$500 FOR SILICON VALLEY'S SHAREHOLDERS? NEW FUND FOR THE DISMANTLING OF NAVAR

Did you buy a fund or Nawal's attention?

The most famous angel investor in Silicon Valley, Navar, has just made a new fund. Unlike the 400 companies he had personally voted for in the past (Uber, Twitter, Notion), this time you can vote。

There is no need to be a millionaire, no need to be related, no need to be certified as a "qualified investor" in the sense of US securities law. With 500 dollars, you can buy shares in OpenAI, Anthropic, XAI, SpaceX。

Its name is USVC (United States Venture Capital), built by AngelList, and Navarre himself chairs the Investments Committee. When AngelList went online last night, AngelList received 2.75 million browsing and Navarre long browsing 2.25 million browsing. They have a big tagline for this fund, the American People's Endowment Fund。

Sounds like a complete financial equality. But it's more complicated than propaganda。

500 dollars for a silica topstream

The long thrust announced on the line was written by Nawal himself, and the texture is the classic Nawal, short sentences, adages, historical analogy。

He started in the 1500s, and then gave a comparison between the median age (6 years) of American companies listed in 1980 and the median age (13 years) of companies listed today, meaning that the bulk had grown in the open market, and today most of them were locked in private fundraising。

And the whole tweet ends up in a kind of fatalism adage, "In the future, either you tell the computer what to do or the computer tells you what to do." You don't want to be on the wrong side of that deal. "The narrative is as beautiful as Silicon Valley's last carefully written ad。

ONE OF THE HARD RULES OF THE US PRIVATE MARKET OVER THE LAST FEW DECADES IS THAT IF YOU WANT TO INVEST IN UNLISTED COMPANIES, YOU HAVE TO PROVE THAT YOU ARE A “QUALIFIED INVESTOR” – A THRESHOLD THAT KEEPS THE MAJORITY OF ORDINARY PEOPLE OUT OF VC。

USVC BYPASSED THE DOOR BY DIRECTLY REGISTERING ITSELF AS A CLOSED FUND UNDER THE INVESTMENT COMPANIES ACT OF 1940. THIS IS THE SAME LAW APPLICABLE TO THE UNITED STATES COMMON FUND AND ETF. ONCE REGISTERED, THE FUND IS SUBJECT TO A STANDARDIZED AUDIT AND PERIODIC DISCLOSURE OF FINANCIAL STATEMENTS, BUT THE PROCEEDS ARE OPEN TO ALL WITHOUT A REVIEW BY A QUALIFIED INVESTOR, AND A TAX FORM OF 1099 IS ISSUED ANNUALLY, WHICH IS MUCH MORE FRIENDLY TO INDIVIDUAL INVESTORS THAN THE K-1 FORM THAT IS COMMON TO PRIVATE FUNDS。

A figure of $125.0 billion is repeated in USVC propaganda. This is the cumulative asset currently carried by AngelList. AngelList, since its founding in 2010 as a co-founder of Navarre, has evolved into a bottom-up infrastructure for private investment in the United States, with over 4,500 active fund managers and over 25,000 operating foundations, supporting over 13,000 active start-up companies。

The USVC's GP Ankur Nagpal expressed this as our "unfair advantage" in the announcement of USVC's tweets, translating it as the ability of USVC to select shares, not from Nawal or Ankur alone, but from using AngelList's data stream and manager's network as a screen。

Ankur Nagpal is the day-to-day management of USVC, the founder of the online educational platform Teachable, is now the PPP of USVC, and also the founder of the AngelList Internal Emerging Fund, Vibe Capital. The role of Navar in the USVC is that of the Chairman of the Investments Committee, who is responsible for shaping investment strategies but not for day-to-day decision-making。

The consultant seat also included several old faces of Silicon Valley. Cyan Banister, former Funders Fund Partner, Ariele Zuckerberg, previously invested in hedge funds Coatue and Kleiner Perkins, founder of Jeff Faganan, Accomplice Foundation, early on in Carbon Black, BillPack, Whop。

THE LIST ITSELF IS A SIGNAL THAT THE USVC WANTS TO SEND TO RETAIL INVESTORS: WE'RE NOT CASUAL BULK PROPERTY, WE'RE BEHIND AN ENTIRE MATURE VC CIRCLE。

OPEN THE LID, USVC. WHAT'S IN IT

USVC IS STRUCTURALLY DIFFERENT FROM OUR USUAL ETF, MUTUAL FUNDS. IT IS A PERMANENT CLOSED FUND WITH NO FIXED DURATION AND SHARES NOT TRADED IN SECONDARY MARKETS。

COMPARED TO THE TRADITIONAL VC FUND, IT DOES NOT HAVE A LOCK TERM OF 10 TO 15 YEARS. COMPARED TO ETF, ITS SHARE DOES NOT APPEAR ON ANY EXCHANGE, NOR DOES THE PRICE FOLLOW THE MOODS OF THE SECONDARY MARKET, BUT FOCUSES ON THE FAIR VALUE OF THE BOTTOM COMPANY。

THIS STRUCTURE GIVES A "SOUNDINGLY REASONABLE" YIELD CURVE, AND IT DOESN'T GET BEAT UP EVERY DAY LIKE THE PUBLICLY TRADED ETF, AND IT DOESN'T LEAVE YOU LOCKED UP FOR TEN YEARS LIKE THE OLD VC FUND。

ACCORDING TO THE OFFICIAL NETWORK, USVC'S INVESTMENT STRATEGY IS DIVIDED INTO THREE PATHS:

First, to other fund managers. USVC, in its capacity as LP, will contribute to the new and emerging fund manager on AngelList platform. This is the main path for USVC to get openings in the early stages。

ARTICLE II, ADDITIONAL GROWTH WHEEL. WHEN ONE OF THE COMPANIES IN THE PORTFOLIO COMES OUT, THE USVC WILL TRY TO HOLD UP THE NEXT ROUND SO THAT ITS SHARE IS NOT DILUTED AS THE COMPANY CONTINUES TO FINANCE。

Article III, Second share. Through AngelList’s network, private equity shares have been purchased directly from existing shareholders and have been advanced。

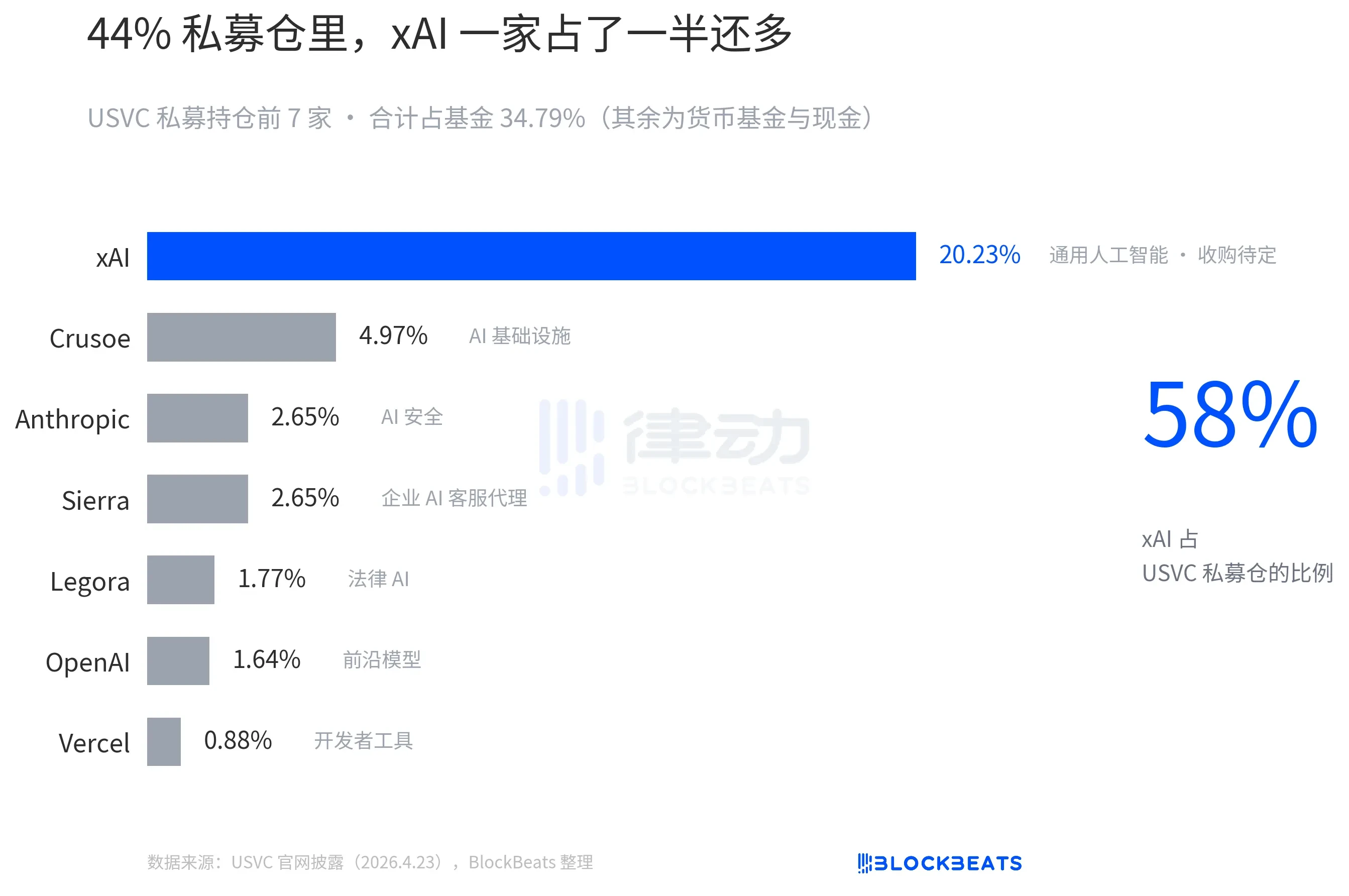

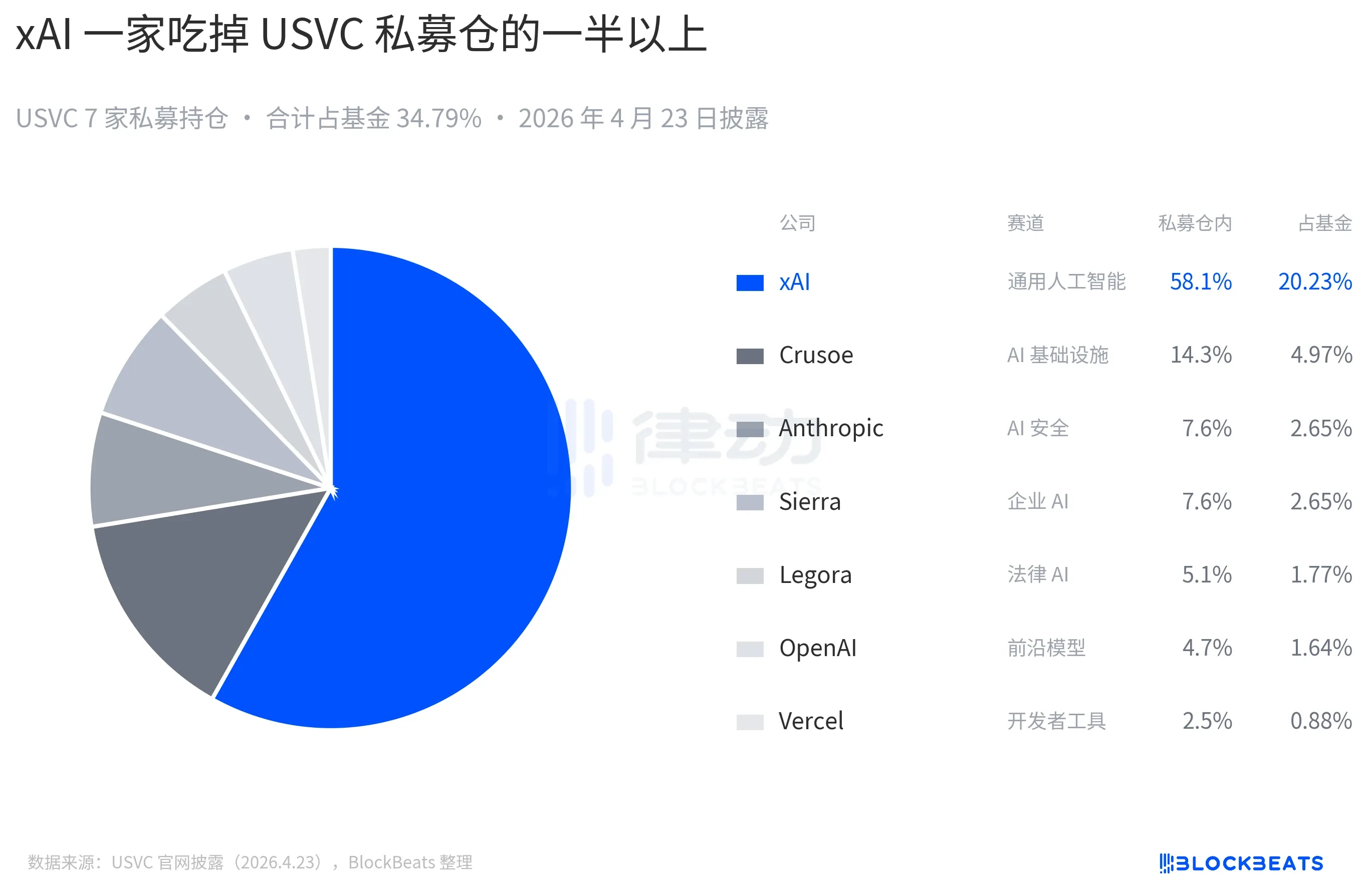

The three paths have a hidden meaning, and USVC is essentially closer to a FOF, not a direct-investment fund. Most of its money goes not directly to OpenAI, Anthropic's shareholders' lists, but first to other fund managers, then to those fund managers。

The USVC official network currently discloses a holdup of OpenAI and Anthropic, but the largest share is XAI:

USVC SHARES ARE NOT LISTED ON ANY NATIONAL STOCK EXCHANGE, SO YOU MIGHT ASK, HOW DOES USVC GET INVESTORS BACK

THE ANSWER IS A QUARTERLY BUY-BACK OFFER, WITH THE FUND BEING ENTITLED TO INITIATE A QUARTERLY BUY-BACK AT ITS OWN INITIATIVE, WITH A MAXIMUM OF 5 PER CENT OF THE FUND ' S NET ASSET VALUE. BUT THIS IS THE "DISCRETIONARY" OF THE BOARD, NOT THE CONTRACTUAL OBLIGATION. IT'S A BETTER MIDDLE GROUND THAN ETF BUT BETTER THAN TRADITIONAL VC. FOR READERS, IF YOU'RE IN A RUSH TO USE MONEY ONE DAY, THE USVC SHARE WILL NOT ACTUALLY MATERIALIZE。

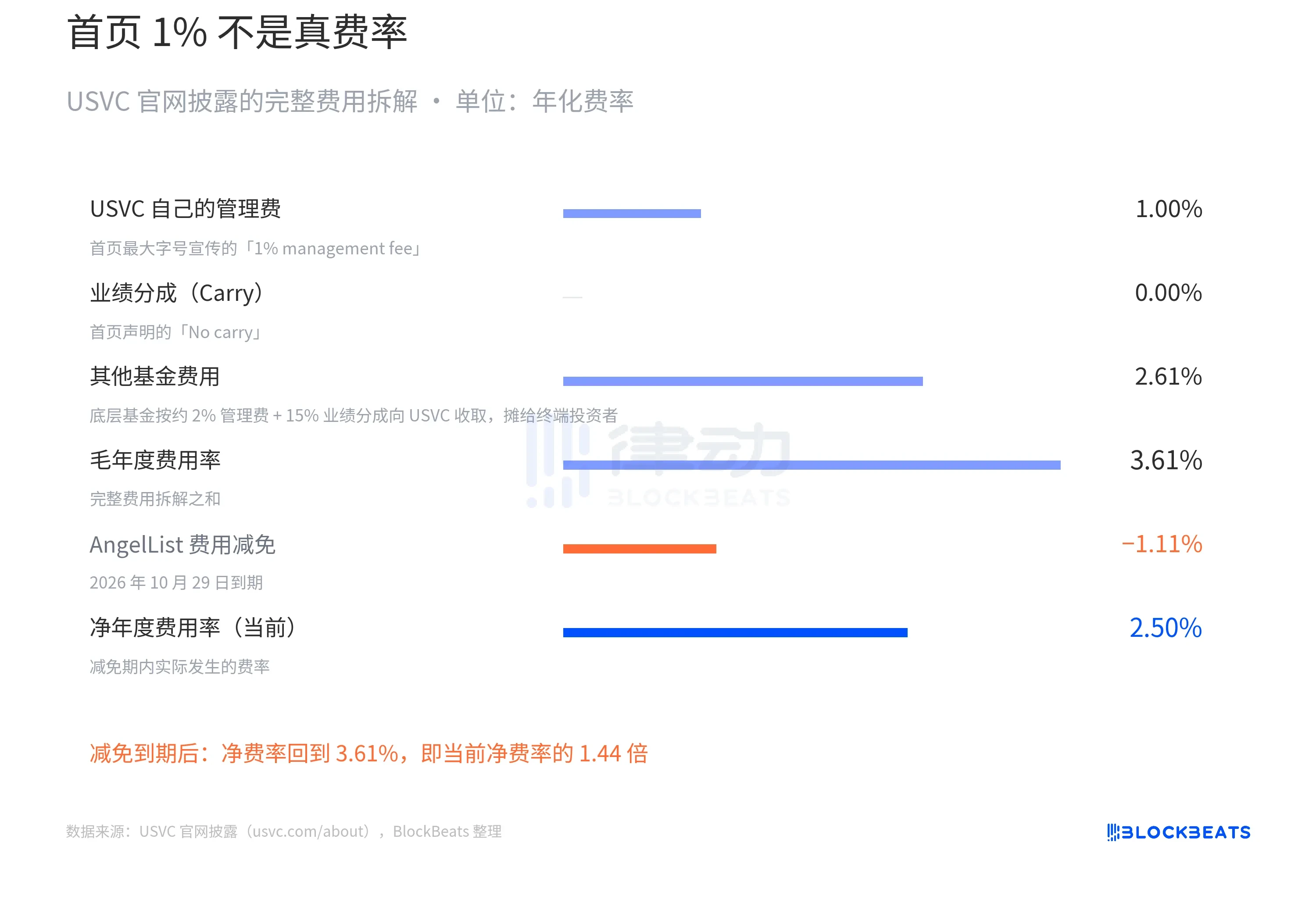

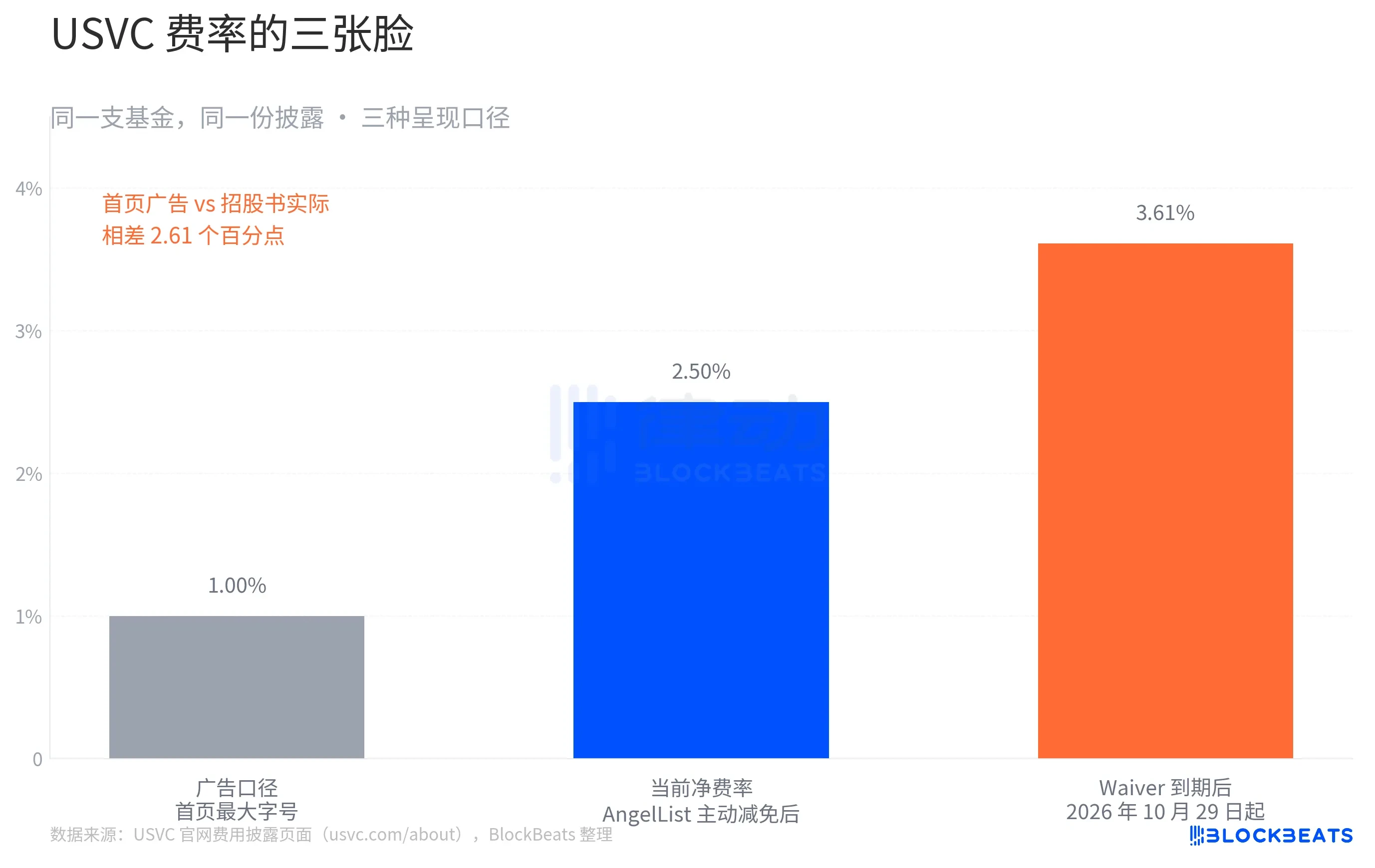

THE MOST INTERESTING THING ABOUT THE WHOLE USVC STORY IS ITS TARIFF STRUCTURE。

AT THE TOP OF THE OFFICIAL WEB PAGE, USVC WROTE A LINE WITH THE LARGEST WORD: "1% MANAGEMENT FEE, NO PERFORMANCE SCORE." AND THEN THE TRADITIONAL VC'S 2% MANAGEMENT FEE WAS COMPARED。

THIS IS USVC'S AD FACE. TURNING TO THE COST BREAKDOWN AT THE BOTTOM OF THE SAME PAGE, THE STORY CHANGED. THE FULL COSTS DISCLOSED BY USVC ARE BROKEN DOWN AS FOLLOWS:

WHAT IS "OTHER FUND COSTS 2.61%"? AND THAT'S THE FIRST OF THE THREE PATHS THAT USVC SAID BEFORE, TO INVEST IN OTHER EMERGING FUND MANAGERS, WHO THEMSELVES CHARGE USVC 2% OF MANAGEMENT FEES AND 20% OF PERFORMANCE. THE COSTS ARE USVC AS AN LP TO PAY FOR THE FINAL DISTRIBUTION TO THE END INVESTORS。

So the USVC net rate should actually be 2.5%. This is not the final form. There is also a key qualification for the network, which AngelList agreed to provide for some of the costs and part of the operating expenses until at least 29 October 2026, but at a rate of 3.61 per cent directly after the expiration of the reduction。

Assuming 12 per cent of gross annualized annualized gross proceeds at the bottom of the USVC, the median level for the VC at the first line of the last decade. During the Waiver period, the net rate was 2.5 per cent, the investor ' s net return was about 9.5 per cent, the Waiver ' s net rate returned to 3.61 per cent and the investor ' s net return was about 8.4 per cent

Ten years of compound interest, $10,000 became $24,800 and $22,400, respectively. Gap US$ 2,400, equivalent to 24 per cent of the initial principal。

IT'S NOT A FAKE STORY. ALL THE NUMBERS ARE CLEARLY WRITTEN IN THE USVC OFFICIAL NETWORK'S COMPLIANCE DISCLOSURE PAGE. BUT THIS GAP DESERVES TO BE TOLD ABOUT A FUND THAT PLAYS "FINANCIAL EQUITY"。

Behind the narrative, is this really "publicizing investment"

Aakash Gupta, a relatively well-known analyst in the Silicon Valley industry, went directly to extract documents that USVC disclosed to SEC. He found that, as at 31 December 2025, the total size of the USVC Fund was only $8.3 million. Of the 8.3 million, 56 per cent (about $4.65 million) fell in a government money market fund with a return of 3.6 per cent。

There is a clear contrast between this number and the formation of the seven star companies on the front page of the website. What you see is OpenAI, Anthropic, XAI, SpaceX, and you might think your $500 would go to these companies at roughly the same rate. But the fact is that the total size of the Fund under the SEC is less than $10 million, more than half of which is short-term national debt。

This is of course a reasonable explanation: the Fund has just been established, cash deployment takes time, and Ankur later mentioned in his tweets "there are also a number of potential new projects in Pipeline."。

THERE IS ALSO A COMMUNITY VIEW THAT CRITICIZES USVC AS THE NEW "MOBILITY OUT OF ART" OF NAVARRE, ARGUING THAT USVC IS NOT ACCESS, BUT A DISTRIBUTION MECHANISM, WHICH DISTRIBUTES THOSE SLOTS THAT HAVE ALREADY GONE UP。

Over the past decade, private fund-raising valuations have achieved a major increase, from 86 billion to 500 billion over three years, and from 24 billion to more than 20 billion over 18 months. There are already several precedents on the open market that suggest that private fundraising may be excessive: Figma fell by 50 per cent for two weeks on the market, and Klarna fell from $46 billion to $6.7 billion on the market. In this context, it is more like "distribution" to sell the warehouse space to the diaspora。

QUARTERLY REPURCHASE CAPS OF 5 PER CENT APPEAR TO BE FRIENDLY UNDER NORMAL MARKET CONDITIONS. HOWEVER, ASSUMING THAT THERE WAS A MAJOR REVERSAL IN THE MARKET IN 2027, THE VALUATION OF PRIVATE CORPORATIONS AT THE BOTTOM OF THE USVC FELL, AND SECONDARY SHARE TRANSACTIONS CONTRACTED. AT THIS POINT IN TIME, IT IS THE RATIONAL CHOICE OF THE BOARD NOT TO BUY BACK THIS SEASON, RATHER THAN SELL LOW-VALUE BOTTOM ASSETS TO SATISFY THE BUY-BACK。

Silicon Valley developers and investors Kenn Ejima directly commented that USVC was seen as a fund with a limited window of opportunity, the length of which depended on the length of Navarre ' s seat in the chairmanship of the Commission。

The word "democratization" has appeared several times in the financial history of the past century. A question that has been asked repeatedly is, "Democratized, opportunities or risks?" But this time, it might be, "Did you buy a fund, or did Navarre's attention for years?"