivate, constituting a logical closed circle. In this ring, there's not a single link left for "fate"。

II. Why CDRC

Commerce first. On 8 January 2026, the spokesperson of the Ministry of Commerce publicly stated that the acquisition “will be evaluated for consistency with the relevant laws and regulations on export control, export and import of technology, and foreign investment”. But on April 27th, the hammer fell on the Commission。

There are articles in this department. According to some experts, the Ministry of Commerce is based on the Directory of Export Restrictive Technologies, which describes controlled technologies very specifically: Artificial intelligence interface technology for Chinese and minority languages. Manus, after taking a bath, all services have been converted into English and Chinese users have been denied access. This means that there may be some controversy if the line of export controls is simply pursued。

This is the room for controversy over the applicability of the statute. But we prefer a deeper meaning, which, after all, is less hierarchical than political considerations。

The Commission is responsible for “security clearance” and the Ministry of Commerce is responsible for “export and import of technology”. The appearance of the Commission meant that the matter had changed from “business” to “sovereignty”。

In other words, the CSD’s involvement as a macro sector with more integrated economic management than that of the Ministry of Commerce also sends a clear signal that this is not an occasional enforcement of the law against a company, but rather an institutional deterrent to “one punch, one punch, one punch, one punch, one punch, one punch.”。

One for an example。

All those who are still watching now see where the red line is -- not in the vagueness of a particular article, but in the irrefutable ultimate measure of national security。

III. Four high-risk trigger points

The following four red lines have been clarified in the Manus Consolidated case and the “penetrating” review principle established by the Foreign Investment Security Review Scheme. If you step on any one of them, you can't think about the "showing out" route。

Red Line I: Founder with Chinese passport, not cancelled

The founder of Manus, Shaw Hong, is a Chinese national. China ' s export control laws cover natural persons. This means that the founders themselves may be the subject of regulatory attention and that the arrangements cannot be understood only at the company level。

The harsher reality lies across the Pacific: the Chinese founders' financing environment is also tightening in the North American geopolitical risk assessment of VC. a16z The head of the Silicon Valley wind was thrown under geopolitical pressure and the willingness to invest in the founders of the Chinese passport fell sharply。

Manus’s B round of financing was led by Benchmark, but after that Benchmark was strongly rebuffed by US politics over this investment, several Republican senators called the deal “assisting the Chinese government”。

The investors of Silicon Valley Foundation stated:

The founders were Chinese, the company was in Beijing, and the core technology is universal AI Agent - this is the original sin。

Both sides are closed. You've got a Chinese passport, you've got American capital; you've got Chinese technology, and Chinese regulations don't let go. This stitch is much narrower than most people think。

Red Line Two: Money from the state

IT'S NOT ONLY THE NATIONAL SECURITY FUND THAT COUNTS AS A DIRECT INVESTMENT. THE LEADING FUNDS AT ALL LEVELS OF GOVERNMENT, THE STATE COMPONENT OF THE RMB FUND, AND THE POLICY BANK LOANS - ALL OF WHICH FALL WITHIN THE DEFINITION OF “NATIONAL BLOOD TRANSFUSIONS” - HAVE BEEN ESTABLISHED. THERE ARE ALSO OFFICES, MATHS, TALENT SUBSIDIES, ETC., WHOSE PROCEDURES ARE TOO CUMBERSOME TO PROCESS, AND WHICH ARE WRITTEN IN BOOKS AFTER AUTUMN。

Red Line Three: First line code written in China

The initial writing of the core code, the completion of algorithm model training, the storage location of the technical document - these seemingly “pure technology” facts are legally proof of the “technology source”. The early development of Manus was completed in China and when the team moved to Singapore, the code itself constituted an export of technology. Manus has never made any technical export declaration in respect of this transfer。

Red Line 4: Using Chinese data

THIS IS THE MOST LIKELY ILLUSION OF MANY AI ENTREPRENEURS: TO THINK THAT COMPANIES ARE CLEAN AS LONG AS THE DOMESTIC USERS ARE CLEARED AND CHINA'S IP IS BLOCKED。

But in regulatory terms, "technology" is not just about code, it's about data genes。

The Data Security Act and the Data Exit Security Assessment Scheme have a clear review requirement for cross-border transmission involving “critical data”. Although Manus has shut down Chinese services and blocked China’s IP, the early accumulation of user interaction data has completed the core training of the model - the data gene is engraved in the weight of the model, not the “late-cleaning” that can be recovered. Among Chinese users, the model was labelled with a Chinese label。

IV. ENTERPRISES IN SPECIFIC TERRITORIES: TEAMS, NOW

The ARR provides a security vetting mechanism for foreign investment that may affect national security, focusing on areas of defence and security, such as military industry, as well as important areas in which foreign investment can gain effective control, such as critical information technology, critical technologies, critical infrastructure and vital resources。

In the current regulatory environment following the Manus case, the following points deserve particular attention:

First, the judgement of “real control” does not depend solely on equity in practice; it falls into this category if foreign investors are able to have a significant impact on the enterprise's business decisions, personnel, finance, technology, etc. (e.g. having a veto or the right to know about key technologies). This is a very broad definition, for example: you took only 5 per cent of the equity of the dollar fund, but this 5 per cent share with a one-vote veto could be considered to have a significant impact on the enterprise's business decision-making, and thus "real control" and initiate review。

SECONDLY, THE COMMISSION, AS THE LEAD AGENCY FOR THE WORKING MECHANISM, HAS THE AUTHORITY TO PROVIDE COMPLIANCE WINDOW GUIDANCE BASED ON NATIONAL SECURITY JUDGEMENTS. FOR EXAMPLE, ON 24 APRIL 2026, THE CDRC REQUESTED PART OF AI ' S REFUSAL TO PROVIDE GUIDANCE ON EQUITY, WHICH WAS NOT INCLUDED IN THE TEXT, BUT WAS AN EXTENSION OF THE TERM "DAY-TO-DAY SECURITY REVIEW AND PREVENTIVE MANAGEMENT" AUTHORIZED BY ARTICLES 3 AND 7 OF THE ARR SCHEME。

THIRDLY, IT IS NOT RECOMMENDED TO CIRCUMVENT CENSORSHIP THROUGH VIE, PROXY, TRUST, ETC. IN PRACTICE, AN ENTERPRISE MAY BE AT RISK OF CORRECTION, SUSPENSION, WITHDRAWAL OR OTHER DISPOSAL FOR COMPLIANCE ONCE A CIRCUMVENTION ARRANGEMENT HAS BEEN FOUND TO EXIST。

In the past, the grey path of both sides of the wall has been blocked by 360 degrees. From now on, businesses must be clear on Day 0 on compliance。

ESPECIALLY ON THE AI TRACK, THERE ARE ONLY TWO ROUTES。

ROUTE A: TAKE THE US DOLLAR ROUTE - COMPLETELY CLEAN

If you decide to take the dollar fund, take the Silicon Valley route, and the ultimate goal is to be bought or put on the market, then what you're going to do is not take a bath, but change blood。

One hard standard: you can't step on one of the four red lines。

It means four things:

FIRST, THE FOUNDERS SETTLE NATIONALITY. THE CHINESE PASSPORT ITSELF IS THE UNITED STATES VC PERCEIVED COMPLIANCE RISK LABEL. IF YOU GO THIS WAY, IT IS NOT AN OPTION, BUT A PREREQUISITE。

SECOND, NO STATE MONEY. FUNDS INVOLVING GOVERNMENT-LED FUNDS, STATE-OWNED LPS AND POLICY LOANS SHOULD BE FULLY COMPLIANT AT AN EARLY STAGE OF FINANCING, AND SHOULD BE LIQUIDATED OR REPURCHASED AS NECESSARY。

Third, the source of the code is offshore. This is the most cruel and central one. The first line of the core algorithm must be completed outside the country. In-country teams can only do non-core modules or marginal operations. You need to build a truly research-and-development offshore technology center from the start -- not a shell, an entity。

Fourthly, data are isolated from users from day one. Do not touch Chinese user data from the start. It's not "late cleaning" but "never owned"。

This path is based on the premise that you can afford to be completely cut off from the domestic market. Revenues, users, brand synergies in the Chinese market were abandoned. You bet on the return of globalization to cover that price. And even if you did all of that, you'd have to face an increasingly unfriendly American-founder Chinese identity, which is still the "precious sin" in the eyes of some of the forces of Silicon Valley。

ROUTE B: FOLLOW THE INSIDE ROUTE - TIE UP THE NATIONAL TEAM

If you do not want or cannot take the American route, turn compliance into your moat。

Core logic: China's land, Chinese land, can only grow the Chinese renminbi。

First, to proactively embrace State/civil resources. In financing, priority is given to the RMB fund, the government-led fund, and the platform for investment. This is not a forced choice, but rather a strategic one: the national identity is the strongest regulatory pass。

Secondly, compliance is a pre-emptive advantage. While colleagues are trying to detour, you proactively declare safety clearances, proactively complete classification of data, and proactively file technology exports. In the eyes of regulation, you are “one of your own”; in the eyes of the market, your commitment to compliance is a barrier to short-term chase。

Thirdly, certification as a licensing barrier. This is not a cost, it is a license. In a tight regulatory environment, the difference between having a licence and not having a licence is between life and death。

Fourth, voluntary declaration of security clearance. Under Article IV of the Foreign Investment Safety Review Scheme, foreign investment involving important information technology and key technologies is subject to active declaration prior to implementation. This is not a burden for enterprises that follow the State's financial route, but rather the best gesture for you to take a position on regulation。

Following this path, you accept the RMB valuation logic and exit rhythm -- fast-forward, $2 billion lightning acquisition may not be your concern, but you switch to policy expectations of stability and continuity in the domestic market。

There's no other way to be big

"Cayman Holdings + Singapore Operating + R & D + US$ Financing in Singapore" has been sentenced to death. It is dangerous, not flexible, to continue to hesitate on this path. Supervision doesn't give you immunity because you haven't figured it out。

The pageant, go clean. If you choose the insider, you tie it down。

The Manus case is the only operational manual left to AI cross-border entrepreneurs。

It's written at the end: Butterfly effect. It's termed "single."

Manus named its parent company Butterfly Effects - the butterfly effect. Looking back at the name now, I can only lament the phrase。

This butterfly fanned its wings twice and rolled up two storms. One was an offer from Silicon Valley and one was a paper ban from Beijing. The pre- and post-regulatory control has now taken shape and the solicitation of purchases has become a failure of compliance, and this case will be included in a financing memorandum for each subsequent cross-border scientific enterprise。

Turning back to the perfect path of nine months' exit and two billion dollars' acquisition, three repeat mined areas were hidden from the beginning:

- TECHNICAL MINED AREAS: AI CORE CODE IS MONITORED AS SOON AS IT IS GENERATED IN CHINA

- Data mined areas: data from China are not traceable

- Identified mined areas: In this age, technology has nationality, who does it, and nationality。

In accordance with the law, the past was a principle, followed by iron law。

The focus today is not on who will be convicted, but rather on the trend of continuing to compress the grey space that used to be moved by registration, structure, and retrofitting. For the founders, going to the sea is no longer a game of "regulating regulation before compliance" but, from Day 0, thinking about the subject, the money, the technology, the data and the declaration path。

It is to be hoped that every founding team that finds a way out of the time, whether you choose the United States-funded runway to do your best or the system of internal expertise to do your best, will be able to see the rules, stand firm and walk further。

* This paper is a subjective analysis of the editorial team based on open information and industry observations and is intended to provide a multidimensional perspective for exploration. Nothing in the text constitutes a legal opinion or an investment proposal. If specific legal issues or business decisions are involved, it is important to consult licensed professional lawyers。