Opens the black box of MM token loan - from the off-site contract to Chain Let's go. Disclosure

by:

original link: https://x.com/agent/status/2055917832890696069

Statement: For the purpose of reproduction, readers can obtain more information by linking to the original language. If the author has any objection to the reproduction, please contact us and we will proceed with the modifications requested by the author. Reproduction for information-sharing purposes only does not constitute any investment proposal and does not represent the views and positions of Wu。

if you've ever doubted, as i did, exactly what tokenomics was writing about, "5% for market distribution," you might want to see the next article. so 5% is it loaned or sold? how much is it? expires or rights? the three questions determine the movement of atcoin over the year, and retail never sees the answer。

Rats

In the spring of 2025, the Movement Labs' MOVE token came online for less than a few months, with a familiar and strange encryption ring。

It's familiar because the script is a standard attcoin: TGE, the high point, the marketer is accused of selling continuously, the projecter publicly denies that the price is given in the most straightforward way。

Stranger, because this time the market agreement itself was reversed. Chat records, term sheet, market-owned warehouses, market rights prices, token lending, are available on Twitter, investigative journalist reports, and community discussions. This is the first time the industry has seen the standard structure of MM loan on a specific project -- a contract for loaning + call option -- – How to turn an agreement that was supposed to be a liquidity service into a free-of-charge outlet for marketers after listening day。

It was only later that Movee was normal in the industry, and someone just leaked the deal. Atcoin's long-discussed “discretion” phenomenon, which is still under constant pressure outside unlock, is mostly based on the same type of agreement. Only most of the time, this type of protocol is locked in PDF files, encrypted Signal groups, and one that only the projecters and MM know about orally。

The evolution of the encrypted market over the past decade, when one of the main lines is said to be the ability — leverage, emptiness, information — of only a few people to move through chain agreements to retail. Sustainable contracts break leverage asymmetries, and agreements like Shortit are breaking empty asymmetries. Bringing the details of MM loan into the chain is breaking the last layer: information asymmetries in the first level of the market。

the triad, the altcoin market has for the first time a price equivalent structure for traditional capital markets。

this article is about the three democratizations: how they happen, why they go together, what happens when they go together。

i. triple asymmetries found in prices

it's not stock. that sounds simple, but almost all the structural problems in the atcoin market stem from a tacit, but rarely stated, fact that it has the shape of a financial market, which is virtually non-existent。

An IPO with a U.S. share will go through SEC review, underwriting agreed prices, roadshow, lock-up period, post-marketing listing rules, and internal downs and downs. Each step has open and enforceable rules. Retail can't play with Goldman Sachs at the same table, but he knows at least what shape the table is -- how much it is -- when the insiders can sell, who is the marketer, and if there are any restrictions on making short。

atcoin is not. almost all key variables are not subject to public disclosure. real and effective circulation, market identity and holding, options, options, unlocking paths - variables that directly determine price expectations are largely outside the view of retail。

this structural opacity has long shaped the three-tier asymmetries in the atcoin market。

The first level is leverage asymmetries. Early encryption markets, especially before 2017, were only available. A retail, even if it's accurate, can only bet in a single-multiplier spot. Projectors, VCs, market traders can magnify dozens of times in the determination of the same direction through off-site lending, derivative tables, and self-financing movements. As a result, even in the open market, the two people with the same information have completely unequaled the actual downable capacity。

The second level is directional asymmetries. Before the renewal of the contract, the encryption market was essentially a market with more than enough. BTC, ETH, and spot loans can barely be constructed to be empty, but atcoin can hardly be completely empty. This creates an odd balance: marginal incentives for all market participants point in the same direction — pull the coin up first. Because only increases can generate returns, narratives, KOL, media, marketing budgets, and incentives for all are the same. Atcoin's long-term narrative-driving roots are in large part the result of its structurally one-way market。

The third level is information asymmetry. Even if retial had access to leverage and empty tools, he still had no idea what price and when to do it -- because he didn't know the real effective flow, he didn't know the number of tokens he borrowed, he didn't know the options, he didn't know the rational choice of MM at different prices. All this information, the program knows, VC knows, MM knows, only retail doesn't know。

Three layers of superstition have created the most stable power relationship in the Atcoin market in the last decade: the project team plus the early VC plus market merchants mastered information and tools, completed the warehouse slots before every rod in retail entered, and finally passed the price risk to unmatched bulkers. It's atcoin, the design of the market, not the ethics of any single project。

The next story is the most memorable structural change in the encryption market in the last decade: how these three layers of asymmetries were broken separately。

CONTINUED CONTINUES — Leverage Democratization

In 2016, BitMEX came online in Seychelles with a product that looked strange at the time: a contract of durability — a derivative that did not have maturity and that fixed the spot price with a funding ring。

This invention does not have a full counterpart in traditional finance. Traditional futures necessarily have maturity dates, which determine their hedge and arbitrage structure. BitMEX removes the due date and introduces the funding rate as a hold-up cost, with an equal engineering value to standardize, liquidate and host an indefinite leverage position。

Until then, encrypt retail, to leverage, to go to a CEX's "leverage spot"... – In fact, it is borrowing money from an exchange, cumbersome processes, non-transparent costs and original clearing mechanisms. Institution has a completely different way of playing: self-employed, OSC lending, moving bricks across the board, and leverage is the label in the toolbox。

Leverage exists long ago. What really changes is its availability. BitMEX provides 100 times leverage that anyone with USDT can open a warehouse. After entering the battlefield in 2019, Cheonan pushed the system to global retail: the interface was simple enough to have only two long/short buttons, the bond rate was automatically calculated, and the clearing line was open to everyone。

in 2021, the cow market completed the final validation of the conversion: the daily turnover of the contract for renewal exceeded the stock. the main location of the encrypted market, price discovery, was transferred from spot to perpetuity。

this transformation has often been discussed as a “discretionary leverage”. that's only half the judgement. it is true that perpetuity has left a large number of scattered households in high leverage, but it is at the same time a tool that retails for the first time on the leverage dimension and insituation is a real match. before it lasts, a retial judged the right direction and his largest position was locked in the cash-for-money ceiling; after continuation, his downside capacity was limited only by his own risk preferences and bond management capabilities。

the increased frequency of liquidation is the price of leveraging democratization. this is a characteristic of the tool itself, not a flaw — a market where retial and institution bet on the table, which would have to make everyone accept the same risk structure。

but eternally only solves this layer. a retail, even if he holds a 100-fold leverage, if he's judging attcoin to fall, probably finds himself without the tools. most atcoin does not last, even if it does, to the point where it's so thin that it's going to eat directly. the leverage and direction of the mainstream currency has been permanently addressed, but both the direction of the altcoin and the information of all the currencies have been left。

This is a problem to be addressed in the next decade。

Right to sell air — democratization of direction

In 2023, it was judged that attcoin would fall -- like an upper-line L1 or higher L1, or an anchored GameFi, or an narrative that was gone -- and you would find a very awkward thing: you had little way of doing it。

Only a few mainstream currencies are covered by the CEX contract. Beyond the pre-market value of 50, atcoin, most of which either had no derivatives or had only one very bad-moving contract – with a thin list of tens of thousands of dollars, a 5 per cent discount, a funding rate permanently in the direction of empty (meaning that you pay a tax every eight hours) and a very unfriendly clearing line. And the result is, even if you're right, the actual betting power is eaten by mobility, and it's not mathematically cost-effective。

As for off-the-shelf lending, it is virtually non-existent on the attcoin - without CEX willing to maintain the borrowing market for longtails, not deep enough, and too risky for lending suppliers。

this causes a long-term structural disorder in the atcoin market: it is a market that can only do more。

Only a few markets can produce a very specific set of equilibrium effects. The marginal incentives of all market participants point in the same direction: the projecters want to rise, the VC wants to rise, the MM wants to rise, the KOL wants to rise, the media wants to rise, and the second-class diaspora wants to rise. When everyone in a market earns money only when it rises, narratives, traffic, marketing, community operations all concentrate on “how to raise prices a little more”. This is a question of incentive structures and does not have to rise to the ethical level。

the deeper consequence is that when no one can bet on it, the market can never be priced down. an effective market requires pessimists and optimists to bet on the same price in order for prices to approximate their fair value. atcoin, for most of the last decade, only the optimists have been able to bet. the only option for pessimists is not to buy, and not to buy leaves no signal on the price。

This is..@youcanshortit This type of problem to be solved by an on-chain working protocol: to empty any token, any point in time, any retail with transparent pricing costs. Its core mechanism could be simplified as follows: an agreement to maintain a lending pool, allowing any token holder to lend the currency to the empty person, an empty person to assume a transparent interest rate (as determined by the supply and demand of the pool, not the CEX black box), an empty, stable currency to be held in the agreement as collateral, an increase in prices being liquidated and a decline in profits。

The mechanism in traditional finance, called security institutions, is a specialized, institutionally open market. In encryption, it has to be on the chain and must be open to retail, because no CEX in the Atcoin market is willing to do this for longtails -- it's not economically worthwhile。

the value of the democratization of the sale of space is easily misinterpreted. most people think it's a way to make money from the crash. this understanding is only a small part of it — it has been a difficult and asymmetrical mathematical transaction, and most dispersed households do not necessarily earn money if they have the tools. what really changes is the other level: when a currency is allowed to be empty, over-optimistic narratives are tested emptyly, and over-pessimistic narratives are tested flatly. the altcoin market is beginning to have a two-way debate。

But even with a two-way tool, retaiil still faces a fundamental problem: he doesn't know what to do at what price and when. Because the most important variable that determines the short- and medium-term supply -- MM hold and option state -- he still doesn't see it。

This is the third level of asymmetries. And it's really the last mile。

MM loan Uplink - Democratization of Information

A. Standard structure of MM loan

To make it clear why MM loan is at the heart of altcoin's information asymmetry, you have to look at its standard structure. The vast majority of retails, even after years in the encryption circle, have only heard the word "marketing" and have never seen a real MM protocol。

the agreement between the projector attcoin and the marketer is almost the same template: Loan + Call Option。

On the eve of TGE, the projecter gave a token (usually 1 to 5 per cent of the supply in circulation) in the form of a loan to MM. “Leave” is important in accounting - the project party does not sell it, so there is no need to disclose the proceeds of sale, part of which token is still classified in the tokenomics files as “distribution to the market” or “liquid reserve”. The duration of the contract is usually between 12 and 24 months, at which time MM has two options: to return the original number of token or to buy it as pre-agreed. This "buy or not buy" option is a financial one that usually falls between 25% and 100% premium of TGE prices。

The contract would also provide for a share of profits, a guarantee clause, market obligations, etc., but Loan + Call Option was a skeleton。

This structure is attractive to both sides. The project party was provided with immediate secondary liquidity without having to sell the currency directly, and there was no sale, tokenomics narrative kept clean. MM is in a more comfortable position: zero costs get a lot of inventory, get a go-up option, barely afford a go-down -- if the price falls TGE, just give it back, and there's no need for impairment. Incentives are asymmetric: the projecter bears the opportunity cost (the currency increases MM ownership, the projector sells less), and the MM gets all the top, almost nothing. That's why the MM business has been one of the most profitable tracks of encryption in the past few years, and little retail knows the exact structure of the business。

B. How the structure is systematically driven

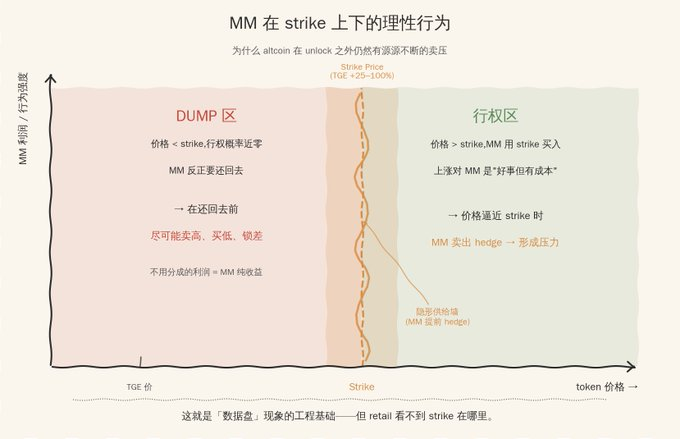

By understanding the structure of the agreement, we can understand why a large number of altcoins are still under constant pressure outside unlock. The key is to look at the rational choice between different price zones。

When prices are much lower than those of strike, MM rights are close to zero -- he won't use a $2 strike to buy a currency that has fallen to $0.5. In this case, the token he held had no long-term value, and sooner or later he had to return it. The rational choice is to sell it as much as possible, buy it back at a lower price, and lock the spread before returning it. Each time, the "high-sale" was token borrowed from the project provider to make a profit. The part that doesn't need to be divided is the net proceeds of MM。

Incentives become more complex when prices approach strike. If you go through the strike, the MM needs to buy a loan from strike price at the end of the period, the increase is good for him but cost. It's rational to sell a hedge ahead of time, to take out a part of the potential right-handle obligation. The effect seen in the market is that a hidden supply wall is naturally formed near the strike, which in turn suppresses price breakthroughs。

The two mechanisms overlap, producing the most common and difficult to explain phenomenon in the altcoin market: the seemingly irregular and continuous pressure on sales outside unlock. Retail saw that the price was falling and could not be attributed to any unlock event -- because the compactor was not the projector, not the VC, and the handheld projector "loaned" token's MM. That part of the token is classified in the tokenomics files as a "liquid reserve" and has an equivalent in transactional behaviour to "already in circulation and continuously under pressure"。

this is the engineering basis for the "disk" phenomenon. so-called data discs - prices are precisely contained in a zone, up the ceiling, down the ceiling, and always find a connection - there's probably an option-induced model of business behavior running behind them, but retail can't see the parameters of this model。

C. WHICH FIELDS SHOULD BE DISCLOSED IN THE CHAIN

If MM loan is recognized as the most important box variable attcoin, the next question is which fields to disclose。

Not all details must be made public. MM ' s quote algorithm, risk management parameters belong to his Alpha and the chain would destroy his business logic. What needs to be disclosed is the smallest collection that has a direct impact on retail price expectations and does not constitute MM algorithm IP: number and wallet address of loaned token, contract duration, stike price, unlocking and returning curves, profit-sharing mechanisms, warranty and default terms。

These six, taken together, are just enough to retial, using standard financial analysis methods, to extrapolate the rational reaction of MM between different price zones, turning the current black box into a modelable supply curve. MM's specific transactional behaviour (his alpha) does not have to be disclosed, but is the incentive parameters behind the behaviour。

Technical realization is not complex. A standardized schema, a token loan contract for mandatory writing of a register on the chain, an index service for analysts to read, can be completed with hundreds of lines of code on EVM. The real hard part is never technology, it's motivation -- how to get the projector and the MM to take to the disclosure. This is the question to be answered in the next section。

What happens to the ecology after disclosure

after disclosure really happened, there were a few direct changes in the altcoin market。

The pressure structure becomes readable. The number of traffic in the tokenomics files is separated for the first time from the MM loan, and retail can get "book traffic + MM loan = actual voltage". After disclosure, price fluctuations close to strike will become a new critical price in the attcoin technical analysis, a “institutional cost line” similar to the stock market, but more precisely because it is written in the contract. Complementing the Shortit class to make empty tools, retail can build symmetrical positions around strike for the first time。

Accountability becomes enforceable. One of the tokens dropped sharply today, and the projector could say "market behavior," MM could say "passive hedge." After disclosure, each MM wallet exits into an open contract, any dump can be attributed to a specific (project party, MM) combination, and reputational costs enter the MM decision function for the first time. The project party can no longer speak of “no team push” and “no top-level business cooperation” at the same time — after disclosure, the two sentences can only be divided。

The second-tier effect of greatest concern is the transparency premium. Once a portion of the project is voluntarily disclosed in the market, the non-disclosure is assumed to be the worst-case scenario (a bit similar to Proof of reserve) - retail would assume that its lending volume is large, striike is very low and its base is very high, and therefore the valuation is low. Disclosure thus moves from cost to signal, from self-help to a tool to obtain valuation premiums. This is the internal dynamic that any disclosure system can really run — not compliance pressure, but market pricing pressure。

Of course, all of this is about ideality, which is very difficult to do。

the altcoin market after the triad

Leverage, direction, information — the three layers of asymmetries referred to in the preceding three chapters — have been dealt with separately over a decade by three different agreements. Looking at these three democratizations together, a new set of market structures will emerge。

the deleveraging of leverage allows retial to zoom in on the bet when judging the right direction. the empty democratization has allowed retaill to bet when it's decided to fall. democratization of information allows retial to know for the first time what price and when to bet. it's only the first time that retaiil has a complete set of tools with an insituation at the same table。

Once the three tools were in place, the price discovery mechanism itself began to change。

the altcoin price discovery has long been dominated by two things: narrative (who tells stories that attract more attention) and liquidity (who uses more money to push prices to a certain location). Before the three democratizations, both were controlled by the project ' s three parties, the VC-MM. Retail's role has been that of recipient of narratives and provider of liquidity — the former deciding what he buys — and the latter deciding when he will be delivered。

After three layers of asymmetries were broken, the main axis of price discovery shifted from narrative + liquidity to information + expectations. Retail is no longer looking at KOL's flyers and K-lines, but also a readable MM contract disclosure, a transparent empty lending pool, and a modelable set of options. Narratives still exist, but narratives can no longer drive prices in isolation, and information will immediately re-pricing the excessive narrative。

It is important to note that the co-opted space between the projector and MM does not disappear. Smart players will still find a new way to play -- to split the option structure into a sub-chain agreement, to spread out the strike with a multi-leg derivative, to borrow directly with DAO governance tokens. Each evolution of the disclosure system creates new means of circumvention, which is the norm in any financial market。

But the marginal costs of complicity can be significantly raised. Today, one project partner and MM designed a contract "defunct to retial" at almost zero marginal cost because nobody saw it. After disclosure, any overly radical clause would be identified and priced by the market, and contract design itself would be an open game. The conspiracy will not disappear, but the rate of return on the conspiracy will be significantly lower。

The second-tier effect that deserves more attention is a shuffle by market participants。

The quoted MOVE is a specific sample, but similar projects have been the main addition to the atcoin market in the last three years - the core business logic is "low circulation + high FDV + strong market + narrative rush." Under disclosure, they are immediately priced back to the real supply curve and lose their existing economic base. The withdrawal of this category of token would significantly lower the overall valuation hub of atcoin。

Projects that have real needs, are willing to voluntarily disclose, and choose to walk along the MM will receive a valuation premium, a more stable retail hold and a longer market life cycle. There are very few projects in this category today, but the disclosure system would give them positive feedback on the secondary market and increase the number exponentially。

Emerging players. The MM protocol itself. When all the key parameters of an MM business have to be chained up, MM, the role will be partially agreed -- there is an algorithm that is driven entirely by smart contracts, and the projecter uses open schema configuration parameters, the contract is automatically implemented for listing and return, without the GSR, the Wintermute layer. MM operations move from "relationship-driven + information-poor" to "agreement-driven + standardization" and in the long run remodel the industrial structure of the atcoin market。