In-depth study of the chain lending market: liquidation of credit under the chain

I. Definition evolution: from encryption levers to mainstream financial infrastructure

Lending on the chain is not new。The introduction of a mobile mining mechanism in Compund in 2020, which pushed DeFi from a polar circle to a public view, opened the door to DeFi's summer. At the same time, the chain-based lending is essentially a high-leveraging tool for encryption — a user over-collateralized encrypted asset that captures liquidity, then markets liquidity into a gain aggregater or liquidity, pursuing several times the annual gains of traditional finance. This model works well in the cattle market environment, but the chain effects of the 2022 Terra/Luna crash and FTX bankruptcy exposed the vulnerability of super-high mortgage rates and chain clearing. After two years of shuffles, the chain made a critical transition from "leveraging tools" to "configuring infrastructure". The driving force of this transition is threefold: first, the improvement of the regulatory environment — the emergence of the MiCA framework in the European Union, the gradual endorsement of the ETF by the SEC, which has partially removed the barriers to compliance in the chain of traditional finance; second, the uplink wave of RWA assets — real assets such as United States Treasury bonds, monetized corporate bonds, real estate gains rights, which have begun to become central collateral for chain lending, changing the asset structure and user image of chain lending; and third, the exploration of interest rate marketization — From the initial pure floating interest rate to fixed interest rate agreements (e.g. Notional, Yield Protocol) to the hybrid interest rate system (Pendle), the chain-based interest rate pricing mechanism has grown more mature and has begun to be aligned with traditional financial markets。

As atAt the beginning of 2026, the classification of assets in the chain lending market has developed a clear three-tiered structure: The bottom tier is fixed-currency borrowing, represented by USDC, DAI, USDT, which is the largest market area and the most manageable area, typically with 80-90 per cent LTV; the middle tier, with volatile asset lending as collateral for mainstream encrypted assets such as ETH, BTC, which is usually controlled at 50-70 per cent to address the liquidity risks associated with volatile prices; and the top tier, RWA asset mortgage lending, which includes monetization (OUSG in Ondo Finance), corporate credit (private borrowing in Maple Finance), real estate gains, which is becoming a new growth engine for chain lending, particularly by institutional investors seeking compliance entry points. In terms of geographical distribution, the user structure of chain lending is undergoing profound changes: Asian markets are dominated by individual investors and arbitrators, favouring high leverage and complex strategies, while European and American markets are showing a clear trend towards institutionalization, with greater requirements for compliance hosting, KYC certification and audit transparency. This fragmentation of user structures has a direct impact on the functional design priorities of agreements in different regions。

II. COMPETITION STRUCTURE: A BETWEEN STRENGTHEN AND TECHNOLOGY

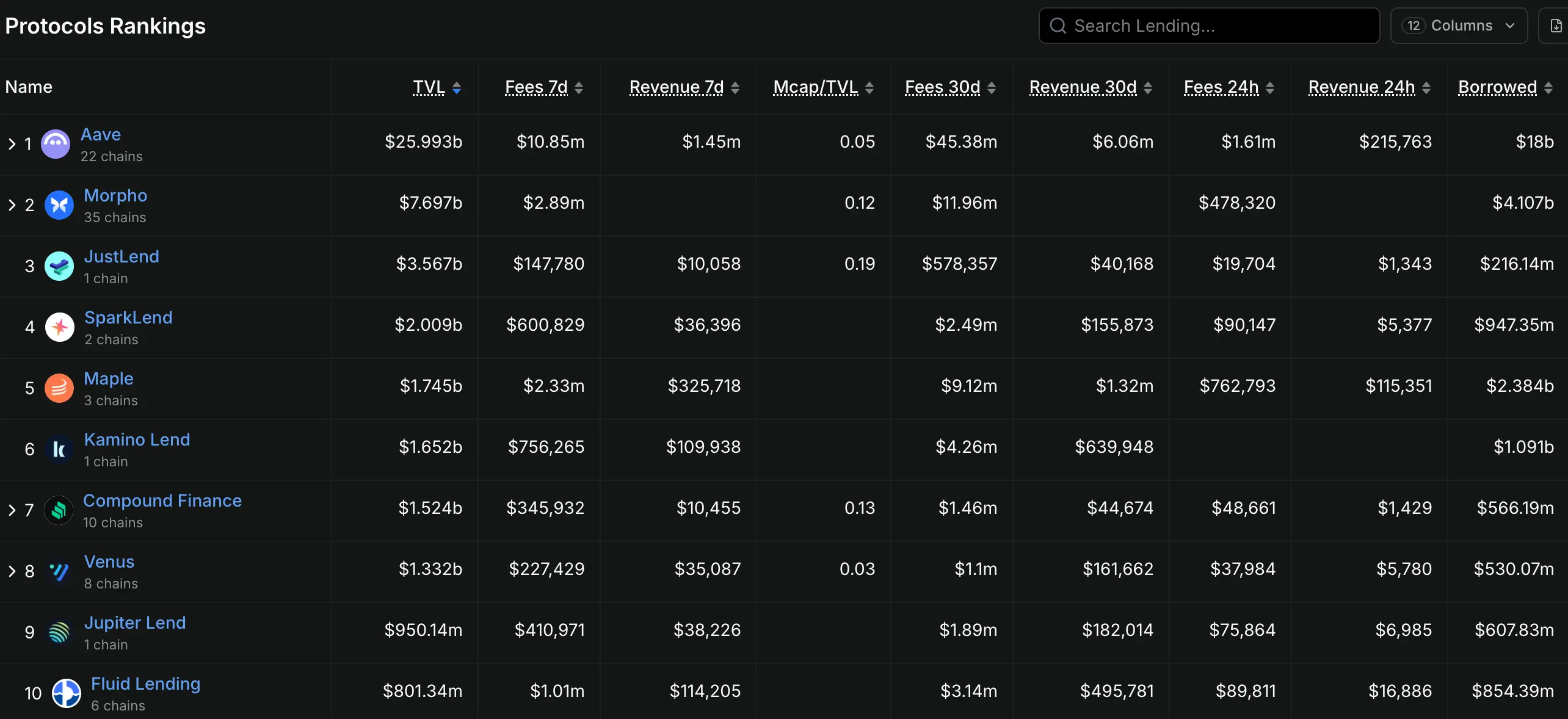

The competitive pattern of chain lending markets is typical"A super strong" feature. Aave is absolutely dominant with about $32.9 billion in TVL, more than ten times ahead of the second-name Compund (about $2.6 billion), and more than 50 per cent of the total TVL in the lending track. However, Aave's moat does not come from network effects or brand recognition -- I don't know. These are of little value in the Open Source Agreement world — but rather in its continuing technological and ecological expansion capacity. From the floating interest rate model of Aave V1, to the credit commissions and lightning loans introduced in V2, to the Portal cross-chain mobility and isolation model of V3, each generation of Aave's products is precisely hitting the market. The V4 version is expected to be online by mid-2026 to further strengthen the cross-chain liquidation capacity and institutional compliance framework. In the shadow of Aave, a number of differential agreements are searching for their own space. Morpho Labs followed a unique evolutionary path — initially as an optimisation layer for AAVE and Compund (upgrading capital efficiency through P2P matching) and then gradually developed independent Morpho Blue (no prophecies, no governance lending) and Morpho Vaults (revenue strategy managed by professional risk planners) from "optimal" to "independent agreements". Spark Finance, on the basis of the DSR (DAI savings rate) ecology of MakerDAO, has established a solid user base in the area of stable currency lending, which, in conjunction with the technology of Aave V3, makes it an important gateway to institutional entry。

In terms of technical routes, the chain-based lending agreements are divided along three paths. Number one:The "Consolidated Liquidity" route (P2Pool), with representational agreements including Aave, Compund and Kamino Finance, is based on the idea of pooling credit funds into shared pools to achieve efficient allocation of funds through algorithms that adjust interest rates to the utilization rate dynamic. This route has the advantage of being sufficiently mobile, having a simple user experience, and the disadvantage of being less capital efficient (the lender cannot directly negotiate terms with the borrower). The second is the "point-to-point match" route (P2P), which represents a number of agreements, including Notional Finance and Myso Finance, the core idea of which is to provide lenders and borrowers with a direct match to achieve a fixed-term, fixed-interest-rate lending experience. This route has advantages in terms of interest rate stability, but is relatively insufficiently liquid and suitable for borrowers with a clear plan for the use of funds. The third is the "Permissions Pools" route, which includes the Euler Finance (V2 version) and Ajna Finance, the core concept of which is to give the agreement full risk management authority to the market-- - Unpredictable feeding, unsanctioned voting, borrowers and lenders setting their own parameters and risk taking their own risk. While this route is more decentrized, it also faces higher user education costs and potential smart contract risks。

Core risks: liquidation, credit and cross-chain triple dilemma

Risk maps for chain lending are much more complex than traditional finance. Unlike the banking system, there is no deposit insurance in the chain agreements, no central bank lender of last resort, no supervisory window guidance— When the crisis comes, the clearing mechanism becomes the only price discovery mechanism, and this “inexhaustible mechanization” tends to magnify the fall in market panic. Clearing waterfalls are the most typical systemic risk of chain lending. On Thursday, 12 March 2020, the "Black Thursday", a single-day drop of 37 per cent in the fare price, the launch of a large-scale liquidation by MakerDAO, an extreme phenomenon of zero-price deals in liquidation auctions due to insufficient liquidity, and the actual liquidation of ETH collateral is only 50-60 per cent of the market price. A similar incident took place again during the collapse of the UST/LUNA in May 2022, when a number of highly leveraged positions in Aave and Compund were forcibly liquidated, further exacerbating market outages. To address the risks of liquidating waterfalls, the agreements adopted different strategies: Aave V3 introduced the "Efficacy Mode" to allow borrowers to optimize the efficiency of collateral against specific assets; the Isolation Mode placed high-risk assets in a stand-alone pool to prevent the risk of a single asset from spilling over to the agreement as a whole; and Ajna Finance completely abandoned the predictor, using the automatic pricing of the supply-and-demand relationship between collateral and debt, and left full responsibility for price discovery to the market。

Credit default risk is the second most difficult task of chain lending. With extra collateralThe "mechanical execution" model is different, and credit lending on the chain without collateral or under-collateralization is naturally facing assessment challenges. Goldfinch and Maple Finance have adopted a hybrid model of KYC certification and settlement on the chain by scoring for borrowers through real-world credit assessment institutions (e.g. Blackstone Credit Partners, Van Eck, etc.), but there is a fundamental contradiction between this "centreized endorsement" and DeFi's unlicensed spirit. In November 2022, encryption trading agency Orthogonal Trading declared default and left some $36 million in bad debt on the Maple Finance platform, an event that exposed the vulnerability of chain credit lending - I don't know. When the borrower is an institution rather than an individual, his or her asset allocation and risk management capacity are uneven and the reliability of "credit assessment" is questionable. The deeper paradox is that chain credit lending tries to replicate traditional financial credit evaluation systems in a decentrized world, but the road faces an inherent tension between regulatory compliance (GDPR, KYC/AML) and chain anonymity. Effective credit assessment mechanisms, while protecting the privacy of users, will be at the core of the long-term development of chain credit lending。

Cross-chain security is the third most difficult task。Aave's Portal function, Morpho's cross-chain deployment, and Ajna's multi-chain expansion — the cross-chain layout of the head agreement is moving the chain-lending boundary from a single chain to a multi-chain ecology. However, the complexity of cross-chain expansion has multiplied security risks. The Ronin Bridge attack in 2022 (loss of $625 million) and the Harmony Horizon Bridge attack (loss of $100 million) revealed how the security hazard along the bridge was transmitted to the DeFi ecology. When Aave ' s V3 agreement introduced assets along the BNB Chain, Avalanche, Arbitrum and others into their lending pool, those assets actually needed to be trans-chained through the bridge, which was often less secure than the chain itself. Even more problematic is the dependence of price prognosis on cross-chain assets - when the prophecies of a chain are abnormal or delayed, the position of the chain as collateral for the asset may be at risk of not being liquidated in a timely manner. This "bunk effect" means that the overall security of chain lending agreements depends on the weakest link in all the chains it extends. For investors, a focus on cross-chain expansion strategies and bridge security is a key dimension in assessing the long-term risks of the agreement。

IV. Innovative trends: fixed interest ratesRWA AND THE INSTITUTIONAL WAVE

Despite the risks, the innovative engine of chain lending has never stopped。Between 2024 and 2026, three forces are reshaping the rules of the track. The first force is a breakthrough in borrowing at fixed interest rates. The traditional P2Pool model is essentially floating interest rates — rates adjusted to the dynamics of the utilization of the pool, and borrowers may be under pressure to increase interest costs when market interest rates rise rapidly. This uncertainty is unacceptable for enterprises and institutions seeking to stabilize financing costs. Notional Finance pioneered a fixed-term, fixed-interest-rate lending product that allowed borrowers to lock interest rates for the next 12 months or even longer when they created the loan, and the lender to match the term by purchasing a supporting income certificate (fCash). Pendle Finance, on the other hand, coins the right of return — the future proceeds of the asset are split into principal gold coins (PTs) and proceeds tokens (YTs) so that the lender can lock in definitive gains through the purchase of PTs, while transferring the risk of interest rate fluctuations to the willing YT holders. Together, the two routes contribute to the process of market-based pricing of interest rates in the chain。

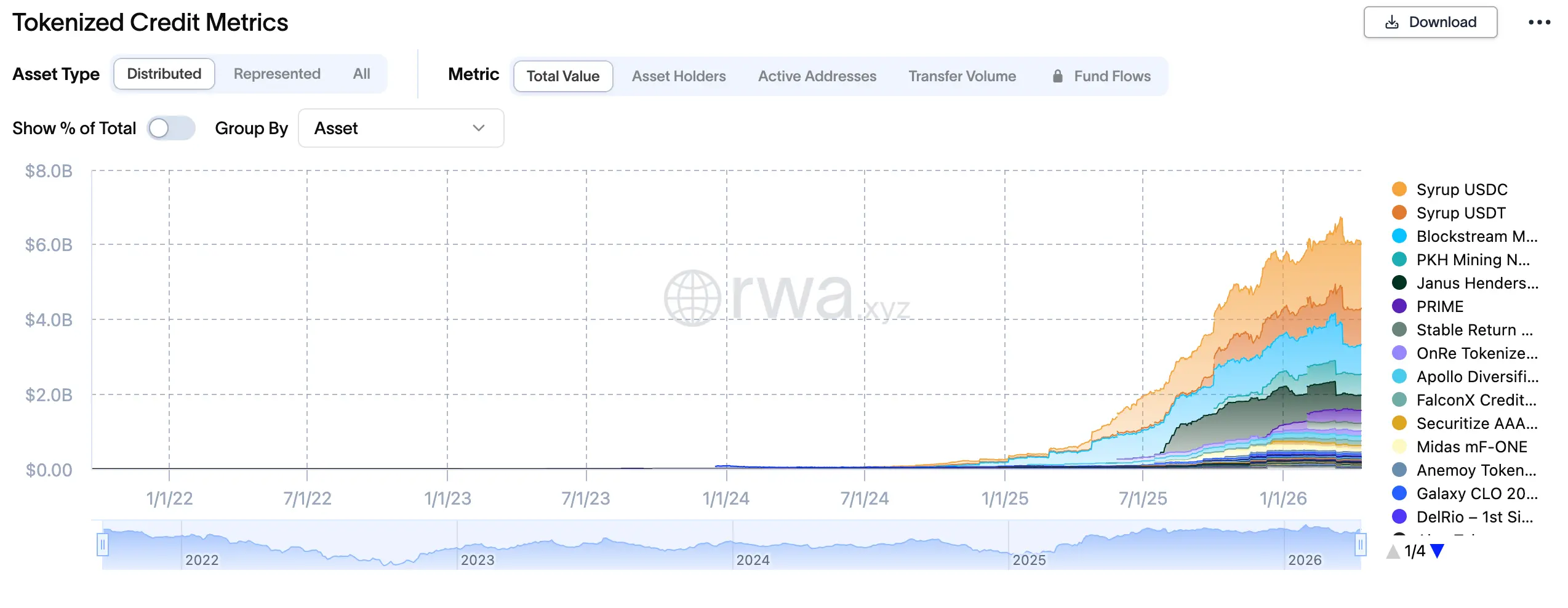

The second force is..RWA lending surged. In early 2024, BlackRock's monetization fund, BuIDL, was over $5 billion in size, and Ondo Finance's OUSG (United States debt gains currency) was over $1 billion in size — and these compliance assets began to be introduced into chain lending agreements as core collateral. The triple advantage of low volatility, liquidity and regulatory compliance compared to the volatility of encrypted assets such as ETH and BTC has become the "green channel" through which institutional funds enter the chain to borrow. Agreements such as Maple Finance, Pendle and Flux Finance have supported the use of dollar-based debt as collateral for borrowing, and users can access liquidity in United States debt positions while retaining the proceeds of United States debt. In the V4 version, Aave specifically designed the "Institutional Market" for RWA assets to provide chain lending services for compliant borrowers registered under the SEC framework. By early 2026, RWA lending in the chain had exceeded $18.5 billion and was expected to exceed $50 billion by 2027。

The third force is the acceleration of the wave of institutionalization. andDeFi ' s preferred anonymous, unlicensed, complex strategies differ, and institutional funding requirements are compliance, auditability, and risk control. The RWA lending platforms, such as Centrifuge, RWA.xyz and others, have designed product frameworks specifically to meet institutional needs: KYC/AML certification, sub-chain credit assessment, hosting bank liquidation, regulatory reporting - these traditional financial infrastructures are being "transferred" to the chain. More profoundly, institutional entry is changing the gaming pattern of chain lending. Traditional DeFi players are used to using leverage, lightning and arbitrage strategies to extract agreement value, while institutional funds tend to be more "held-loan-held-repossession" conservative. This difference in strategy will lead to a fundamental change in the financial structure and interest-rate curve of the lending agreement — more long-term lock-in, more stable interest rates, lower speculative liquidation. For agreements, how to serve good institutional users without loss of dispersed mobility is a challenge that requires long-term balance。

Participation strategies: three value trails and risk tips

For investors and practitioners interested in the chain of lending tracks, the current market provides three clear lines of value participation. The first clue is..Aave ecological extension investment. In addition to the direct possession of AAVE tokens, attention to Morpho Labs (as an independent agreement at the Aave Optimum level, its Morpho Blue is setting up a new paradigm of unpredictable borrowing), Spark Finance (stable currency-lending agreement with MakerDAO, which benefits from the DSR ' s ecological expansion) and the new functions (e.g., institutional markets, cross-chain liquidation) associated with the upgrading of Aave V4 are options for more risk-adjusted returns. Historical data show that AAVE tokens tend to yield significant excess returns whenever Aave issues a major version of the upgrade or when TVL is record high。

The second clue is..RWA Loan Track Beta opportunity. Ondo Finance (OUSG), Maple Finance (institutional credit) and Centrifuge (in-kind asset financing) are three different routes into RWA. Ondo ' s advantage lies in the deep integration with the Belet Buidl Fund and a stable source of return from compliance with the United States debt; Maple ' s advantage in having a credit file established by its real institutional borrowers (Coinbase Ventures, Framework Ventures, etc.); and Centrifuge ' s advantage in the real demand for its physical asset financing and a lower default rate. For investors seeking access to the RWA track, a decentralized deployment strategy is recommended to avoid the risk of a single agreement for a black swan。

The third thread is the structural opportunity for a fixed interest rate innovation agreement。Pendle Finance and Notional Finance represent two different fixed interest rate paths: Pendle achieves "resilient separation" through right-of-receiving monetization, which is suitable for high-level users who understand the logic of DeFi Lago; Notional achieves "interest rate lock" through traditional fixed-term loans, which are better suited for institutional users seeking stability. It is a matter of concern that Pendle ' s TVL grew tenfold in 2024, from less than $100 million to more than $1 billion, and that its high volatility of YT coins provides space for arbitrage and speculative tactics。

While pursuing opportunities, three types of risk need to be focused. The first is smart contract risk– The size of the TVL of the loan agreement has made it a high-value target for hacker attacks, and the US$ 197 million loss from the 2023 attack on Euler Finance warns us that even the head agreement may have undetected contractual loopholes. Second is the liquidity concentration risk - when a collateral (e.g. stETH, Lido pledge ETH) is overrepresented in an agreement, the extreme volatility of the collateral may trigger systematic liquidation. Third is the regulatory policy risk - the "unlicensed lending" function of a chain-based lending agreement may be identified by regulators as the issue of unregistered securities or illegal financing, especially under the MiCA framework in the United States and the EU, where compliance costs will increase significantly. For the allocation ratio, it is proposed to limit the chain lending exposure to 20-30 per cent of the overall DeFi configuration and to prioritize mature agreements that are subject to multiple audits, robust TVL, and transparent team background。

VI. CONCLUDING REMARKS: INFRASTRUCTURE VALUE AND INVESTMENTS Bell

The chain loan isDeFi is the closest track to the definition of "infrastructure". It does not seek the ultimate leverage multiples of a lasting contract, it does not rely on the false prosperity of a denominated incentive like a liquid mine, and it does not face a cyclical zero asset loss like the NFT market. Its value is rooted in real financing needs, steady interest income and building institutional trust. Behind 64.3 billion dollars in TVL are countless acts of financing, deposit and risk management by individuals and institutions, and the scale effect of this "grain finance" is the simplest and strongest value proposition of DeFi. Looking ahead, the investment clock on the chain is moving from "conceptual validation" to "institutional acceptance". The influx of RWA assets, the creation of institutional markets and the improvement of the compliance framework have been driving this track away from encrypted First Nations playgrounds to the extension of traditional finance. In this transition, striking the balance between "DeFi original innovation" and "institutional compliance needs" will be key to determining the ups and downs of agreements. For long-term investors, the chain-based lending track deserves a strategic configuration, the core warehouse should focus on the core ecological assets of Aave, and the satellite warehouse could be moderately involved in the alpha opportunities of RWA and fixed-rate innovation, while maintaining a culture of fear of smart contract risks and warehouse management discipline。