Hong Kong stabilization coin "gunfire": from cards to ecology, the real long run is just beginning

Contribution: Farmers Frank

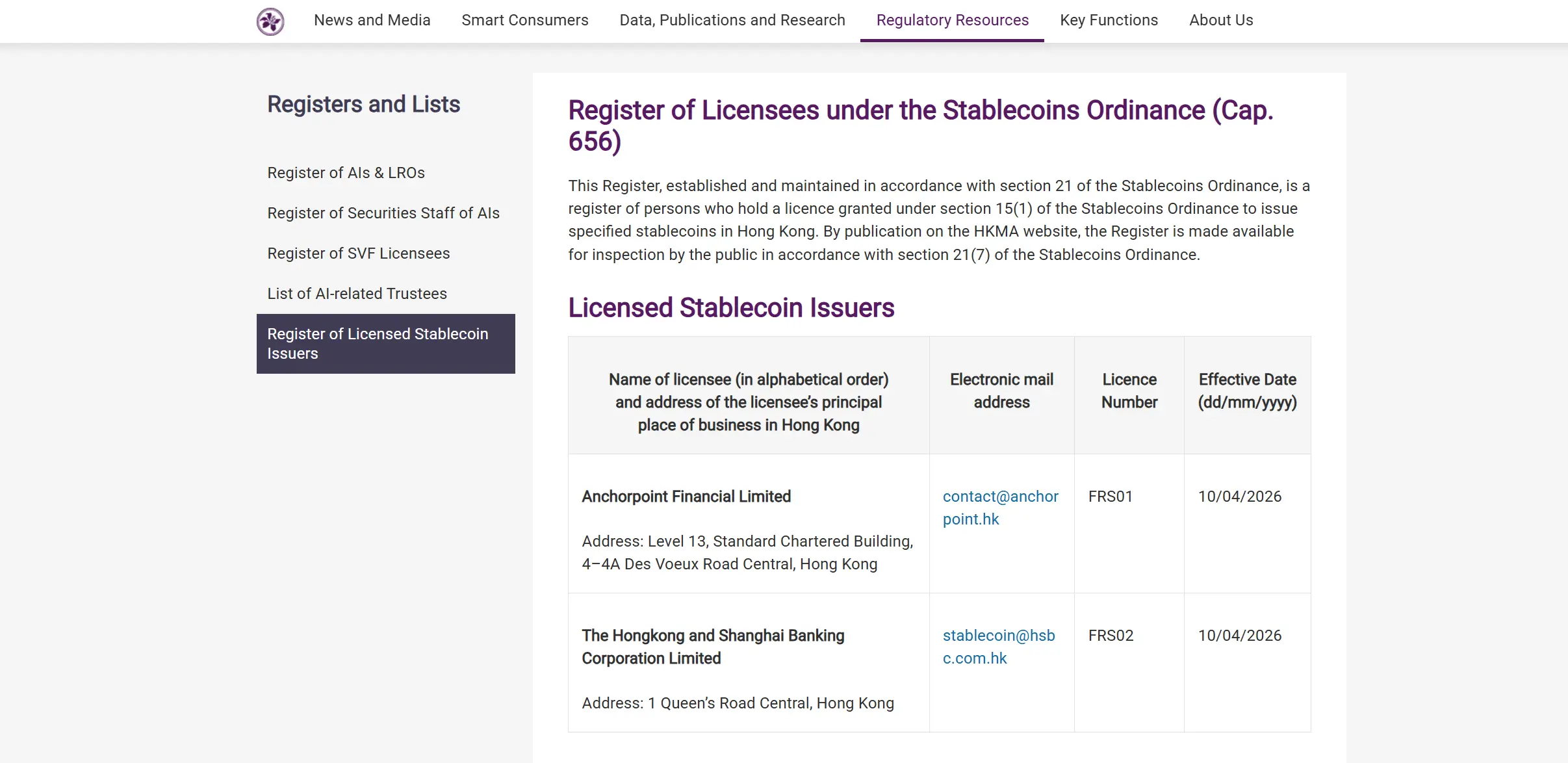

On 10 April 2026, the Hong Kong Monetary Authority officially awarded the first issuer of a stabilization coin to the Finance Technology Ltd. of Pyramid and HSBC Bank Ltd. in Shanghai. Hong Kong has thus become one of the world’s first financial centres to move beyond a complete “legislation-review-dealing” system, which also means that the regulation of the currency is officially moving from policy design to the licensing phase。

In the news, many people have also noticed an interesting signal: the first two to get a license, HSBC owns it independently, and the second is the joint venture between the Scum Charter Bank (Hong Kong) and Hong Kong Telecommunications, Animoca Brands。

In other words, HSBC and scum hit two of Hong Kong’s three main bankers。

What does that mean

I. From "soldier" to "stabilizer."

To be realistic, it is not surprising by itself that the first license plates were rich and slag, but the policy signals released behind this choice deserve careful reading。

This requires a return to Hong Kong’s own very special currency distribution system. It is well known that Hong Kong ' s current currency system is primarily the responsibility of commercial banks, with the exception of HK$10, which is issued directly by the HK$20,50,100,500 and HK$1,000, which are issued by three bankers, HSBC, Scum and China-China。

In other words, with regard to monetary and financial infrastructure, Hong Kong has long accepted a very clear institutional arrangement:The front-office distribution function is carried out by highly regulated commercial agencies, while the regulatory authorities control the stability of the system through rules, reserves and prudential requirements。

In this framework, the first stabilization plates were given to HSBC-led and Scum-led joint ventures, which essentially continue with the idea of "starting with the most secure subjects " , in keeping with Hong Kong's own monetary tradition。

For a new class that has just entered the institutional stage, the first issuances are stable, manageable and unmistakeable, and are in itself a very normal path to financial regulation。

This is not really hard to understand。

While the stabilization currency is in the guise of "virtual assets", once institutionalized, regulation is never the first story, but the most traditional and financial: Whether the reserve assets are real, whether the foreclosure mechanism is clear, whether risk segregation is sufficient, whether the flow of funds is controlled, and whether the AML/T mechanism is reliable。

But this logic naturally leads to another question: why is China's silver Hong Kong absent from the three main banknotes

It is clear that this matter is not simply a question of qualifications or competence. In fact, in August-September 2025, China’s capital Hong Kong was once widely recognized as an active participant in the first applications, until October 2025, when a joint statement at the central level further clarified the policy boundaries, imposing greater restrictions on the issuance of private currency stabilization, particularly the renminbi-linked stabilization currency, and setting aside plans for some of the medium-sized institutions (including China’s capital, China’s capital Hong Kong, China’s capital Hong Kong, Asia, and large Internet enterprises like ants and Kyoto)。

Source:Institute of Rehabilitation

It also means that the first licences were finally given to two banknotes, both as the institutional logic of Hong Kong's initial phase of stabilization and as a realistic answer in the current cross-border policy environmentIf Hong Kong's currency is going to go far, it's up to the next stage。

And that is precisely where much of the discussion is the easiest to ignore。

II. Compliance is important, but "licence" is econometric

In analysing the prospects for Hong Kong ' s stabilization currency, a reference system is the development of the Hong Kong Virtual Bank。

In 2019, the Authority issued 8 virtual banking licences to institutions, with high market expectations, and many believed that the new licensing system would automatically lead to new patterns of competition and new financial experiences; in 2024, the Authority issued a review that indicated that the market was ideal for the overall response to the products and services provided by the eight virtual banks, but also made it clear that the current number of virtual banking licences was suitable and that no new ones would be issued for the time being。

This is a very typical sample. In retrospect, virtual banks are certainly not fruitless, but licensing does not automatically translate into market power, much less into sustainable business models, which also reveals the reality that in a financial system that already has mature profit pools, mature customer relationships, and mature clearing paths, there is often a long distance between system opening and market opening。

To be honest, license plates solve access problems, but not user habits, scene coverage, commercial efficiency and network effects。

The same is true of the stabilization currency, which can only be more difficult。

AFTER ALL, UNLIKE VIRTUAL BANKS, IT NOT ONLY COMPETES WITH THE TRADITIONAL FINANCIAL SYSTEM, BUT ALSO COMPETES GLOBALLY WITH USDT, USDC, AN "OLD PLAYER" WHO IS DEEPLY EMBEDDED IN EXCHANGES, CHAIN AGREEMENTS, AND WALLET SYSTEMS。

At the end of the day, it's not a license that automatically owns the market. The license only solves the problems you can be allowed and trusted to issue stability coins, but it can't solve a few more difficult things:Why would a user use your stabilizer? Why would trading platforms, wallets, merchants, marketers, and corporate financial systems take your stability coin? Why would funds be willing to stay, flow, sink in your system, and eventually create a network effect

In other words, distribution is a supply-side qualification and ecology is the answer to demand。

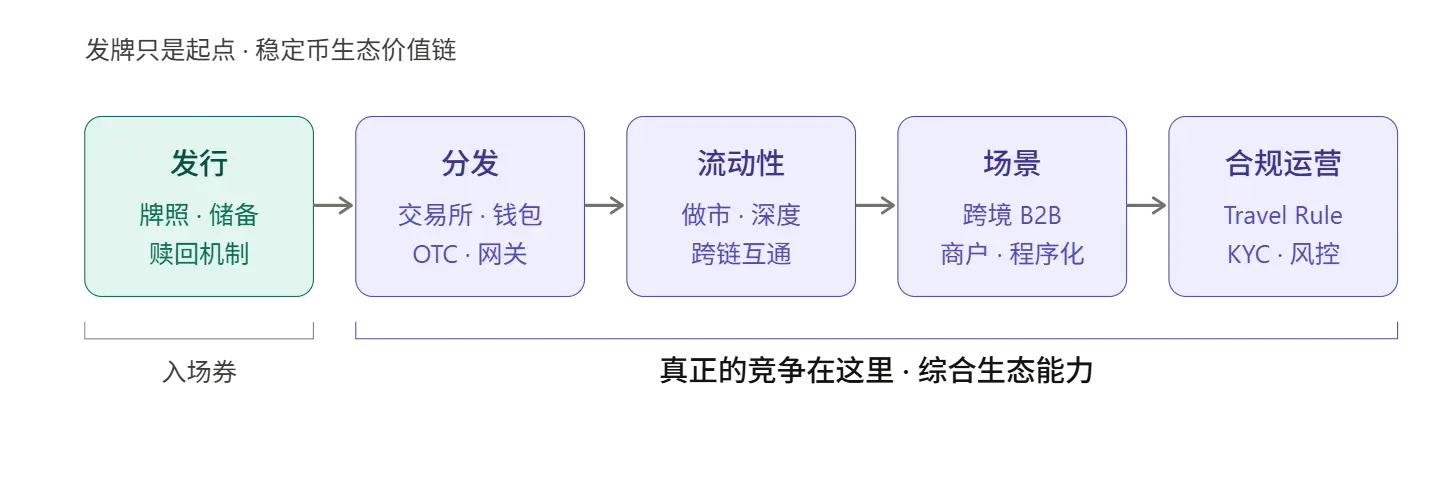

If you look at the competition in the market, the real test starts at the moment when you're dealing, because the chain of competition for a stable currency contains at least five links:

- It's a distribution

- Distribution. The solution is "not in the hands of the user."

- Liquidity. The solution is, "Can't you slow in and out?"

- The solution is "What else to do besides hold."

- Operating, addressing "how to let compliance, liquidation, wind control, identification and users experience long-term stability"

And in these five steps, distribution is just the first。

And that's why the outside criticism that Hong Kong's Stable Money cannot only have a license should not be simply interpreted as a bad song. On the contrary, it points to the next phase of Hong Kong's Stable Currency that really has to be filled with homeworkWhen cards are issued, and without sufficient distribution, mobility, organizational and scenario capacity, Hong Kong ' s stability currency is likely to remain institutionally correct and difficult to move towards commercial success。

Today’s global stable currency market is not a market where compliance labels alone can win users, and user habits, scene entrances, trade depth, clearing efficiency, wallet access, French currency access, developers’ interfaces are the key variables in determining whether a stable currency really survives。

This shift in focus is already evident from the development path of overseas markets。

Upon completion of Bridge’s acquisition, Stripe no longer merely treated stabilization currency as a marginal capacity to pay, but rather further integrated it into enterprise financial management and global payment systems, such as Stablecoin Financial Accounts, which was introduced in 2025 for 101 national enterprises, and later Open Insurance, which was driven by Bridge, are all attempts to upgrade stabilization currency from a supporting alternative asset to a “capacity to pay that can be embedded in an enterprise’s financial system.”。

The action of Circle is equally representative. For some time, Circe has been moving USDC in the direction of more “proceduralized payments”: on the one hand, it openly promotes self-payment based on x402, allowing AIAgents to use USDC to automatically pay API, calculus, data, and content; on the other hand, it is promoting the standardization of small, machine-to-machine payments。

This suggests that, in the eyes of the most sensitive payment infrastructure players, the focus of stabilizing currency competition is no longer just on the issue of eligibility per se, but on who can make it the financial bottom of a business that can be reached, settled and managed。

The previous practice in Hong Kong was that, well before the entry into force of Hong Kong ' s Stabilisation Currency Ordinance last year, the licensed OSL group had launched three new, fully institutional-oriented products: a compliance and stability currency management platform, StableX, asset monetization services, Tokenworks, and an enterprise-level encrypted payment programme, OSL Bizpay, which came online in 2026 as a United States federally regulated, and a United States dollar-compliant enterprise-level stabilization currency that can be distributed in Hong Kong in compliance, mainly in the areas of cross-border electronics, large trade and interactive entertainment。

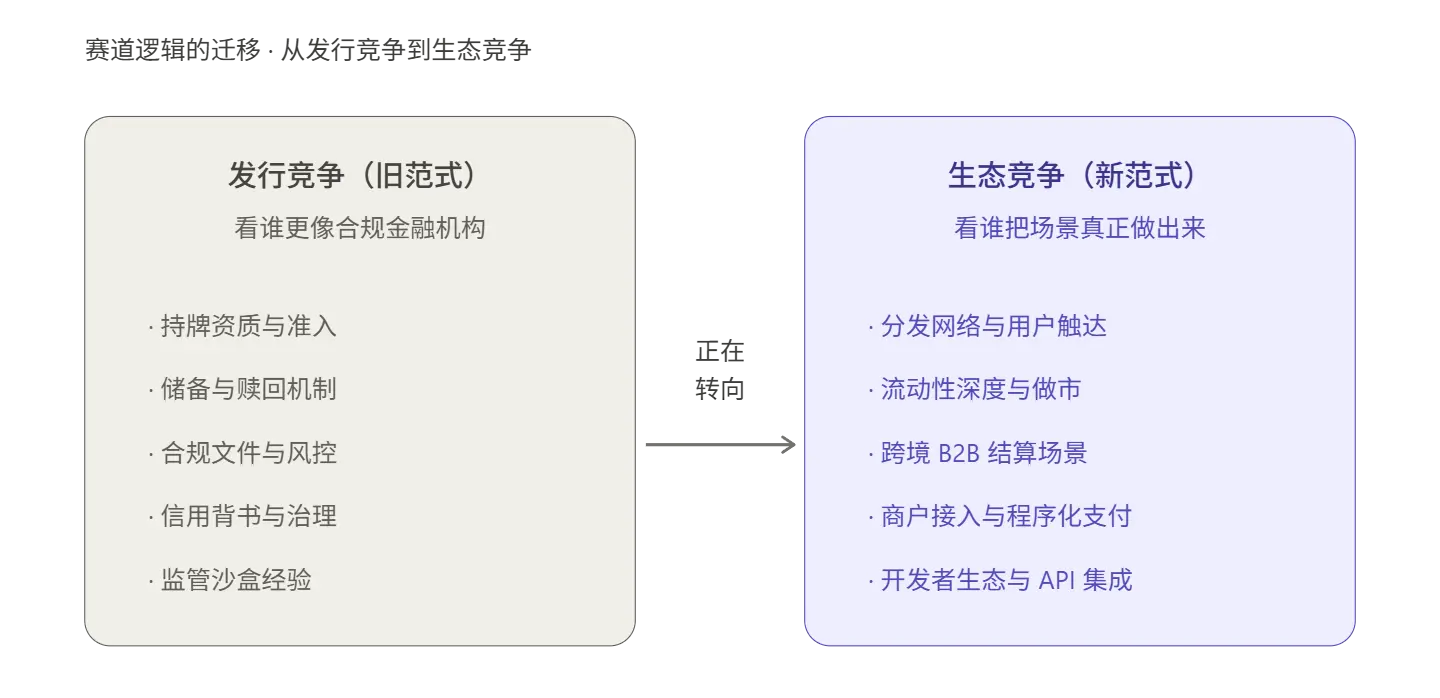

Looking at Hong Kong in this context, one of the more crucial questions is whether Hong Kong’s first card deals will be “who gets in safe first”, but whether Hong Kong will become a truly competitive and stable currency ecology, which is determined by “who will fix the next four things.”。

iii. Distribution is not final, and ecological co-builders are the key

The pattern of the ecological division of labour is becoming clearer in terms of the structure of the global stable currency market。

THE MOST NOTABLE FEATURE IS THE HIGH CONCENTRATION OF THE DISTRIBUTION END. FOR EXAMPLE, USDT AND USDC TOGETHER ACCOUNT FOR OVER 86% OF THE TOTAL MARKET VALUE OF THE STABLE CURRENCY, BUT THE SIZE ADVANTAGE OF THE ISSUER IS NOT NATURALLY EQUIVALENT TO ECOLOGICAL CONTROL, THE REAL COMPETITIVENESS OF THE STABLE CURRENCY, AND IN MANY CASES IT DEPENDS NOT ONLY ON THE SIZE OF THE ISSUE, BUT MORE ON THE DEPTH OF THE FLOW, CHANNEL COVERAGE AND PENETRATION。

USDC, for example, has a market value of 42 per cent of USDT, but is significantly more active in chain transfers, institutional payment scenes and developers’ ecology, which is backed by distribution networks and scene carrying capacity, rather than mere distribution volumes; and PYUSD, whose statutory issuer is Paxos, which is really driving its expansion, is PayPal’s account distribution capacity。

This means thatThe issuer and ecological co-builder of the stabilization coin are already two different combinations of capabilities:

- The issuer is responsible for reserve management, compliance controls and foreclosure mechanisms, which are at the heart of the issue level

- The ecological co-builders are responsible for distribution channels, liquidity aggregation, site access and commercial operations, which are at the heart of the application layer。

The two are not substitutes, but rather upstream and downstream synergies。

If the stable currency ecology is compared to a building, the issuer obtains a licence to build the building on a ground basis, which really determines how high it can be built, and which is the weight structure on each subsequent floor, and which is part of the distribution channel, the liquidity of the transaction, the payment network, the site access, and the capacity to operate in compliance。

So the real test of Hong Kong's stabilization currency is probably not "who gets a license" but "who gets a license and who really uses it."。

That is why the next phase of Hong Kong ' s stabilization currency is truly scarce, not necessarily just as a new issuer, but as an eco-based platform capable of carrying distribution, trading, payment, liquidity and compliance。

In fact, even the first players themselves are already using action to illustrate this. It was reported that the Pepsi Finance Scheme worked with selected enterprises to provide the public with their stabilization currency as distribution partners; HSBC was prepared to reach users through Payme and HSBC HK Mobile Banking。

In other wordsEven the first issuer to get the license plate, the first reaction after landing is not "I can finally deliver the coin," but "How do I distribute it?"This in itself suggests that the stabilization currency is not a business done by the issuer alone, but a system project that must rely on multilevel ecological collaboration。

It is also in this sense that the next phase of Hong Kong is truly scarce, not necessarily just a new issuer, but an eco-based platform capable of distribution, trading, payment, mobility and compliance。

This is also the most visible place in this round of discussions — an integrated capability platform capable of connecting both distribution and circulation and use ends, or a real decision on Hong Kong's stable currency ecological height。

THE ABOVE-MENTIONED HONG KONG-OWNED CARD PLAYER OSL HAS MADE IT CLEAR THAT IT WILL WORK ACTIVELY WITH HONG KONG-OWNED STABILIZER ISSUERS TO TAKE ADVANTAGE OF ITS DISTRIBUTION, MOBILITY AND CAPITAL ADVANTAGES, AND TO PROMOTE THE LOCATION OF THE RELEVANT PRODUCTS AND APPLICATIONS, WHICH MEANS THAT IT WILL BE MORE PROACTIVE IN PLACING ITSELF IN THE SERVICE OF PLACING THE "BREATHING VEINS" OF THIS STABLE CURRENCY NETWORK。

I don't knowFor an emerging market that naturally requires multi-stakeholder collaboration, such roles are not necessarily less scarce than licensing itself。

This is even the key variable that determines whether Hong Kong’s stable currency will take its place in global competition。

At the end

Back to a more macro perspective, the situation facing Hong Kong ' s stabilization currency today is not easy。

In the interior, the policy horizon will not be relaxed in the short term; overseas, the barriers to user habits and network effects are already high, and in this pattern, if Hong Kong's stable currency ecology is only at the level of “dealing-issue-compliance”, it is likely that it will be the same as the virtual banksThe system is doing well and the data are valid, but the larger ecology is not growing。

But this, in turn, is the window of opportunity in Hong Kong。

The global stable currency market is undergoing a profound paradigm shift, and the stable currency is no longer merely an encrypted trading medium within the market, but is being redefined as an infrastructure for the next generation of global payments and settlementsIn this new paradigm, compliance capacity is no longer the only competitive dimension, and distribution networks, payment scenarios, technology infrastructure and eco-operational capabilities become equally, if not more, critical。

As an international financial centre, Hong Kong has a natural advantage in institutional design and compliance governance, but if it is to truly translate this advantage into a stable currency ecological competitiveness, it is clear that the first licences alone will not be sufficient. It will also require the payment of companies, technology platforms, compliance intermediates, Web3 originals and home-owned companies to run the distribution, liquidity, scenes and operations of more difficult and real jobs。

There is still a long way to go after the deal, and real competition for Hong Kong ' s stable currency is just beginning。