THE BATTLE OF THE SIX GODS: 13F, THE UNITED STATES OF AMERICA, AND THE TOP INSTITUTIONS ARE BEGINNING TO RIVAL EACH OTHER

IN 2026, Q1, THE TOP INSTITUTIONS DID NOT GIVE UP AI, BUT THEY NO LONGER BOUGHT "THE SAME AI"。

2026 Q1, THE RESULTS OF THE SIX BIG FUNDERS' STOWING, CAME OUT。

AS IS WELL KNOWN, EACH YEAR IN MID-MAY, ONE OF THE MOST INTERESTING WINDOWS OF TIME FOR THE GLOBAL UNITED STATES STOCK MARKET, AT WHICH POINT MAJOR INSTITUTIONS ARE REQUIRED TO SUBMIT 13F DOCUMENTS TO THE UNITED STATES SECURITIES COMMISSION (SEC) FOR DISCLOSURE OF THEIR HOLD AT THE END OF THE PREVIOUS QUARTER, ALTHOUGH THE 13F ITSELF IS DELAYED, USUALLY WITHIN 45 DAYS AFTER THE END OF THE QUARTER, AND IS NOT SUITABLE FOR "REAL-TIME COPYING" PURPOSES, BUT IT IS WELL SUITED FOR OBSERVERS TO RE-UNDERSTOOD THE MAIN MARKET LINE IN THE LAST QUARTER。

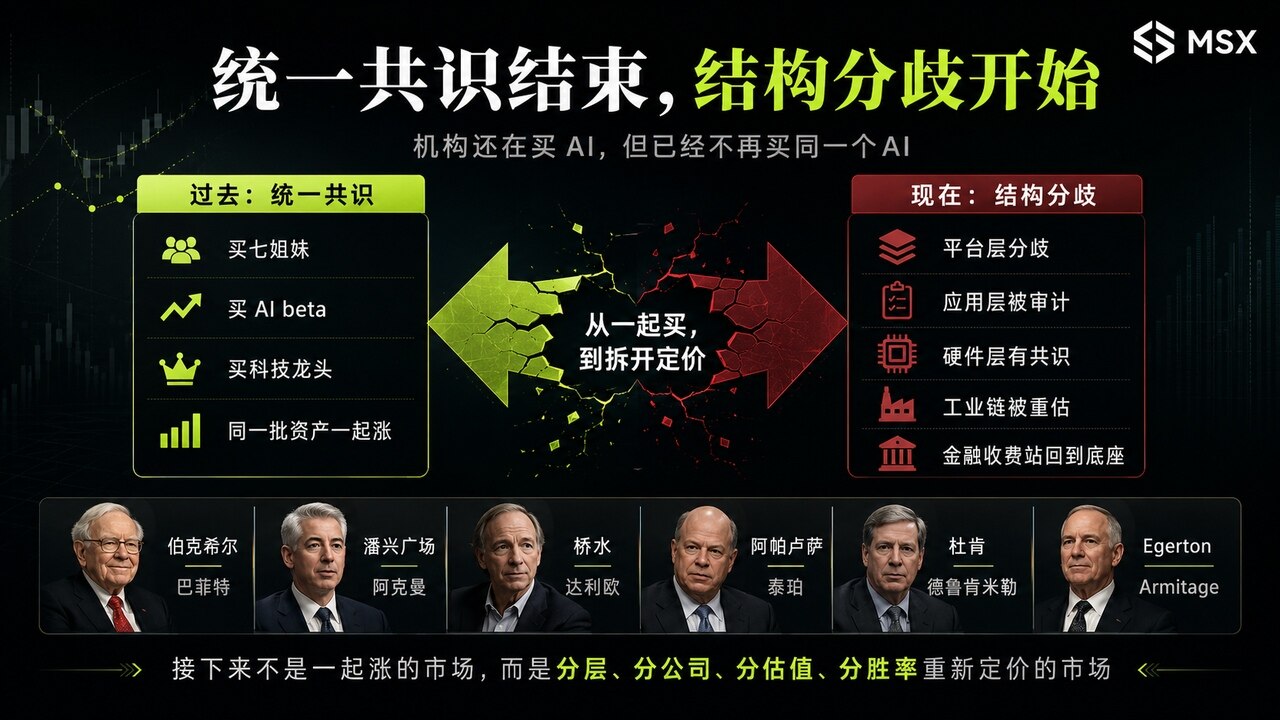

AND THE FIRST QUARTER OF 2026, 13F, THE MOST IMPORTANT CHANGE WAS NOT WHO BOUGHT THE STOCK, OR WHAT SOME BIG GUY CLEANED UP, BUT..The consensus between Wall Street's top funding is starting to break。

Because over the past few years, the US stock market has a very clear common narrative: buy seven sisters, buy an AI, buy platforms, buy high-quality technology. The financial direction, though sequenced, is largely the same, but this time it is different — again Google, where people are crazily stowing, where people are almost clearing; Amazon, where people are sold out completely, where people continue to retort; Microsoft, where new core positions are built, where people are removed directly; and the traditional SaaS, which is heavily liquidated by bridge water, where AI hardware and computing infrastructure are purchased by another group of funds。

THIS SUGGESTS THAT THEIR JUDGMENT AS TO “WHAT LEVEL OF MONEY WILL EVENTUALLY GO TO” “WHICH COMPANY WILL BE RE-EVALUATED BY AI” “WHICH VALUATIONS ARE OVERSTRETCHED IN THE FUTURE” IS BEGINNING TO BECOME QUITE DIVIDED。

SO THIS TIME, 13F ISN'T A SIMPLE HOLD-UP LIST, IT'S MORE LIKE A WALL STREET RIVAL MAP。

I. Core change: the consensus has moved from "what to buy" to "who's picking up who?"

THIS TIME, ONE OF THE MOST OBVIOUS TRENDS OF INTEREST IS THATTHE AGENCY HAS ALREADY BEGUN TO DO RIVALRY WITH EACH OTHER WITHIN THE AI MARKER。

IN THE PAST, THE UNITED STATES STOCK AGENCY TRADED MORE LIKE A RIVER IN A SIMILAR DIRECTION, EXCEPT FOR A DIFFERENT SIZE AND RHYTHM. NOW IT'S MORE LIKE A FORK IN THE ROAD, BECAUSE EVERYONE KNOWS AI IS THE MAIN LINE, BUT NO ONE IS WILLING TO PAY THE SAME VALUATION FOR THE SAME STORY:

- Some people buy Google because it's cheap, cash-flowing, YouTube and search still have moats; others sell Google because the AI search can hit its core business model

- Some buy Microsoft because Azure and the Enterprise AI portal are more certain; others clean Microsoft because the market has already given it an excessive AI premium

- THE PURCHASE OF AMAZONS IS DUE TO THE FACT THAT AWS REMAINS THE CORE PLATFORM FOR AI CLOUD CAPITAL EXPENDITURE; THE SALE OF AMAZONS IS DUE TO THE FACT THAT THE PORTFOLIO NO LONGER REQUIRES SUCH HIGH-VALUE PLATFORM RISKS

- Some fled Salesforce and Servicenow because traditional SaaS middlemen ' s values were being compressed by AI; some bought NVIDIA, station power, beauty light, Sandisk because bottom hardware was to be bought first regardless of which AI application won

SO THE CORE OF THIS 13F IS NOT "BUY AI"。

It's..AI, AS A UNIFIED CONCEPT, IS BREAKING DOWN AND INSTITUTIONS ARE BEGINNING TO RE-PRICING IT INTO PLATFORM LAYERS, APPLICATION LAYERS, HARDWARE LAYERS, INDUSTRIAL CAPITAL EXPENDITURE LAYERS AND FINANCIAL TOLLHEAD LAYERS。

Let's go to the house first。

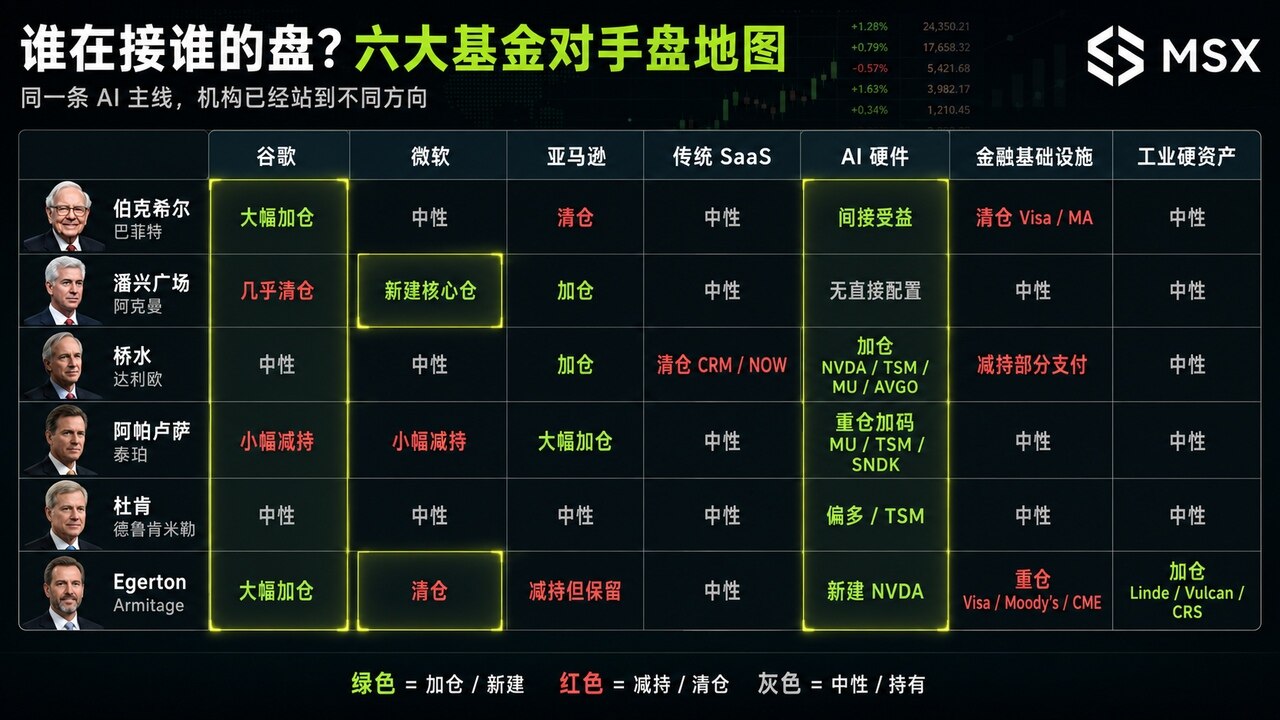

1. Birkhel: Reline in the post-Buffet era

OBJECTIVELY SPEAKING, 2026 Q1 WAS THE FIRST COMPLETE OBSERVATION WINDOW AFTER BURKE HILL ENTERED THE BUFFET ERA。

AND THE MOST INTERESTING THING ABOUT THIS 13F IS THAT IT DOES TWO SEEMINGLY CONTRADICTORY THINGS AT THE SAME TIME:On the one hand, the combination has been considerably streamlined and on the other hand, the Google has been significantly enhanced。

According to public reports, the Alphabet holdhouse was significantly upgraded in the first quarter of Birkhel, along with the construction of new warehouses such as Dammeh Airlines and Messi, and the removal of more than one hold in Amazon, Visa, Mastercard, United Health:

- (a) The clean-up of Amazon, Visa, Mastercard, indicating that it does not want to continue to maintain all business models that used to look good

- Kala Google, which means that it is not away from technology, but rather that it is looking for assets that are closer to the traditional aesthetics of Birkhel, i.e., strong cash flows, unvalued valuations, sufficiently controversial, but that the bottom line business has not yet been fully false

AND THAT'S WHY GOOGLE BECAME THE BIGGEST POINT OF DISAGREEMENT FOR THE 13F, AND BURKE HILL BOUGHT NOT AN "AI STORY" BUT A CASH-FLOWING GIANT RE-SUSPECTED BY THE MARKET, STANDING ON THE SIDE OF THE "GOOGLE RIVER STILL HAS VALUE."。

Panhing Square: Ackerman stands across from Buffet

If Burke Hill was one of the biggest buyers of Google this time, Ackerman was the most typical opponent。

Pansing Square Q1's most striking move was the near clearing of Alphabet and the creation of a new Microsoft warehouse, while Ackerman's public explanation emphasized that Microsoft experienced a more attractive valuation of stock prices and that the long-term growth potential of Azure, Microsoft 365 and Enterprise AI remained strong, in other words, he cut the technology open from Google to Microsoft。

This is in stark contrast to Birkhel, which, in the end, sees the resilience of Google searches, YouTube, clouds and advertising cash flows, and Ackerman sees the risk of generating AI's subversion of the search portal。

One thinks Google has been underestimated, one thinks Google's moat has been re-pricing, or straight whiteACKERMAN DIDN'T GIVE UP AI, HE JUST THOUGHT GOOGLE WASN'T THE MOST WINNING CARD IN THIS AI DEAL。

3. Bridge Water Fund: Dario is selling software and buying hardware

THE BRIDGE WATER FUND 13F HAS ALWAYS BEEN COMPLEX BECAUSE IT IS NOT A SINGLE CORPORATE JUDGEMENT, BUT A MACRO CONFIGURATION。

But this bridge water is very clear:SELL TRADITIONAL SOFTWARE, BUY AI HARDWARE。

Open 13F tracking shows that bridge water exits in the first quarter of Salesforce and is clearly in the direction of AI hardware and infrastructure such as NVIDIA, power builders, Amazon, etc.; some market reports also mention the importance of the power build as one of the major new warehouses of the bridge season, and the importance of the line as the main exit route。

It suggests that the bridge water is not simply multi-technology, but rather a chain exchange within the technology. Over the past decade, traditional SaaS has been one of the most comfortable business models: subscription income, customer viscosity, high Māori, good cash flow, but the valuation logic of traditional SaaS began to be re-evaluated when AI emerged。

If large models can automatically generate codes, automatically complete processes, and automatically replace some of the enterprise software functions, the value of the traditional SaaS middle layer will be reduced, so bridge water will not retreat from the technology unit this time, but rather from "software brokers" to "AI hard currency."。

THE COMMON DENOMINATOR OF ASSETS SUCH AS NVIDIA, UTILISATION, LUMINARIES, LUMINUM, AMPHIBIANS, AND AMAZONS IS THAT, REGARDLESS OF WHO WINS THE AI APPLICATION, THE BOTTOM CAPITAL SPENDING RATE GOES THROUGH THESE LINKS。

In conclusionBRIDGEWATER IS NOT BUYING THE AI CONCEPT, BUT BUYING THE AI MUST SPEND THE MONEY。

4. Apalusa: The bet on Tepper is "hardware for no one."

DAVID TEPPER'S APPALUSA ALSO GAVE A VERY STRONG DIRECTION IN Q1。

Public reports indicate that in the first quarter, Appalusa substantially stoked Amazon and Uber out of the aviation unit and added Sandisk, while continuing to increase the exposure of semiconductors such as Micron, desk power and AI hardware chain assets。

It's very directAI, IT DOESN'T MATTER WHO WINS IN THE END, FIRST BUYS WHAT ALL WINNERS HAVE TO BUY:

- MIRROR REPRESENTS HBM AND MEMORY

- (a) Power generation represents advanced production and generation

- Sandisk represents the storage chain

- AMAZON FOR AWS CLOUD INFRASTRUCTURE

THESE ARE NOT PURELY AI APPLICATIONS, BUT AI HARDWARE, CLOUDS AND INFRASTRUCTURE IN THE ARMS RACE, WHICH, OF COURSE, IF YOU LOOK CLOSELY, OVERLAPS WITH BRIDGE WATER, BUT WHO IS MORE FOCUSED AND AGGRESSIVE。

OR RATHER, BRIDGE WATER IS A MACRO-CONFIGURATION OF "HARDWARE, SOFTWARE DOWN," AND TEPPER IS MORE LIKE A DIRECT BET THAT THE AI CALCULATOR CYCLE IS NOT OVER, AND THE REAL ONES THAT GET ORDERS AND CASH FLOWS ARE HARDWARE AND INFRASTRUCTURE CHAINS。

In a summaryTaper buys shovels, and they're the ones that sell shovels the closest to math bottlenecks。

5. Duken House Office: The signal from Druken Miller is "no hot spots."

The Ducken family's office in Drukken Miller is different from the previous ones。

IT'S NOT THE MOST TYPICAL BIG BUYER OF AI HARDWARE THIS TIME, BUT IT'S IMPORTANT TO REPRESENT ANOTHER INSTITUTIONAL IDEA, NOT TO STAY TOO LONG IN THE MOST CROWDED PLACES。

In fact, Drukken Miller has in the past reduced or withdrawn from popular AI concepts such as NVIDIA, Palantir, while maintaining attention to more upstream assets in industrial chains such as desk power, and public reporting also shows that these macro-trading types of finance, Duquesne, are characterized by rapid adjustment rather than a long-term story。

THIS IS IN LINE WITH THIS 13F MAIN LINEWHEN THE MARKET CREATED A CONSENSUS ON AI APPLICATIONS, TRULY SENSITIVE MACRO-FINANCE HAD BEGUN TO MOVE TO A MORE UPSTREAM, LOWER, CHEAPER LINK。

In conclusion, he does not stand in the most crowded places, but goes ahead where the market is not fully priced。

Egerton Capital: Clean Microsoft, Google, In Weida and Industrial Hard Assets

Egerton Capital bought not only AI, but also financial infrastructure and industrial hard assets, and, more importantly, it cleared the microsoft to the opposite side of Ackerman。

Public 13F tracking shows that Egerton Capital combined approximately $9 billion in the first quarter, with the top five holding warehouses including Visa, Alphabet, Moody's, Linde and Carpenter Technology; and also new or upgraded NVIDIA, Linde, Devon Energy, Canadian Natural Resources, etc。

It's an interesting group, not just to buy seven sisters, but to divide the combination into several lines:

- The first line is financial infrastructure: Visa, Moody's, CME, Interact Brokers, Mastercard

- The second line is AI platform and algorithm: Alphabet, NVIDIA

- The third line is industrial hard assets and capital expenditures: Linde, Vulcan Materiels, Carpenter Technology, Amphenol

- Line 4, energy and resources: Devon Energy, Canadian Natural Resources

This suggests that Egerton is not buying an AI story, but is buying an AI cycle, industrial capital spending and a financial toll。

The key is that it's soft, and it's very clear to Ackerman。

Ackerman believes that Microsoft is more successful at the AI Enterprise entrance and at Azure, so a new Microsoft is being built; Egerton chooses to clear Microsoft and place more technology in Google and NVIDIA。

IT'S ALSO AI, IT'S ALSO QUALITATIVE GROWTH, AND THE ANSWERS FROM DIFFERENT AGENCIES ARE COMPLETELY OPPOSITE。

II. Horizontal comparisons. Who's playing the opponent

GOOGLE: CURRENT ROUND 13F TOP SAMPLE OF DISAGREEMENTS

We can say that:Google is one of the most unique assets in the 13F: Birkhel has a huge silo, Egerton has a silo, Alphabet, but Ackerman has almost cleared it。

This suggests that Google has become a divisive asset, from being the leader of consensus technology in the past. Google searches, YouTube, clouds, advertising cash flows are still strong; valuations are relatively less expensive; and AI shocks are over-expanded by the market. On the empty side, it is argued that generating AI may change the search portal; that advertising business models are revalued; that Google Cloud and Gemini need to prove commercialization efficiency; and that capital spending may reduce profitability。

So Google is not simply "the agency is buying" or "the agency is selling" but it's more like a moat pressure test。

WHO BUYS GOOGLE, BUYS CASH FLOW AND LOW VALUATION REPAIRS; WHO SELLS GOOGLE, SELLS AI, SEARCHES FOR THE RISK OF SUBVERSION OF THE OLD ENTRANCE。

2. MICROSOFT: SOMEONE WHO IS AN IA PORTAL TO AN ENTERPRISE IS CONSIDERED TO BE OVERPRICED

Microsoft is also the subject of great disagreement。

Ackerman ' s new Microsoft was created because he saw the long-term certainty of Azure, Microsoft 365 and Enterprise AI; however, Egerton ' s s silo-soft-soft is an indication that another type of institution is not willing to continue to pay an overpaid premium on Microsoft ' s AI platform。

This difference is crucial. Microsoft was not abandoned by the market, but it was no longer an uncontroversial consensus asset。

The question was whether a good company had been overdrafted at a good price. This is also the most likely problem for high-level technology units, and business can continue well, but stock prices have already been set ahead of schedule for the coming years。

3. Amazon: Birkhel, Ackerman and Tepper

The Amazon is not a consensus either。

Birkhel's cleanhouse, Amazon, but Ackerman, Thaper, still valued Amazon, bridge water was placed in a critical position, and Egerton kept a space even if it was reduced。

THE DIFFERENCE BEHIND THIS IS WHETHER AMAZON IS A HIGH-VALUE PLATFORM RISK OR AI CORE INFRASTRUCTURE IN THE CLOUD CAPITAL EXPENDITURE CYCLE

MANY SAW AWS, THE POWER COMPANY'S BASIC DISCS, ADVERTISING OPERATIONS AND AI CLOUD REQUIREMENTS; THE LIGHTWEIGHT SAW STREAMLINED COMBINATIONS, VALUATION DISCIPLINE AND REBALANCING OF PLATFORM ASSETS。

So Amazon is not a moat dispute like Google, it's more like a "assembly position dispute," and the agency wonders whether this kind of Amazon opening is needed under the current price and combination structure。

4. Traditional SaaS: from security assets to audited assets

The bridge water silos, Salesforce and Service Now, are one of the most structured actions in the 13F。

Rather than simply selling two shares, it represents a re-examination by the market of the traditional SaaS business model, because in the past SaaS was a high-quality asset that earned money from subscriptions, viscos, data and processes, but the middle-level value of enterprise software began to be challenged by the broader AI model。

If many processes can be automatically completed by AI, many codes can be generated by AI and many software functions can be directly accessed by large models, the traditional SaaS high valuation needs to be re-explained。

AND THAT'S WHY, THIS TIME, TRADITIONAL SOFTWARE AND AI HARDWARE FORMED A VERY VISIBLE RIVALRY, SELLING THE MIDDLE LAYERS OF SOFTWARE AND BUYING COMPUTING, MEMORY, PROXY, CLOUD AND HARDWARE INFRASTRUCTURE。

5. Financial infrastructure: Birkhel, Egerton

Visa and Mastercard also had interesting differences。

Wisa and Mastercard, but Egerton’s first hold is Visa, who also holds financial infrastructure assets such as Moody’s, CME, Interactive Brokers, which means that the charge point has not lost value。

It was just that different bodies had been divided about its location in the configuration. Birkhel may be doing a combination of clean-up and a thin old warehouse, while Egerton views assets such as Visa, Moody's as a long-term cash flow base。

So, it's not a simple "payment stock goes bad," but..Financial infrastructure is no longer an intellectual consensus, but it remains a high-quality base in the eyes of some institutions。

HOW EXACTLY DO WE UNDERSTAND THIS

A LOT OF PEOPLE WOULD SAY, "THIS TIME, 13F LOOKS LIKE IT'S STILL BUYING AI. HOW CAN WE SAY CONSENSUS IS GONE

The point isThe AI consensus is still there, but the AI Beta consensus is gone。

IT'S COMMON KNOWLEDGE THAT BUYING AI, BUYING SEVEN SISTERS, BUYING A TECHNOLOGY LEAD, BUYING A SEMICONDUCTOR ETF, IS PROBABLY KEEPING UP WITH THE MAIN LINE, BUT IT'S DIFFERENT NOW。

AI HAS BEEN DISMANTLED, SUCH AS PLATFORMS, APPLICATION LAYERS, HARDWARE LAYERS, CLOUDS, INDUSTRIAL CAPITAL EXPENDITURE LAYERS, AND FINANCIAL TOLLHEAD LAYERS, WHICH MEANS THAT THE FUTURE WILL NO LONGER BE AN "AI BOOM" AND THE MARKET WILL BE ASKING MORE AND MORE QUESTIONS。

IN SHORT, THIS IS THE REAL SIGNAL OF THE 13FAI TRANSACTIONS FROM GENERALIZATION TO HIERARCHY。

At the same time, the divide about Google is also a very typical new signal that no one has a eternal moat。

You know, Google used to be one of the strongest moats, but after the generation of AI, it had to be re-audited. This does not mean that Google is not going to work. On the contrary, Birkhel and Egerton Kaoriya are saying that there are institutions that believe that the market is too pessimistic about Google; but Ackerman is saying that another type of agency believes that changes in the search business model cannot be ignored。

This is a truly mature market, not for everyone to believe in the same moat, but for everyone to retest old beliefs with new information。

In addition to thisMICROSOFT, GOOGLE, AMAZON, NVIDIA, STATION POWER AND BEAUTY LIGHTS CAN BE GOOD COMPANIES, BUT GOOD COMPANIES DO NOT EQUAL GOOD PRICES。

In this institutional move, valuation discipline is evident: Birkhel cashed some of his assets at a high level; Ackerman bought them after Microsoft's turn back; Egerton siloed Microsoft but siloed Google and NVIDIA; and Thaper bets on hardware, but also trims some of his high technology exposures。

This means that big money is not simply superstitiousThis quality, combined with the current price, gives a sufficient rate of compensation。

Finally, there is a commonality that this time many agencies are streamlining their portfolios, like Birkhel and Apalusa, which are reducing their holdings, Pansing Square, which is already extremely concentrated, and Egerton, which has almost a billion dollars, has only 20 American stockholdings。

This means that in high-market markets, the real big money is not necessarily more dispersed, but more concentrated, because the more the differences, the less the problem can be solved by buying everything。

You have to know what floor you're buying, what risks you're taking, who the opponent is, and why the market re-pricing it。

IV. What is the message for us

I THINK THAT THIS TIME 13F IS OF MAXIMUM VALUEWho's buying, who's selling, who's picking up his plate。

It is a consensus if one asset is purchased by all agencies; it is a disagreement if one asset is bought by some of the top money and another is sold by others。

Differing assets are more worthy of study than consensus assets, as real excess gains often occur when markets do not yet have a uniform answer。

Google is a typical example。

Birkhel and Egerton stood by the buyer, Ackerman stood by the seller。

IT'S NOT ABOUT CHOOSING ONE SIDE. IT'S ABOUT REMINDING YOU THAT YOU HAVE TO ANSWER ONE QUESTION. - DO YOU THINK GOOGLE'S SEARCH OF THE MOAT WAS PERMANENTLY WEAKENED BY AI, OR WAS IT SHORT-TERM UNDERVALUED BY THE MARKET

If you can't answer, don't copy。

IT'S ALSO IMPORTANT THAT IN THE FUTURE AI CAN'T JUST ASK IF IT'S AN AI CONCEPT, BUT AT LEAST THREE LAYERS:

Platform level: including Microsoft, Google, Amazon, Meta. They look at entrances, clouds, advertisements, cash flows and ecological positions

Application level: includes Salesforce, Servicenow, Adobe, Palantir, etc. See if AI enhances it or replaces it

Hardware and infrastructure layers: including NVIDIA, desk power, aesthetics, cartoons, Sandisk, Oracle, as well as electricity, industrial gases, materials, data centre chains, and in general capital expenditure, capacity bottlenecks and orders。

In generalTHIS IS NOT ALL AI, BUT HARDWARE AND INFRASTRUCTURE; THE MOST DIVISIVE IS THE PLATFORM LEVEL; AND THE MOST STRESSFUL IS TRADITIONAL APPLICATIONS。

And let us remind ourselves not to use the term "possession of a long time" as a reason for not selling. This time, Ackerman's clean-up Google, Burke Hill clear-up, Visa, MasterCard, Amazon, the bridge clear-water warehouse, Salesforce, and Service Now, all point to a real institutional investor, not not to sell for long periods of time。

The standard for selling is not "how long have I been in possession," but is the reason why I bought it

If the moat has changed, cash flows are expected to change, the valuation rate has changed, and the location of the industry has changed, the length of holding cannot justify its continued holding。

The holding period is the result。

Holding is a prerequisite。

Of course, the time has come to streamline the hold-up, and many of them like to open a supermarket-like hold-up — they buy 20 or 30 shares, which they call risk spread。

BUT THIS TIME, THE REAL BIG MONEY IS AT THE TOP OF THE SCALE, BECAUSE THE SIMPLE REASON IS THAT WHEN THE MARKET ENTERS A PERIOD OF DISAGREEMENT, THE DIFFERENCE BETWEEN ASSETS BECOMES LARGER, THE MORE DISPERSED YOU ARE, THE EASIER IT IS TO DILUTE THE REAL ODDS, WHILE BUYING IN RISKS THAT YOU HAVE NOT STUDIED。

If you cannot describe in three sentences the core competitiveness, the main risks and the current rate of compensation for a stock, it should not be in your core slot。

FINALLY, THIS TIME, 13F ALSO EXPLAINS THE OLD STORY: CASH IS NOT WASTE IN HIGH MARKETS。

BIRKHEL'S HIGH-LEVEL ASSETS, THAPER'S HIGH-TECH CUTTING, AND DRUKKEN MILLER'S NOT INTO THE HOT SIDE OF THE WAR, AI, ARE ALL DOING THE SAME THING, AND THAT'S NOT GIVING HIMSELF THE RISK OF BEING BEATEN IN THE MOST CROWDED TRADE。

When the short-term increase in a popular beacon is too large and valuations are clearly overspent over the next two years, the best discipline is not to fantasize at the highest point, but to convert profits into cash in batches。

The value of cash is not reflected when it rises, but when the market suddenly falls non-linear。

At the end

IF THIS IS SUMMED UP IN ONE SENTENCETHE AGENCY IS STILL BUYING AI BUT NO LONGER BUYING THE SAME AI。

SO, THIS TIME, THE 13F REALLY TOLD US NOT TO COPY THE BOSS, BUT..When top-level institutions are beginning to compete with each other, it is even more important for ordinary investors to look beyond conclusions and to see clearly the assumptions behind each transaction。

The consensus did not disappear completely, but the consensus was over, and then the United States share was no longer a growing market together, but rather a market with layers, branches, valuations, victory pricing。

Let's meet the new wind together。