A cruel reflection from the Silver Trench: about leverage, game and human chains

Photo by Alexander Campbell

Original: Deep tide TechFlow

Introduction:After a historic fall in precious metals last Friday, Alexander Campbell, a former Bridgewater researcher, wrote this in-depth reflection。

Not only did the article disprove, from a financial engineering point of view, the mechanical principles that led to the collapse of the Silver 6-Sigma (six times the standard deviation) level – including the short Gamma effect, the leverage of ETF stomping and the price-fixing contest between Shanghai and New York markets – but it also rarely revealed the emotional struggle of a professional investor in the face of a conflict between fan responsibility and rational decision-making。

The text reads as follows:

Last Friday was a painful day。

That's my reflection。

In the second half of this article, we will follow the standard process of combing the historic event of Friday's lasagna: what do we think actually happened? Why? What has been the impact on the portfolio? And where we're going next。

But first, my reflection. If the content becomes a little... philosophical, please take it easy。

The sentence quoted at the beginning of this paper (relative: "Suffering + Reflection = Progress") is not just a motto for me, it is a way of life. This is one of the most profound lessons I have learned during my tenure in Bridgewater, and it is a way of putting all the pain into context。

On the road to the Goals, you will face challenges. There must be a retreat on the way to the financial targets。

I've been through worse in terms of retreats. Maybe not in a single day, but certainly in the whole life. Of course, the situation is likely to get worse, perhaps with the volatility of silver and gold being a “creas in a coal mine”, signalling a series of chain-reaction “liquid competitions” that push asset prices down and the demand for risk-averse assets (such as United States dollars, bonds and Swiss francs). There is a real possibility。

In the next few days, you'll see a lot of experts coming out of the woods and saying, "I told you so!" Selling one or another of these ideas and throwing a screenshot on your face. In a way, when the deal went the other way, I did the same thing, so I wasn't different。

But the reality is that no one knows the future. There are always unknown conditions, and the world is chaotic and dynamic. While this has made it possible to gain an advantage (Edge), even the best investors have a 55-60 per cent winner. Gödel's machine will never be really complete. That is why diversity is necessary, why it is necessary to fight, and why it is why you see that the best investors maintain a sense of humility almost at all times. Although sometimes the accompanying language of compliance makes it difficult to understand what they really mean。

Nevertheless, I think it is important to look at the moment when you make a mistake, to diagnose what happened and to try to learn — about the world and about yourself. It's hard to reflect when you get 130% more in a year. But when you have an expected annual volatility of 40 percent of the books lost 10 percent in a day, reflection is a requirement。

Thursday night through Friday afternoon, I've been thinking a lot. Later, we will discuss the rational process of trying to track the evolution of the world, collide stories, analyse causes and respond. But before that, I want to talk about the emotional side。

All professional investors, or at least those taking real risks in open markets, will understand what I mean by “investment is often emotional”. There are two demons in your mind: greed, which tells you to keep pressurizing, and to take further advantage of your excess earnings, Alpha. It fights with fear, which knows that “I may have been wrong, and many things I do not know.”。

I am particularly interested in a new feeling of responsibility that has evolved from Thursday night to Friday。

You see, a lot of people who are reading this blog are new. The eyeball always chases the returns, and the fluctuations in prices ranging from $60 to $120 attract a lot of attention to these pages, and they fill my inbox with information. I was thanked, and I was asked for views. In my area of comment, there seems to be an inexhaustible number of people asking me for updates every minute, support places, etc. This process may be familiar to well-known public figures, but it is relatively new to me。

If you look at my Twitter/X, you know I'm trying to use an Irreverent. This is the style that I learned from the Oxford Union debate -- between Insoucient and Insight. It's not just an act, it's a world view: I usually strongly believe that I'm right, and I know that I'm often full of shit, and that these views are rapidly evolving in the face of new information. I think this perspective goes hand in hand with many professional “Shitposters”。

When you become "micro-viral," what has changed is that even if you try to keep that cynical tone to convey the message, the distribution of people who actually listen is getting bigger. From your friends, colleagues and Internet fans, you have become the countless strangers who read your articles, read you, interact with you. In addition to knowing that as the spread becomes wider, your informational context may be diluted (like an Internet speaker game), there is a time lag (Lag) problem。

I started writing a silver/solar relationship in 2023. About 18 months ago, I started "knocking the table" recommending. My portfolio was 100% done more. With the price rising, from $25 to $40, then $60 and $80. I slowly reduced this risk exposure from “more irresponsible” to “more dangerous” to “more still”. Sell a little, or let the options roll and try to lock profits while keeping them open. The problem is that as the silver rises, it becomes more volatile. So I'm still doing well. In response, the opponents would say that this is a red flag signal, and that is true (we will discuss it later in the section on signs), but the point is that you end up in such an awkward position: Although a lot of people are in the car for $25 or $40, you realize that, because of the time lag in writing articles and reading information, the eyeball weighted average purchase price could be as high as $90。

That puts you in an interesting position. You'll feel guilty, as I have felt at some point in the past week or so, if you “run the road” simply because it's cold in the back. You think you owe the people who like your work, you should stick to the deal and put yourself in their position。

This is completely stupid from the point of view of financial management. You can tell yourself that if you were managing other people's money, you would have cut off all your positions on Friday morning when the Chinese market opened without saving the market and sold gold on a large scale. You can rationally say that I wouldn't hold so many positions on copper if I managed other people's money. I'll remove the risk on Friday morning when it rises by 10%. Ultimately, however, the books are the books。

Let's say one more thing before we get into your most important part。

Some of you subscribe because you like what I think of silver and markets. Some of them are because they like my gossip。

Looking ahead, I am considering separating them. Punctuation — about philosophy, worldviews, thinking about processes — will remain free of charge. If I start publishing specific, actionable trading ideas and providing real-time updates, this could turn into a fee-paying item. It will create a real sense of responsibility on my side and create real value on your side。

Now, just know that not every post is about the stone. Some of you will not like this. It's okay。

Considering all this. What happened

How historic is this

Before going into the article-by-article analysis, let us put last Friday in the background. Because I don't think people are aware of how rare this is。

That's silver for 275 years of daily rate of return. Last Friday ' s fluctuations were one of the largest single-day drops in the metal ' s history. We're talking about the end of the dollar-based silver fixation, the collapse of the Hunt Brothers and the volatility of March 2020 -- this is just a normal Friday in January, with no warning。

Pre-Friday Volsurface price shows that changes in 3-Sigma (triple standard deviation) are considered as tail events. And what we got is about6-SigmaI don't know. This should not have happened according to historical distribution, but it happens when the positions of all people are consistent and mobility disappears。

Specific details

If you follow this story from a narrative perspective, even before Friday, the past few months have been a crazy journey. The silver was at a high level of over $40 when it opened in November, rebounding 74 per cent by the end of the year to about $85, and then reverting to 15 per cent by the end of the year. As we mentioned in a previous article, many of them subsequently defended the trend, opening another wave of monsters at 65% rebounding and reaching a peak of about $117 on Monday, followed by Western sellers entering the market and dropping prices again by 15%。

Gold mirrors these trends to a large extent, and the trend “New York sells, Shanghai buys, metals flow east” looks intact。

Even until Thursday morning, the news was occupied by a 10 per cent increase in copper prices overnight. (This is another warning signal that things are getting a little harder to control, and we will discuss it in a subsequent article on red metals)。

I felt this severe concussion, and I reduced the slot and released this tweet. That's more of a message to myself. Thirty per cent of that figure has been hanging deep in my head, and has been marginalized as a voice of fear rather than reason。

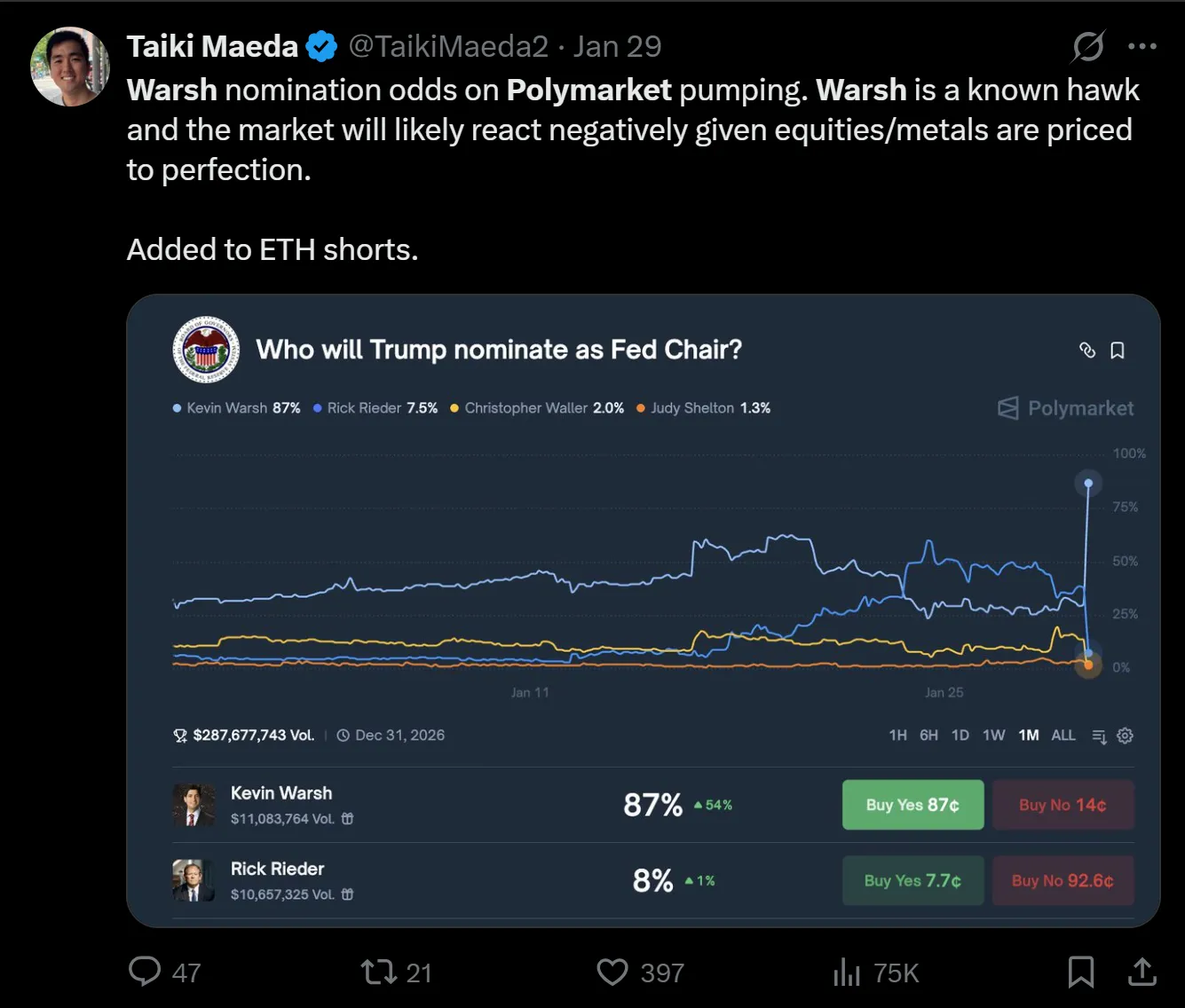

Later Thursday, Kevin Warsh appeared and his confirmation/dissemination on Pollymarket will be nominated as the Fed Chairman。

Warsh is seen as a sort of “hard money” advocate, and I am very good at it. You see, I saw him at Stanford ten years ago briefly. At that time (approximately 2011-2015), he was famous for calling for the return to normality of the Fed ' s massive quantitative easing (QE) policy following the financial crisis. At that time, he seemed more like a statesman than an economist, and I always felt that his hawk stance was one way to be famous in the sea of the loose money advocates. After all, when you're not on the driver's seat, it's easy to appeal for interest rates and abbreviations。

So, although I have a lot of risk exposures in bulk commodities (in fact, copper and gold are more expensive than silver), I thought I'd only get a little bit hurt and wait for the Chinese market to open. Reminding me that, as I have been publishing for months, it seems to me that Western metal investors do not realize that today “you are the tail, the dog is in Shanghai”. They underestimated:

(a) the actual demand for these metals is concentrated in the east:

(b) how much of the total proceeds from these metals came from the “overnight” market (measured by the proceeds from yesterday's closing to today's opening):

(c) how much money does china actually have compared to the west:

Yes, there is much on the Internet about how much of the “China premium” is caused by confusion over the value added tax (VAT) levied on retail physical delivery. There is a lot of difficulty and confusion in the macro field, so people on the Internet don’t press their calculators, but rather shake their charts, ignoring it, and using it as a weapon to spread suspicion in the “China is pushing up prices.” In my view, this is a typical case of “change, not level”, because it is clear that (a) this premium (or discount) has recently increased, and (b) this has also happened in India。

But I can feel that empty narratives are gaining momentum. Even when supported by demand, for example, there is an disproportionate premium for the only purely offshore silver fund。

Moreover, there is indeed some evidence that the pressure on physical purchases has eased, most directly at the “front end” of the London silver curve. Over the past month, it has seen a significant decline in the level of “off-the-shelf water”。

I cut my Delta to almost even before nightfall, but I thought, "Wait till China opens up." This may be my biggest mistake。

Instead of counterattacking, China was sold. It's not just silverGold's down, 8%I don't know. This is Strike one. I didn't know, but the local Chinese silver ETF actually stopped。

This means that the Chinese diaspora did not save the city。

THIS WAS SUPPOSED TO BE A SIGNAL OF RETREAT. I CHECKED THE BOOKS, DREW UP A LIST OF POSITIONS AND WAS SATISFIED WITH MYSELF, BECAUSE MOST OF MY OPENINGS WERE INTENDED TO EXIST IN THE FORM OF POWER, SO IF I DID DO IT COMPLETELY, I WOULD FEEL PAIN, BUT IT WOULD NOT BLOW UP. THIS IS THE SECOND HAMMER. NOT JUST BECAUSE I WAS SUPPOSED TO SELL THE FUTURES DIRECTLY (WHEN GLD AND SLV WERE STILL OPEN, AND I HAD AN AVERSION TO FUTURES, BECAUSE THERE WERE A FEW PAINFUL TIMES IN THE PAST FEW YEARS WHEN THERE WAS NO FULL-TIME DEAL THAT I FORGOT TO SHOW UP), BUT BECAUSE I WAS SUPPOSED TO MAKE A PROMISE TO CUT IMMEDIATELY WHEN THE MARKET OPENED. YES, I WAS FULL OF MEETINGS THAT DAY, WHICH MADE IT IMPRACTICAL TO FLATTEN A GROUP OF 20 OPTIONS POSITIONS, BUT I DIDN'T WANT TO SNEAK AWAY LIKE A DOG THAT RAN AWAY IN THE NIGHT, BECAUSE THERE WERE SO MANY PEOPLE IN THE CAR. THIS IS THE THIRD HAMMER, PROBABLY MY WORST DECISION。

You probably know the next story. The United States had a big fall, and then it went down. The sale was ruthless, and it was too late when I realized what had happened. Because as the day went on, my fourth hammer immediately appeared。

We're in a short Gamma market。

That's what it feels like to be in the air

Short Volt is not just a mysterious state, it actually represents a mechanical process, and market changes are exacerbated by machine-like market behaviour。

The most obvious example was in 1987, when portfolio protection kept the market at a short volatility rate (or “short Gamma” in the term options), as the insurance scheme was forced to sell more and more futures as “ spot” prices deteriorated。

IN RETROSPECT, IT'S CRAZY THAT I'M ACTUALLY FAMILIAR WITH THIS DYNAMIC, BECAUSE IN OCTOBER, I SUFFERED WHEN GLD AND SLV BROKE THE BOTTOM OF MY OPTIONS。

Simply put, this is the mechanism: I'm going to buy Call Options. Usually people who sell you options need to hedge. They're not in the direction of gambling, but they're betting that you're paying more rights than they're expected to do through Delta. They sell options and buy stocks as a hedge. If the price rises and the right price breaks, the option Delta increases, and they have to buy more stocks. Conversely, Delta falls if prices fall below the right price. Now they have a lot of stocks in their hands, so they have to sell them to a market that is falling。

Such behaviour is almost mechanical and can normally be observed from the downward trend in asset prices, which does not seem to be at the bottom. Markets are often particularly vulnerable to short-gamma impacts when approaching monthly or quarterly maturity. If you look at the history of these crashes, I bet most of them happen near or near these maturity dates。

This occurs in the market for options and is achieved through leverage. When investors are leveraged to purchase assets, collateral is usually required to conduct transactions. When prices fall, the exchange or its market chamber demands that they " provide collateral", i.e., more cash. When there is too much leverage in the market, they usually have to sell certain assets to cash the cash. In essence, it keeps them in a state of empty volatility。

The third way to keep this market at a “short volatility” is a little surprising to me. I didn't realize that the "double leverage" silver fund AGQ had accumulated $5 billion in assets. This means that it holds $10 billion in silver. The fund is “rebalancing” every day, so when people wake up with a 15 per cent drop in silver, the fund actually loses 20 per cent * $10 billion, or $2 billion. This leaves $3 billion in the value of the fund before the redemption. That means their new Delta is $6 billion and they have to sell $4 billion in silver

The previous options expert, Kris, outlined the dynamics here:

A friend of mine, Andy Constan, reminded me of this dynamic and told me that the time of "rolling" was 1:30 p.m。

Just a few minutes ago, after I waited for some test-based signals, I bought SLV at a 71 dollar price and doubled the position by buying shares, buying options and selling the price differentials of the lower right. Even if I didn't win my own job, I'd have to profit by using Alpha in market relations。

In fact, I have a fourth approach at a “short swing”. Because I tend to buy a price differential between Call Spreads and Flys, I've been “renewing” my options as the market rights are getting higher. It left me with a false sense of security. By the end of the day, I lost 2% on silver and 2% on gold. Counting the losses of copper and other positions, we fell 8% all day, with wounds but not fallen. This translates our gains from the beginning of the year to the present (YTD) to 12.6 per cent, with a cumulative gain of 165 per cent since January of the 25th year。

Well, if you're still reading, we now have an answer to why the silver was destroyed, and we have a mechanism — short fluctuations — through three channels: over-leveraging, empty front-runner Gamma, leverage ETF。

But where are we going next

War fog

First, we need to remove the fog of war. Given that the Chinese market was closed before the worst movement in the United States, the current simple estimate of the “China premium” is completely disconnected。

THE SAME APPLIES TO THE STATEMENT THAT “THE SLV TRANSACTION PRICE IS BELOW THE NET ASSET VALUE (NAV)”。

THIS SEEMS TO BE MORE BECAUSE SLV USES THE LONDON SETTLEMENT PRICE TO CALCULATE ITS NAV (AND WHEN THE WORST HAPPENS, LONDON IS CLOSED). IN TERMS OF THE DAY PRICE ON FRIDAY, THE ETF LOOKS VERY CONSISTENT WITH THE FUTURE PRICE。

Now, apart from the possible Monday rebound, the real question is, "How does China start Sunday night?" If you believe the rumors on the Internet, the price of goods in the East is still at $136, which means that we may see an increase of +5-10% on Monday。

My fiancée is currently travelling on foot, and she says that jewellers in the west still sell 925 silver (92 per cent purity) at $1.90 per gram (or about $64 per ounce). So the basic situation still seems to be that silver is cheap in the West and expensive in China。

Whether this leads to higher prices will depend on local conditions. As Merridew has pointed out, it is highly probable that Chinese leverage investors will be forced to liquidate at the opening of an opening on Sunday night/Monday morning。

PLUS THE CME BOND WAS RAISED AGAIN ON FRIDAY, BUT REMEMBER THAT BECAUSE OF THE PRICE DECREASE OF ABOUT 30 PER CENT, EVEN A HIGHER DEPOSIT WOULD MEAN THAT THE AMOUNT OF NET CASH WITHDRAWAL COULD BE NEGLIGIBLE. THE BOND PER UNIT OF SILVER HAS INCREASED CONSIDERABLY, BUT THE TOTAL AMOUNT OF THE FUTURES BOND IS APPROXIMATELY THE SAME。

Source:@profitsplusid

BITCOIN'S PRICING IS NOT RISING HERE, AND APPEARS TO BE THE RESULT OF FORCED SALES, CONTINUING CONCERNS ABOUT QUANTUM CALCULATIONS AND A POSSIBLE COMBINATION OF EXPECTED MSTR PROBLEMS。

Based on an analysis of the peculiarity of its business model 14 months ago, we still have an empty position。

What's the reason for the rise

First, the SLV stock price had begun to decline before Friday. As prices fall, this means that nominal exposure has declined significantly。

Unless there is some sort of extreme deleveraging in the Chinese market on Sunday night, the AGQ (twice silver ETF) dump has become the past. Any significant rebound or upturn would be counterproductive — as in the case of Short Call Option, forcing those people to fill in additional shares when prices rise. As for me, I bet the Chinese market won't fall all the way down. And if we really see some kind of compulsory liquidation, the stock market will probably not be spared。

The last point worth noting — the geopolitical context has not become more calm. If anything, signals from Tehran suggest that we are not much closer to some kind of confrontation. Historically, precious metals have performed well in this environment, even if the road to success becomes extremely confusing. Given all these potential deleveraging forces, you should view the current position as extremely tactical. I reserve the right to shift the entire commodity curve to a completely flat or negative Delta, depending on the circumstances。

I may have overloaded my empty positions, but I am increasingly concerned about a substantial retreat in the stock market, as people begin pricing the “air Gap” between the cash flow required to invest in data centres and the actual revenues of these companies. Yes, the AI Ages is coming, and yes, the Moltbook is really interesting (which, if properly operated, consumes a lot of tokens/Tokens), but the deployment of AI in an enterprise still faces enormous logistical, compliance and operational barriers. What you saw on Twitter/X about the workstream revolution came mostly from independent hackers, creators or small companies with flexible and easy business processes. My estimate remains that the smarts started to line up at the end of the second quarter, before they had income. This makes the US stock highly vulnerable to the dynamic effects of the Microsoft crash last week。

So, in relative terms, I'm still looking at metals. But I would like to admit that I may be wrong and seek a more timely response to market conditions。

All of this began with the motto of pain and reflection. Friday brought a lot of pain, and this article is an attempt of reflection. The core logic (Thesis) has not changed — light demand, capital flight from China, supply restrictions. What changed was prices and positions, and I realized that in a market where it felt like it would only go up, there were so many short Gamma risks。

Pain + Reflection = Progress. Let's see what this progress will take when the Chinese market opens on Sunday night. Good luck with the deal and be safe. See you next time。