The value of the stock is high, but the valuation of the stock is still low

It's been up 850% a year. Why is it cheap?

Original by: +6

Today ' s beauty brings in a historic financial report that gives the semiconductor plate a boost of collective confidence。

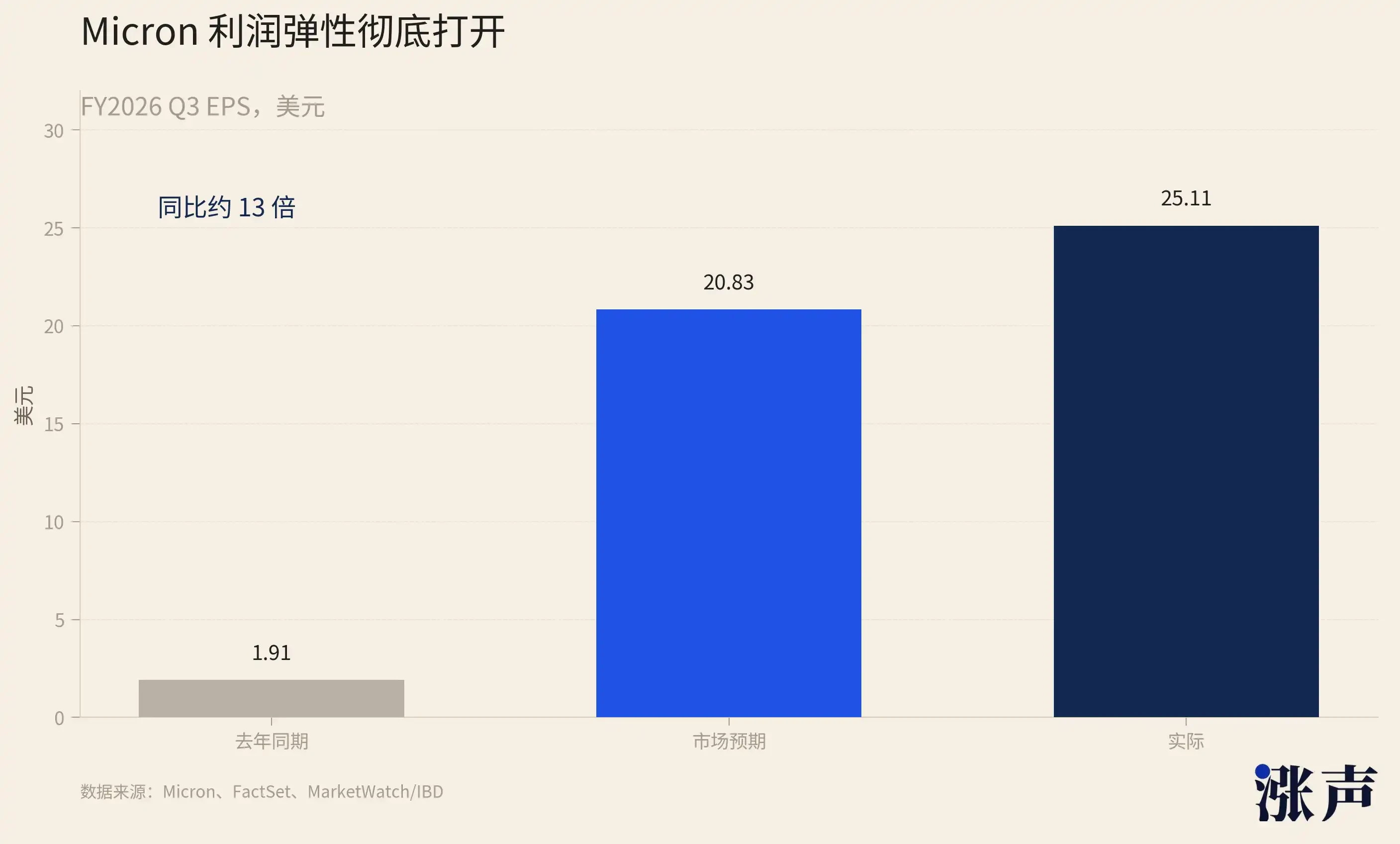

FY2026 Q3 INCOME OF $41.460 BILLION EXCEEDED MARKET EXPECTATIONS BY NEARLY $6 BILLION. A STORAGE COMPANY THAT HAS BEEN LABELLED FOR DECADES AS A "LOW MĀORI COMMODITY" GIVES A GUIDE TO THE MĀORI RATE AT THE LEVEL OF A SOFTWARE COMPANY. THE STOCK PRICE WENT UP BY 13 TO 14 PER CENT, AND IT WENT UP AT $1.16 TRILLION。

The increase in beauty has been exaggerated this year. As at 22 June, closing $1211.38 had more than tripled during the year, more than 850 per cent in the past 12 months, the third best-performing stock of 500 miles in 2026, the first two being Moody and Western data, also stored. The whole plate is going up at this scale. Hercules has increased by over 800 per cent in the past 52 weeks and by more than 400 per cent in the 52nd week。

So many people's first reaction is, of course, "too expensive." In fact, however, the increase in stock prices was much higher than the assessment would have been expensive. In many ways, storage remains a very "cheap" hot track。

THE STOCK PRICE HAS INCREASED NINE TIMES, AND THE PE HAS MOVED ON

ONE OF THE MOST COMMONLY USED INDICATORS FOR DETERMINING WHETHER A COMPANY ' S SHARES ARE EXPENSIVE IS PE, I.E., THE MARKET SHARE。

IN SHORT, PE MEASURES HOW MUCH THE MARKET IS WILLING TO PAY FOR EVERY DOLLAR A COMPANY EARNS. TEN TIMES THE PE, WHICH MEANS THAT INVESTORS ARE WILLING TO BUY ONE DOLLAR A YEAR FOR IT. PE IS HIGH, USUALLY INDICATING THAT THE MARKET BELIEVES THAT FUTURE GROWTH WILL BE STRONG; A LOW PE MAY INDICATE THAT EQUITIES ARE CHEAP, OR THAT THE MARKET BELIEVES THAT THE COMPANY ' S PROFITS ARE NOW ONLY PROCYCLICAL AND WILL SOON FALL BACK。

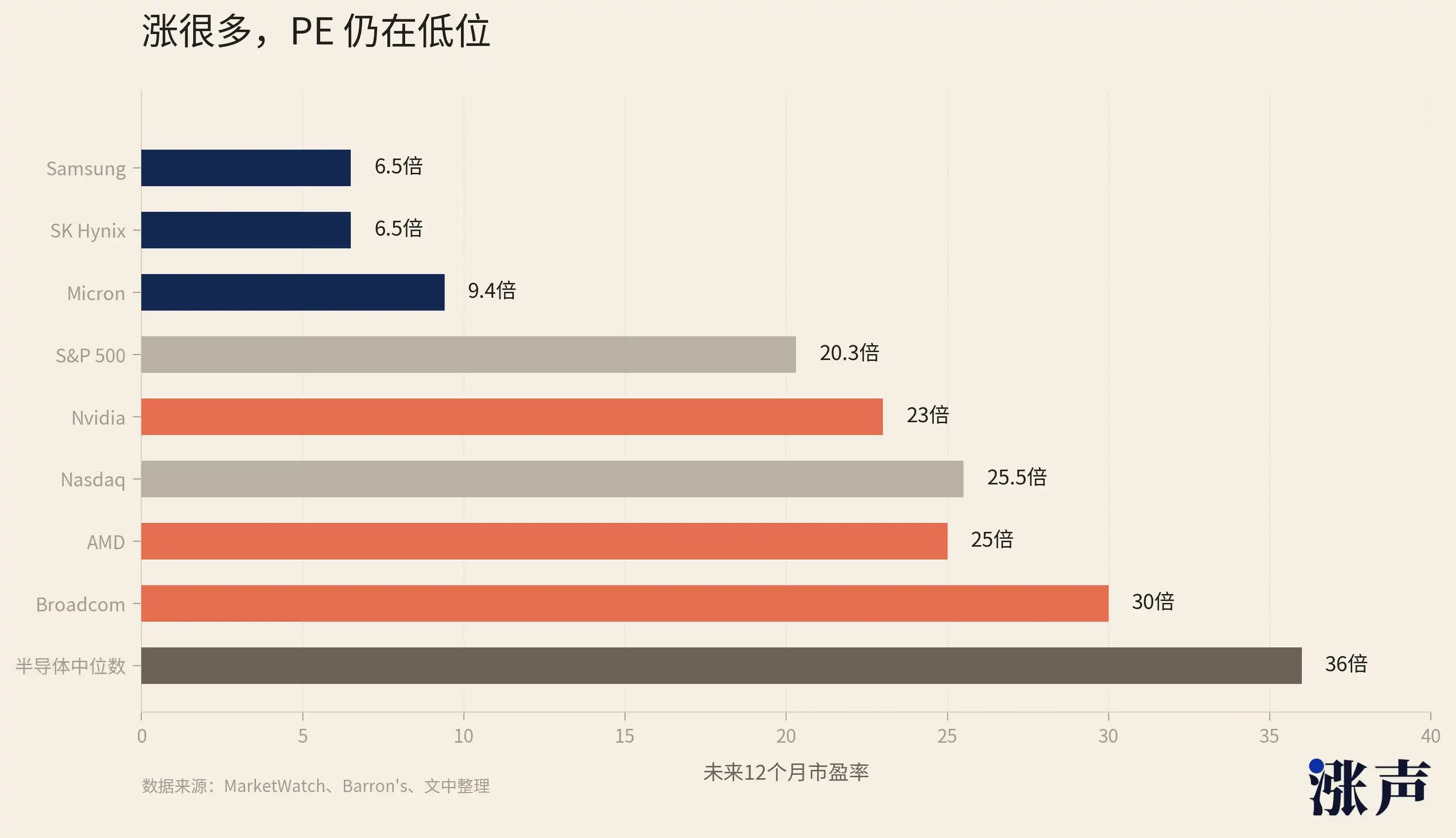

THIS IS WHERE STORAGE IS NOW THE MOST ANTI-INTUITIVE: STOCK PRICES HAVE INCREASED A LOT, BUT PE IS STILL VERY LOW。

According to FactSet, Marketwatch gave a set of figures in its mid-June report: The future of the beautiful light is about nine times that of PE and about 6.5 times that of Hercules and Samsung. For Barren, the long-term PE of American Lights is estimated to be 9.74 times more, but the NASDAQ composite index was about 25.5 times more and the standard 500 about 20.3 times more over the same period. The GuruFocus data on June 21 show that Forward PE of Light is 9.90 times, Hercules at the end of May is 5.92 times, and Tristar is about 5.45 times。

IN OTHER WORDS, MOST OF THE DATA SOURCES SPECULATE THAT THE LONG-TERM PE STORED IN THE THREE GIANTS ARE ALL UP TO 10 TIMES IN SINGLE DIGITS。

THIS SET OF NUMBERS IS IN THE ENTIRE AI CHAIN, ALMOST THE LOWEST SET。

IN WEIDA'S LONG-TERM PE IS ABOUT 23 TIMES AS HIGH, IT'S ABOUT 30 TIMES AS FAST AS IT GETS, IT'S ABOUT 25 TIMES AS HIGH AS IT GETS, IT'S ABOUT 20 TIMES AS HIGH AS IT GETS, AND IT'S ABOUT 36 TIMES THE MEDIAN FOR THE SEMICONDUCTOR INDUSTRY AS A WHOLE. IN OTHER WORDS, THE VALUATION LEVEL FOR THE STORAGE OF THE TRIADS IS ABOUT ONE THIRD THAT OF THE BRITISH WIDA AND ONLY ONE QUARTER OF THE MEDIAN IN THE SEMICONDUCTOR INDUSTRY。

BUT IRONICALLY, THE MONEY IN THE AI INDUSTRY IS INCREASINGLY BEING MADE FROM STORAGE LINKS。

The AI server is not only GPU. Every high-end AI accelerator requires HBM, and every reasoned server requires a large volume of DRAM, KV Cache, model weight, local cache and data throughput. Without HBM, there is no GPU training cluster; without a server DRAM, there is no reasoning cluster; without a high capacity NAND, storage and cache costs for AI applications cannot be charged。

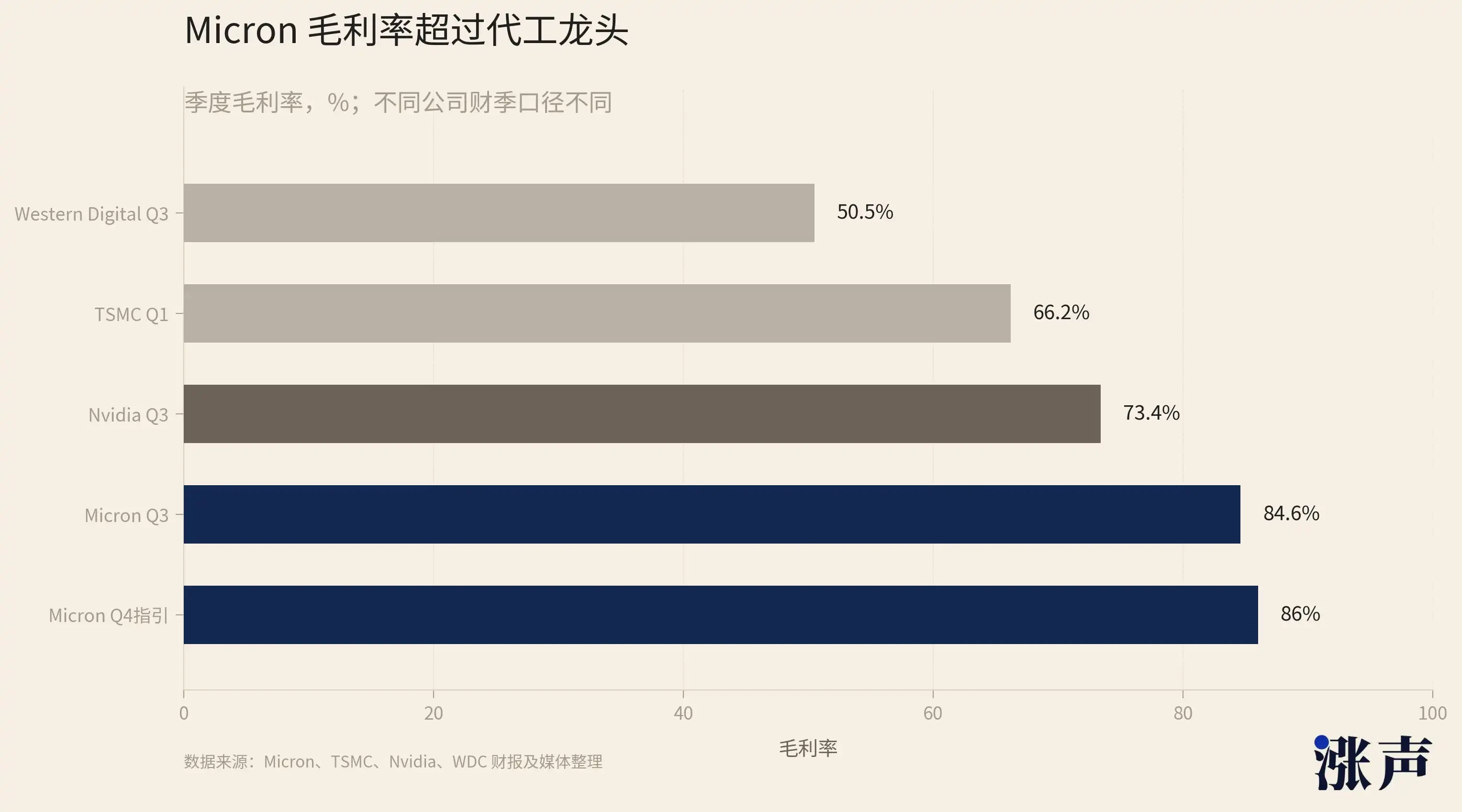

STORAGE IS NO LONGER A COMMON PART OF THE AI INDUSTRIAL CHAIN, BUT A PHYSICAL BOTTLENECK IN WHICH ALL AI CAPITAL EXPENDITURES CANNOT BE BYPASSED. ONE OF THE FIGURES IN THIS FINANCIAL PAPER IS $25 BILLION IN SINGLE-QUARTER DATA CENTRE REVENUES, OF WHICH $5 BILLION, OR 20 PER CENT, IS FOR ENTERPRISE-LEVEL SSD。

As you can see, this bottleneck is now even starting to transfer to consumer electronics。

AI DATA CENTRES PUSH HBM, DRAM, NAND CAPACITY AND PRICES ALL THE WAY UP, AND EVENTUALLY EVEN AN EXTREMELY BARGAINING TERMINAL SUCH AS APPLES HAS TO FACE COST PRESSURE TO TRANSFER SOME OF THE PRICE INCREASES TO CONSUMERS. IN THE PAST, PEOPLE TALKED ABOUT AI MAKING MONEY, AND THE FIRST REACTION WAS YVETTE; BUT NOW IT'S BECOMING CLEAR THAT A LARGE PORTION OF AI'S BILL IS GOING TO STORE。

The stock price of the stock has increased considerably, but profits have increased faster。

MIGWANG JUST RELEASED Q3 EPS 25.11 DOLLARS, COMPARED TO $1.91 IN THE SAME PERIOD LAST YEAR, WHICH IS MORE THAN A DOZEN TIMES THE YEAR. HERCULES'S BUSINESS PROFITS IN 2026 WERE 37.61 TRILLION WON, AN INCREASE OF 405 PER CENT OVER THE SAME PERIOD. THE THREE STAR SEMICONDUCTOR SECTOR Q1 BUSINESS PROFITS INCREASED BY MORE THAN 8 TIMES THE SAME YEAR. THE STOCK PRICE HAS DOUBLED, PROFITS HAVE DOUBLED, AND THE PE HAS NOT BEEN RAISED。

THE AI MONEY IS FLOWING INTO THE PROFIT AND LOSS STATEMENT OF THE STORAGE PLANT。

It's good to concentrate on the release. Mi-guang is only the first shot

It's the money that's been put in the bank for the season。

Next, storage tracks entered a month of extremely dense information: 16 July, Samsung 23 July, Hercules and West 29 July。

AND THE STRENGTH OF THE GUN HAS SET THE TONE FOR THE LATTER. ITS MOST CRITICAL MESSAGE IS NOT A SINGLE-QUARTER OVER-ANTICIPATION, BUT A GUIDE TO Q4'S $50 BILLION INCOME, 86% OF THE MAORI RATE。

This guidance is tantamount to informing the market that the price increase is not only not high but is accelerating. The latter four companies are essentially the same trends revealed in different markets, using different product structures to verify or testify to false light。

First of all, on July 16th, there's an electricity build in the newspaper。

IT'S NOT STORED, BUT IT'S THE BOTTOM OF THE ENTIRE AI CHIP SUPPLY CHAIN. THE GPU IN INWEDA, THE CUSTOM ACCELERATOR IN JB, THE DATA CENTRE CHIP IN AMD, ALL COMING OUT OF ITS PRODUCTION LINE. THE ANSWER TO THE QUESTION IS LOWER THAN THE QUESTION OF STORAGE: WHETHER OR NOT THE CAPACITY BOTTLENECKS OF THE AI CHIP HAVE BEEN OPENED. Q1 INCOME OF $35.9 BILLION, AN INCREASE OF 40.6 PER CENT OVER THE SAME PERIOD, WITH A MĀORI RATE OF 66.2 PER CENT AND ADVANCED PROCESSES ACCOUNTING FOR 74 PER CENT OF THE REVENUE OF THE ROUND. Q2 DIRECTS REVENUES FROM $39 BILLION TO $40.2 BILLION。

A multiplier relationship exists between the build-up and storage of a desk. Every time it sells an advanced crystal circle, there's an AI accelerator downstream, and for every additional accelerator, there's a few HBM blocks. The single GPU combined HBM capacity of the Vera Rubin platform is several times that of the previous generation. The more electricity is generated, the tighter the storage capacity。

July 23 is Samsung's financial report。

15 THE COUPONS EXPECT SAMSUNG Q2 TO HAVE AN OPERATING PROFIT OF ABOUT 88.3 TRILLION WON, WITH A BUSINESS PROFIT OF 66% EVEN OR HIGHER. A COMPOSITE GROUP OF CELL PHONE PANELS THAT DO EVERYTHING, THE PROFIT MARGIN WAS PULLED TO THIS POSITION BY A STORE DEPARTMENT。

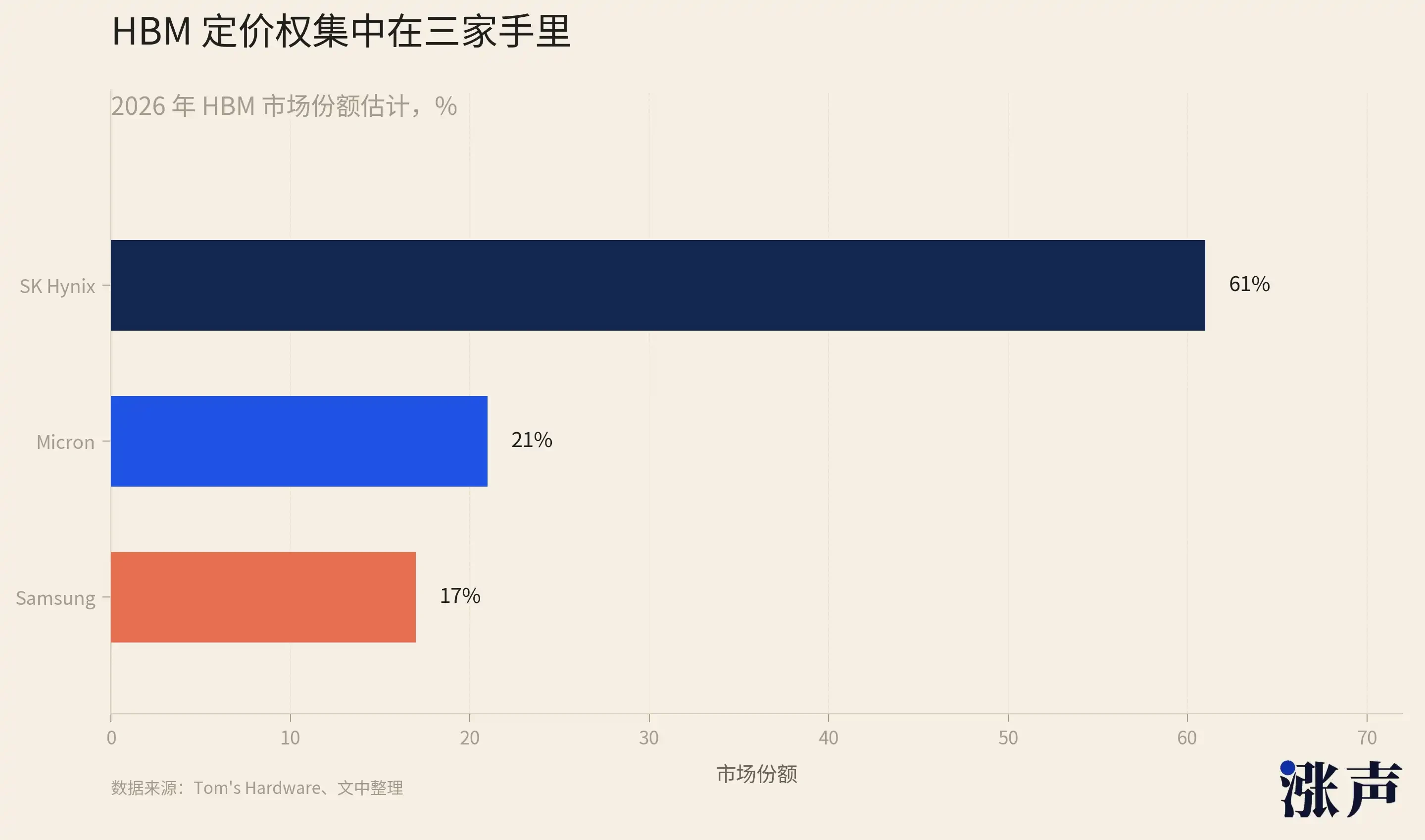

But Samsung's financials are not profit figures, but HBM4. Samsung's share in the HBM market is only about 17%, far behind the 62% of Hercules and 21% of beauty light. HBM4 Intergenerational Switching is the only window for three stars to close the gap. Q1 made a few very specific remarks at the conference: HBM sales increased more than three times the same time in 2026 and HBM4 accounted for more than 50 per cent of HBM sales starting with Q3. Migwang has just revealed that HBM4 36GB 12-Hi has already started to produce quantities. Three card battles on HBM4, one of the most interesting in the second half of the year。

On 29 July, the same day, Hercules and Western data。

HERCULES' Q1 IS AT THE TEXTBOOK LEVEL: QUARTERLY INCOME OF 52.6 TRILLION WON INCREASED BY 198 PER CENT, BUSINESS PROFIT OF 72 PER CENT AND NET PROFIT OF 77 PER CENT. HARDWARE MANUFACTURERS HAVE A NET PROFIT MARGIN OF 77%, APPLES OF ABOUT 25% AND BRITISH WIDA OF ABOUT 58%. SOME OF THE Q2 COUPONS FORECAST A PROFIT MARGIN OF 80 PER CENT. MEI-GOON HAS ACHIEVED 81.2 PER CENT OF THE PROFIT MARGIN AHEAD OF THE BUILD-UP. HERCULES, AS THE FIRST PLAYER IN HBM'S SHARE, Q2 PROBABLY HANDED OVER A SCORE NO LESS THAN THAT OF AMERICAN LIGHT. THE COMBINED OPERATING PROFITS OF SAMSUNG AND HERCULES Q2 ARE EXPECTED TO EXCEED 1.5 TRILLION WON, AND THE COMBINED PROFITS OF THE THREE GIANTS ALONE IN THE QUARTER WILL BE UPDATED。

Western data is the same day Q4, no DRAM and HBM, pure NAND and SSD. It provides another dimension of AI storage needs: the reasoning KV Cache requires a large volume of SSD. Cloud income in Q3 increased by 48 per cent from year to year, with a record Maori ratio of 50.5 per cent. It's worth mentioning that Western Data and Discovery Modi is the best two shares in the 500th grade of 2026, ahead of the beauty light. The growth of the NAND line is not DRAM violence, but it's exactly the same direction。

AI TURNED STORAGE FROM BULK TO LUXURY

THE PRICE OF THE STOCK IS HIGH, THE PE IS LOW, AND THE MONEY IS MORE THAN A BOMB。

It is possible that one might wonder whether all this is sustainable or whether another cycle of festivities will collapse。

And we can look at the analysis of Gitrini Research's semiconductor Jukan。

As early as 2024, when Q1, Hercules and Migwang were still in the post-emergence era of DRAM stocks and stock prices, the Citrini team called them winners. After that, the two stocks rose several times to almost 10 times each. They're almost right about this round of storage. This year, at the beginning of June, there is also a detailed description of his position in the market: He forwarded a report by SemiAnalysis on the adjustment of the memory configuration of the British Rubin server, which put visible surface pressure on Mei-ray and Hercules on the same day。

Jukan’s argument at the heart of the multi-storey is not that of a short-term judgment that “prices will rise”, but that AI turned storage from bulk to luxury goods。

First, HBM broke a curve that lasted 60 years. From 1957 to 2020, the cost of DRAM per gb fell by about one order of magnitude every five years, and the price was falling forever. This is the bottom line of the storage industry, where industry-wide competitive patterns and valuation frameworks are based. Jukan points out that the HBM demand brought by AI has completely broken this pattern. The manufacturers have shifted their capacity to more complex processes, more silica areas, and traditional DRAM supplies have been squeezed。

NONE OF THE MANUFACTURERS ARE PLANNING TO TRANSFER HBM PRODUCTION LINES BACK TO TRADITIONAL DRAM. THE SIMPLE REASON IS THAT HBM PROFITS ARE MUCH HIGHER THAN NORMAL DRAMS, AND RATIONAL MANUFACTURERS DO NOT TRADE HIGH-PROFIT LINES BACK TO LOW-PROFIT PRODUCTS. THIS TRANSFORMS SUPPLY CONSTRAINTS FROM A CYCLE TO A STRUCTURAL PHENOMENON THAT CANNOT BE REVERSED AS LONG AS AI NEEDS REMAIN。

SO THE CONSTANT PRICE INCREASE FOR HBM STORAGE WILL BE LONG。

HBM ' s full-year volume price was largely negotiated at the beginning of the year, giving the manufacturer a strong profit visibility. TrendForce confirms this: Q1 conventional DRAM contract price increases by 90 to 95 per cent in 2026, the largest single-quarter increase since record time, and Q2 continues to rise. The normal DRAM cycle price increase usually lasts between four and six quarters, with the round rising almost eight quarters. Morgan Chase even concluded that DRAM prices could rise for the fourth consecutive year, which had never happened in the history of the industry。

So it can almost be said that storage has changed from bulk commodities to luxury goods。

THE BIGGEST DIFFERENCE BETWEEN LUXURY GOODS AND COMMODITIES IS PRICING. THE PRICES OF LARGE COMMODITIES ARE DETERMINED BY MARGINAL COSTS, WHICH CAN BE EXPANDED FOR EVERYONE, AND PROFITS ARE EVENTUALLY WIPED OUT BY COMPETITION, SO THAT THEY ARE ACCOMPANIED BY A LOW VALUATION. PRICES OF LUXURY GOODS ARE DETERMINED BY SCARCITY AND PRICING RIGHTS, SUPPLY IS CONTROLLED AND PROFITS REMAIN HIGH OVER THE LONG TERM, SO A PREMIUM IS ALLOCATED. THE PREMISE OF THE OLD RULE OF "PE LOW EQUALS THE TOP" IS THAT PROFIT RETURNS TO A LONG-TERM DOWNWARD TREND. BUT IF THE TREND LINE ITSELF HAS TURNED AROUND, RETURNING TO WHERE IT IS IS AN OPEN QUESTION。

BACK TO THE INITIAL CONTRADICTION. EQUITY PRICES ARE HISTORICALLY HIGH AND VALUATIONS ARE HISTORICALLY LOW. THIS ANOMALY EXISTS BECAUSE MARKETS ARE STILL PRICING AN INDUSTRY THAT HAS BECOME LUXURY GOODS USING THE OLD FRAMEWORK OF BULK COMMODITIES. MIGWANG HAS JUST HAMMERED THIS OLD FRAMEWORK WITH A 84.9 PER CENT FINANCIAL ESTIMATE AND 86 PER CENT OF THE MAORI RATE. IF WE DON'T GET BACK, IT'S WRONG TO BE 5 TO 10 TIMES THE PE。

That is why we believe that even if the increase is high, the storage unit will not be expensive。

AFTER HBM, IS NAND THE REAL MAIN COURSE

Every turn of events goes to the middle, and the market asks the same question: who's the next relay。

HBM AND DRAM ARE THE ABSOLUTE PROTAGONISTS OF THIS ROUND OF STORAGE. THE BULGE OF THE THREE GIANTS IS BASICALLY ON THEIR HEADS, AND NAND HAS BEEN USED AS A MATCH。

BUT IF YOU LOOK CLOSELY AT THE SUPPLY AND DEMAND STRUCTURE, YOU FIND SOMETHING COUNTERINTUITIVE: THE NAND THAT'S BEEN USED AS A VIOLET, AND IT'S PROBABLY THE MAIN COURSE, AND IT'S A BIT MORE CRITICAL THAN HBM。

FIRST SAY WHY HBM'S SO FIRE. HBM IS THE DESIGN OF THE AI ACCELERATOR CARD, WITH HIGH UNIT PRICES, HIGH PROFITS AND HIGH TECHNICAL BARRIERS, BY WHICH HERCULES ACHIEVES 62% MARKET SHARE AND 77% NET PROFIT. THESE ARE THE FACTS. BUT HBM HAS ONE CHARACTERISTIC: ITS SUPPLY IS TIGHT, BUT THE PATH TO EXPANSION IS CLEAR. THE THREE GIANTS ARE WORKING HARD ON HBM TO BUILD UP THEIR CAPACITY, SAMSUNG AND MIYUKI ARE CHASING HERCULES, HBM4 AND HBM4E ARE CLIMBING UP FROM GENERATION TO GENERATION. SUPPLY IS INCREASING AT A VISIBLE RATE, ONLY TEMPORARILY FAILING TO KEEP PACE WITH DEMAND。

THE NAND PLANT HAS NOT EXPANDED FOR YEARS。

BECAUSE OF THE 2022 TO 2023 ROUND OF NAND PRICES, ALL THE PLAYERS WERE SCARED. THE CAPITAL SPENDING ON THE NAND OF THE ZHANG MAN, WESTERN DATA, SAMSUNG, HERCULES WAS CUT TO A VERY LOW AND THE NEW PRODUCTION LINE WAS DELAYED UNTIL 2027。

The three giants gave priority to crystal round capacity and capital spending to HBM and high-end DRAM, and the resources left to NAND had been reduced. Mizuoka even shut down the consumer-grade Crucial business and put all the capacity into the enterprise and GPU-grade storage。

THE SUPPLY OF NAND IS MISSING, BUT DEMAND IS HIGH。

The large model reasoning requires a large volume of KV Cache and data throughput, which directly creates an explosive demand for enterprise-level SSD (eSD). In 2026 Q1, the global eSSD income cycle grew by 86 per cent. On the other hand, the HDD shortage. The supply of mechanical hard drives was equally tight, and the data centre was forced to replace HDD with a high-capacity SSD and transferred some of its original requirements to NAND。

The CEO of the cluster electronics said, "Every NAND manufacturer told us that it was sold out in 2026. Zhang also confirmed that all NAND production was sold out throughout 2026. The price of a 1Tb TLC NAND increased from approximately $4.8 in July 2025 to about $10.7 at the end of 2025, more than doubling in months。

HBM IS CRITICAL, BUT SUPPLY IS INCREASING IN A DEFINITE WAY; NAND IS CRITICAL, BUT THE SUPPLY SIDE IS BARELY INCREASING. HBM'S STRESS HAS AN ANTIDOTE, BUT IT'S ONLY SLOW; NAND'S STRESS IS STILL ON FOR A WHILE, BECAUSE THERE'S NO ROOM FOR IT. FROM THIS POINT OF VIEW, THE SUPPLY AND DEMAND GAP FOR NAND IS MORE RIGID THAN FOR HBM AND THE PRICE MAY BE MORE SUSTAINABLE。

AND THAT'S WHY THE TWO BEST-PERFORMING STOCKS IN THE 2026 LOGO 500 ARE NOT HBM DRAGON HERCULES, NOR IS IT BEAUTY LIGHT, BUT PURE NAND AND SSD WESTERN DATA, AS WELL AS BROKEN OUT OF IT. THE MARKET HAS QUIETLY MOVED NAND FROM THE QUARTERING TABLE TO THE MAIN SEAT WITH FOOT VOTES, EXCEPT MOST PEOPLE HAVEN'T NOTICED。

OF COURSE, NAND HAS ITS RISKS. IT'S NOT LIKE HBM HAS AN AI ACCELERATOR CARD, WHICH JUST HAS TO BE TIED, AND DOWNSTREAM DEMAND IS STILL MIXED WITH CYCLICAL FLUCTUATIONS IN CONSUMER ELECTRONICS. NAND'S SCARCE LOGIC IS PREMISED ON THE SUSTAINABILITY OF AI REASONING AND HDD REPLACEMENT NEEDS. AT LEAST AT THIS TIME, NANDS ARE MORE PURE THAN HBMS IN TERMS OF CONTRACT PRICES, STOCK CYCLES, AND WILLINGNESS TO EXPAND PRODUCTION。