IOSG: Consumer-level Cripto Global Census, Users, Income and Track Distribution

The problem of emerging market customers has been resolved and the liquidity problem has not been resolved。

Original title: IOSG Weekly Brief | Consumer Class Crypto Global Census: Users, Incomes and Track Distribution #322

Original by Joey Shin, IOSG Ventures

Summary

The encryption industry says it lacks users every day, but that's not true at all. Consumer-grade encrypted active users have reached tens of millions of levels, just outside Silicon Valley and New York. These people are in Manila, Lagos, Buenos Aires, Hanoi, using Coins.ph (18 million users), Minipay (4.2 million weeks of work), Lemon Cash (Argentina's number one application), but are almost completely absent from the English media。

In turn, the agreements that the Western VC talks every day are not as active as the Tron Shadow Clearing Network in one hour。

Seven core conclusions:The user issue of encryption is essentially a geographical issue; Tron is the most important consumer-grade public chain, but none of NYCs and SFs are talking about it; the chain-based electricians are virtually non-existent; the largest forecast markets are central; income and user numbers are often going backwards; the war on DEX is over; and the really lucrative consumer-grade encryption companies do have it — just not looking like DeFi。

PAYMENTS AND NEW TYPES OF BANKS: USERS ALREADY EXIST, JUST NOT IN VC SIGHT LEE

General awareness: ENCRYPTION NEEDS TO GET INTO THE MAINSTREAM AND BRING IN THE NEXT BILLION USERS. WALLET UX IS A BOTTLENECK。

Data: The next billion users are already present, and the biggest bottleneck is not a customer, but a realization。

Look at the current scale. Telegram Wallet claims to have 150 million registered users (unverified — low confidence), which is set aside。With verified data alone, the user base is already amazing:

Coins.ph has 18 million confirmed users in the Philippines, mainly based on the Tron USDT orbit; MiniPay as Opera's mobile stable currency wallet on Celo amounted to 14 million registered users in March 2026, 4.23 million weekly USDT users, $153 million monthly transactions and 506 per cent growth in chain activity (high confidence - from Tether/Opera/Celo joint disclosure)。

Chipper Cash, which covers 7 million users in nine African countries, recently achieved positive cash flows. Lemon Cash downloads 5.4 million, ranking first in the financial category in both Argentina and Peru, and MAU has quadrupled since 2021. Paga processed transactions amounting to 17 trillion nira in Nigeria during the year, but the proportion associated with encryption is unknown (medium confidence)。

So far, the only paying company that runs both size and revenue is RedotPaySix million users, $158 million in annualized income, $10 billion in annualized transactions, 16 times the value since seed wheels (high confidence - The Block, CoinDesk, corporate disclosure)。

The RedotPay model is an encrypted trans-French card processor for the Asia-Pacific region, a transactional biller with zero risk of non-payment - essentially a encrypted original Visa issuer-receiver。It is the clearest case at present, demonstrating that consumer-level encryption can generate real, recurrent, non-incentive-driven revenues on a scale。

Another bright spot on the revenue side is Exodus, which, according to its SEC 8-K documents, earned $121.6 million in 2025 (high confidence), a small number of publicly listed and audited encrypted consumer companies in United States shares. Its income comes from the exchange and pledge charges of 1.5 million MAU, and shares are listed in the U.S. Board at NYU under EXOD code。

Ether.fi's Cash product is the most noteworthy original entry of DeFi: the first year of profit, with 70,000 + cards, Cash currently contributes about 50 per cent of total income and $2.8 million per month (high confidence - Tokenterminal daily verification). It proves that a DeFi protocol has the capacity to produce real consumer-grade products - although the total number of 200,000 users is still small。

The emerging market customer problem has been solved, and the liquidity problem has not been solvedI don't know. The gap between MiniPay's 4.2 million-week living and its undisclosed (presumably very low) income may be the biggest unresolved problem in the encryption industry - and the greatest opportunity。

marginal improvements vs. non-incremental value: fine-tuned selection criteria

A common rebuttal to consumer-level encryption investments is that encryption must provide a non-incremental value relative to a French currency programme to the cost of hedge integration。The data suggest that the reference to this test is per se wrong。Compare the two most clear data points in the category of payments. MiniPay's advantage over traditional mobile money products such as M-Pesa is at best marginal in the hands of users — a little cheap transfer, a little wider dollar exposure and a little wider cross-border coverage. It has 4.2 million live-time users and earns almost zero. RedotPay's advantage over traditional Visa haircards-collectives is also marginal in consumer experience — brushing cards, buying hot dogs — but the bottom-up mechanisms are structurally different: zero-resistance risk, instant cross-border settlement, no agency dependence. RedotPay generated $158 million in annualized income from 6 million users。

BOTH PRODUCTS RUN THROUGH, BOTH OF WHICH HAVE PMFS. THE DIFFERENCE ISRedotPay’s “marginal but structural” advantage can yield price-fixing rights, while MiniPay’s “marginal and superficial” advantage cannot。Zero non-payment is not a function that users will notice, but it is about 1.5% of the gross profit difference per transaction, permanently captured by the issuing party. A cheap transfer is something that the user takes care of only once and that is not given value after it is used to。

So, the correct screening question isn't, "Is this non-accumulation?" It's "Is this marginal improvement reflected in the structural characteristics of the unit economy?"If the answer is yes — the risk of non-payment, the time limit for settlement, the agency, the efficiency of funds, the cost of hosting — then a product that feels almost unchanged for users can still benefit from a larger business。If the answer is no, the product, even with its tens of millions of users, has no investment value. Both types of consumer-grade encryption have been mixed up, and this category has lost an entire generation of capital。

Electrician

General awareness: Encrypted payments are gradually being used by electricians, only a matter of time。

Data: None of DeFiLlama has a chain-based powerer agreement day agreement revenue exceeding $10,000. It's not very little. It's literally zero。

This chapter is not about competition between initial competitors, but about the absence of competitors。After auditing all the agreements followed by DeFiLlama, TokenTerminal and public disclosure by all companies, we found only one player worth mentioning: Travala, a central tourism booking platform, with revenues of $7.17 million in February 2026 (medium confidence-self-reported, not independently validated). Travala is not an agreement, it's a travel agency that receives encrypted money。

UQUID claims to have 220 million users and 50 million monthly visits (the figure of 220 million actually represents users of cooperative platforms - Binance, etc. - rather than users of UQUID itself). The heading data are misleading, but its product catalogue is indeed quite large - 175 million items of physical goods, 546,000 items of digital goods - Tron doubled its share of its transactions to 39 per cent in the first half of 2025, and 54 per cent of the transactions were valued at USDT-TC20. However, there are no publicly available revenue data and user figures cannot be easily refined。

The gift card and voucher serviceer Bitrefill earned approximately $1 million per month (low confidence - Growjo estimation, historically inaccurate). There are no other chain-based electricians agreements of interest。

There's really a shadow electrician economy on the Tron USDT orbit -- it's P2P, completely informal。Coins.ph deals with remittances from Firao overseas, and money flows to retail consumption. Nigeria's P2P ecology guides $59 billion in encrypted transactions (from Chainalysis) each year through OTC and dollar savings accounts as an alternative to the flawed banking system. In Argentina, the SUBE public transport value is completed through the Tron USDT and the cash OTC channel. Vietnamese freelancers receive wages from TRC-20 USDT and exchange them through the local P2P network。

This is a real economic activity — it is not an electrical infrastructure. No agreement really captures any of them。Virtually all of the entire encrypted power depots — selection, billing, hosting, compliance tracking, dispute resolution, points — are blank。

How much more are left after compliance

Before declaring this one the largest product gap for encryption, one more difficult question must be answered: How many of the existing needs are structural and how many are regulatory arbitrageThe honest judgement is that most of it is regulatory arbitrage。

Today, the dominant pattern in Tron-USDT is divided into three categories:U.S. DOLLAR EXPOSURE NEEDS OF USERS IN CAPITAL-CONTROLLED AREAS (ARGENTINA, VENEZUELA, NIGERIA) — USERS WHO CANNOT LEGALLY HOLD THE UNITED STATES DOLLAR THROUGH TRADITIONAL CHANNELS; CIRCUMVENTION OF VAT, SALES TAXES, IMPORT DUTIES, ESPECIALLY ON DIGITAL GOODS AND GIFT CARDS — DIFFICULTIES FOR TAX AUTHORITIES IN VERIFYING BUYER'S IDENTITY; AND CROSS-BORDER CIRCUMVENTION OF BANK-CONTROLLED FREELANCE AND CASUAL LABOUR PAYMENTS — MAINLY IN VIET NAM, IRAN AND PARTS OF AFRICA。

UQUID'S CATALOGUE OF COMMODITIES IS HEAVILY BIASED TOWARDS GIFT CARDS, PHONE CHARGES AND DIGITAL GOODS, WHICH EXIST PRECISELY BECAUSE THEY CONVERT UNTRANSPARENT ENCRYPTED BALANCES TO A PRICE EQUIVALENT TO A CONSUMERABLE FRENCH CURRENCY AND HAVE LITTLE OR NO IDENTITY FRICTION。

This is crucial to the investment argument, as the survival of regulatory arbitrage requirements under compliance varies significantly。DOMESTIC VAT AND TAX EVASION DEMAND IS ZERO AT THE TIME OF THE MANDATORY KYC AT THE COMMERCIAL LEVEL. THESE USERS DO NOT PAY FOR BETTER BILLING EXPERIENCES, BUT FOR THE "NO TAX NUMBER" COLUMN, WHICH DISAPPEARS AS SOON AS REQUIRED。The demand circumvented by foreign exchange controls is more persistent because its bottom-up problems (Argentina ' s capital controls, Nigeria ' s Naira controls, Venezuela ' s Bolivarians) are structural and long-standing。

However, the platform that serves these needs cannot be legally operated in the required corridors. They can be big, but they cannot be registered, priced and financed, and they cannot cooperate with local financial science and technology issuers — these are the keys to having a moat。

The chances of survival in compliance are narrow but real。

Traditional slow-track or expensive cross-border commercial settlements — Latin America to Asia, Africa to anywhere, freelance collection — can run under any regulatory frameworkBECAUSE THE BOTTOM VALUE PROPOSITION IS "STABILIZED CURRENCY IS A CHEAPER TRACK THAN THE SWIFT STRUCTURE", NOT "STABILIZED CURRENCY HELPS YOU CIRCUMVENT THE RULES."。

B2B SETTLEMENTS BETWEEN SMES IN DIFFERENT JURISDICTIONS ALSO FALL INTO THIS CATEGORY. THE SAME APPLIES TO COMMERCIAL SETTLEMENTS FOR CROSS-BORDER DIGITAL SERVICES。

This led to the introduction of the term "5 trillion-dollar global electrician" as the wrong framework for this opportunity。THE REAL INVESTABLE AREA IS CLOSER TO $20 BILLION TO $40 BILLION IN CROSS-BORDER B2B AND FREELANCE PAYMENTS MARKETS — WHERE VALUE CLAIMS CAN MOVE FROM GREY AREAS TO LEGITIMATE MARKETS。The domestic encrypted closing of accounts for Western consumers — the one that most of the "encrypted payments" claims imagine — is not the opportunity, nor has it ever been。

Winning this type of agreement would look more like "Stabilized Wise" than "encrypted Shopivy". The key question for investors is whether a team is building a viable market or a market that is about to disappear。

Speculation: The End of the End

General awarenessDecentrization is a competitive market where dYdX, GMX and others compete for shares with Hyperliquid。

Data: Hyperliquid has won. GMX and dYdX are not competitors, but agreements at the end of the recession。

Hyperliquid currently controls more than 70 per cent of the unsettled contracts for the permanent sites in all chainsThe monthly nominal turnover of $10.5 billion amounted to $5.8 million in March alone — more than $640 million annually (high confidence - Tokenterminal, DeFiLlama, Dune). In the most recent reporting cycle, the transaction costs increased by 56 per cent. It has executed more than $800 million in HYPE buy-backs, which is one of the few agreements in which the value of the tokens was captured that was not empty。

Compare old cards. GMX earns $5,000 a day and around 500 a day. dYdX earned between $10,000 and $13,000 per day and 1300 per day, a decrease of 84 per cent in the cost of handling。This is not a struggling competitor — an agreement that the runway has already ended mathematically rather than strategically。

edgeX data are noteworthy: US$ 14.7 million for 30 days after verification, 73 per cent retention rate for fees, running on StarkEx ZK-rollup. There was an amalgamation error in our previous data set, which initially showed $2.5 million - after correction, EdgeX was the second most stable place in the chain by income ranking (high confidence - Tokenterminal daily verification). Whether or not EdgeX will sustain growth or will follow the old ways of GMX/dYdX is the only question in this class that remains unanswered。

Hyperliquid is worth looking at because it's not a better deal. The difference between it and GMX or dYdX at the level of order execution is real, but it is only marginal. It wins in depth of liquidity, currency speed and brand。

ONCE MOBILITY IS CONCENTRATED IN ONE PLACE, THE NETWORK EFFECT IS ALMOST UNMOVABLE: TRADERS GO TO THE NARROWEST PLACES, WHERE THE NARROWEST PLACES ARE THE PLACES WHERE THE TRADE IS LARGEST AND WHERE THE TRADE IS BACK. THE LAST DEX CLASS IS ALREADY THROUGH THE WINNER-TAKE-ALL PHASEIn this class, the capital that Hyperliquid deploys is equivalent to burning the money。

Forecasting the market: It's a story of choice, not of decentrization

Another speculative category worth looking at is the forecast market, the dominant narrative being Polymarket's certification of the chain-based forecast market path。The data is about another story — and the lessons of this story have nothing to do with decentrization。

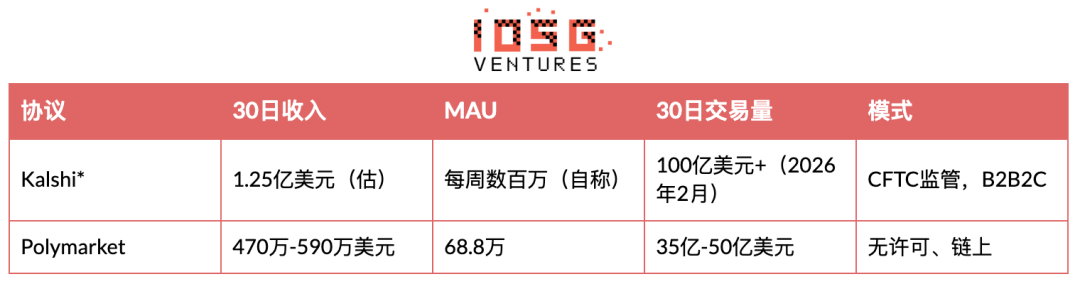

Kalshi is below the chain/class CEX. The contrast itself is a insight。

According to Bloomberg, as of March 2026, Kalshi ' s annualized income amounted to $1.5 billion and was valued at $22 billion. Over $10 billion in transactions were processed in February 2026 alone, with transactions growing 12 times in six months. Sports games contribute 89 per cent of its income. Pollymarket earns between $4.7 million and $5.9 million per month, and MAU 68.88 million per month。Kalshi earned about 25 times the monthly income of Polymark。

The lazy explanation is that Polymark has UX problems. From most product dimensions, Polymarket is the party that's built better -- the order book is cleaner, the settlement is faster, the traders experience even more mature than Kalshi。UX CAN'T AFFORD 25 TIMES THE INCOME GAP。The defense of Polymarket's "not starting to charge" actually makes it worse, not better: if Polymarket loses 25 to one without any rate, the bottom income potential gap is only greater than the apparent figure。

The real explanation is product selection, distribution channels and jurisdictional positioning — these three things have nothing to do with decentrization。

Kalshi chose sports。Sport is a high-frequency, popular and structurally recurrent category:Every day of the week, there is an opportunity to bet, the rules are generally understood and the audience updates itself with the new season. Polymarket has positioned itself in the political and event markets — scattered, dependent on electoral cycles, structurally low frequency. For the users who came to Polymarket in the 2024 general election, there was no reason to come back in March 2026。

For the users of NFL coming to Kalshi, there's a reason to come back every Sunday。Active participation is liquidity, liquidity is price differential, and price differentials are more user-friendly. Polymarket is on the wrong end of the wheel。

The second factor is distribution。Kalshi built a B2B2C model that integrates order book access voucher platforms, financial technology applications and cooperative equations, rather than relying on direct client orientation. Polymarket only does DTC, and every active trader bears the full marketing costs。

The key isKalshi operates legally under the supervision of the CFTC in the United States, and Polymarket, after a settlement with the same agency in 2022, completely geographically blockades American users。The largest projected market audience in English is structurally unreachable by chain products. Kalshi is not just a winner in implementationIt owns a market that Polymarket is legally banned from entering。

The inspiration for the assessment of the forecast market project is specific. The right question is:

(1) The frequency of regular participation in the selected categories

(2) WHETHER THE PROJECT HAS A B2B2C DISTRIBUTION PATH OR DEPENDS ON DIRECT ACCESS

(3) What is the maximum regulatory posture in the market。

The degree of centralization has nothing to do with the result. Polymarket loses 25 to 1 because of the wrong type of product, the wrong distribution mode, the wrong jurisdiction — in that order of importance。

Inferences to this chapter

There are two main points to the speculation board:

(i) Having run out of the winner's class, the winner is really running out of the winner, and capital should no longer be invested there

(2) THE MECHANISM FOR WINNING A WINNER IS NOT DECENTRIZATION, UX OR A CURRENCY ECONOMIC MODEL — IT IS CONSTANT CONCENTRATION OF LIQUIDITY, AND IT IS PRODUCT SELECTION AND DISTRIBUTION THAT PREDICTS THE MARKET。

Both conclusions point to the proposition of DeFi Mullet: the most defensive consumer-end positioning is at the front end of compliance with the encrypted exterior bread。Another.fi Cash is the cleanest case ever. CrediFi and the next generation pay for neighbouring products in the same way。

Stable currency infrastructure: Tron is the most important consumer-grade public chain, but nobody talks about it. It's..

General awarenessEtheum L2 and Solana are the main consumer-class chains, and Tron is an old network that is used mainly for cheap transfers。

DataTron's monthly stable currency transactions of more than $60 billion — comparable to Visa — have 14.3 million MAU, 72.8 million USDT currency holders, and a ratio of 0.2 per cent to 0.3 per cent of the stabilization currency — which proves that its activities are paid rather than speculative. It has an unmarked package of negotiated shadow economies, which the Western media have completely zero coverage。

The numbers are shocking. Tron USDT-TC20 supply is $86.4 billion. Monthly transfers ranged from $60 billion to $135 trillion (threshold confidence - TronScan, TokenTerminal; caps include transactions included in the circular). On March 29, 2026, single-day transfers amounted to $44.9 billion. The network handles more than 2 million transactions per day, covering 13.8 million MAU, of which an estimated 80 per cent or more are below $1,000, of which 60 per cent/70 per cent are below $100。This is a retail payment network, not a whale-led settlement。

Speed indicators are key analytical signals. Tron's USDT speed is 0.2-0.3 times, which means that on Tron's average USDT is rotated only every three to five months。Compared to the speculative public chain, the speed can be more than 10 times - a rapid cycle between the DeFi protocol, leverage position and Launchpad。Tron ' s stable, slow speed is a feature of the payment track: money comes in for a real-world deal, then stays in a wallet and waits for a bill or a remittance. Tron's top 10 USDT holders control only 8.7% of the supply - indicating wide distribution and decentrization of retail sales。

Then the shadow economy. Our audit of TronScan identified several agreements that were not marked and generated significant income but that did not have any documentation in English:

CatFee charges $82,000 per day. No one in the Western encryption media knows what it is. TRONSAVE monthly income US$ 86.33 million, all parties unknown。THESE AGREEMENTS OPERATE IN THE SHADOW ECONOMY OF VIET NAM'S P2P NETWORK, NIGERIA'S OTC PLATFORM, THE PHILIPPINE REMITTANCE CORRIDOR AND THE LATIN AMERICAN CASH CORRIDOR。We estimate that billions of dollars per day pass through these unidentified clearing houses — dynamic addresses, settlements and freelance payment infrastructure — and in fact serve as a banking system for those excluded from traditional finance。

Celo is the fastest growing public chain of the product, driven by the integration of MiniPay and Tether。The number of independent users increased by 506 per cent over the same period, with a total of 12.6 million wallets and $153 million in December 2025 (high confidence). But its size is still only a fraction of Tron。

Etheum remains the institutional settlement track - higher fees limit retail use. Solana ' s stabilization currency activity is dominated by transactions and Launchpad flows (pump.fun, Jupiter, Meteora), not payments. BNB Chain undertakes monthly stable currency transactions of $60 billion, mainly CEX settlements. TON is a variable - Telegram's wallet integration has led to a large amount of registration, but the depth of participation remains unclear。

Synthesis: Regulatory arbitrage life cycle and DeFi Mullet

Each successful consumer-grade encryption category in this census has experienced the same arc line。Starting with regulatory arbitrage; accumulating capital and users in grey areas; experiencing — or unable to withstand — a failure to comply; passing through that part becomes a legitimate financial infrastructure。Agreements that generate real income today and companies are at different stages of the life cycle, and their location determines the risk and return curve of investment。

Phase 1 - Gray zone activated。An agreement or service emerged to address traditional financial refusal or inability to serve, almost always because of a regulatory constraint. Small user groups, highly technical and tolerance of legal ambiguity. Profits are extremely high because regulatory risks are priced. End risk is not capped. Today's examples are CatFee, TronSAVE, Nigeria's P2P USDT stage, and the early days of pump.fun, NFT and even Hyperliquid。

Phase 2 — Users and capital accumulation。PMF HAS BECOME UNQUESTIONABLE. THE VOLUME OF TRANSACTIONS IS GROWING AND USERS ARE BEGINNING TO COME FROM OUTSIDE THE CORE TECHNOLOGY CIRCLES. WESTERN MEDIA ARE BEGINNING TO NOTICE, BUT REGULATION HAS NOT YET BEEN ACTED UPON。Tron's USDT economy is at this stage today - 143 million MAU, monthly turnover of over $60 billion。The period of the 2024 pump.fun, the 2024 general election cycle of Polymarket, and now Hyperliquid are at this stage。

Phase 3 — Compliance transition。A backlash — litigation, enforcement action, conciliation or proactive regulatory communication — promotes the legalization, fragmentation or death of project choices。This is the highest margin and the most analytical stage from an investment perspective。Polymarket's 2022 settlement with the CFTC, $500 million in lawsuits at pump.fun, and any future law enforcement actions against offshore sites for perpetuity are here. Most of the projects could not fully cross this stage。

Phase 4 — Legal EconomyI don't know. The part that passes through becomes permanent, auditable and financeable. The returns were constricted, as businesses were now valued on the basis of financial technology rather than on the basis of a landing project. Kalshi (CFTC regulation, estimate of $22 billion), Exceldus (New York Board, SEC filing), Circle (S-1) disclosure, and RedotPay (financed with comparable multiples of financial technology)。

When the arc is spread like this, the timing of the investment becomes specific。Phase 1 has the largest top-level space, but it is largely not available for institutional capital — the law enforcement order for the bottom business is zero, and the insurance coverage is virtually impossible. Phase 4 has been fully priced; multiples are multiples of financial technology and asymmetries have disappeared。STAGE 2 HAS ALWAYS BEEN THE BEST VC RETURN STAGE IN THIS PLATE, BUT ONLY IF THERE IS A CREDIBLE ROUTE THROUGH PHASE 3。Phase 2 is no longer an issue of "product running" - Phase 2 is clearly running. The question is whether the business model will survive compliance。

Tron ' s shadow agreements cannot get past this, because their raison d ' être is circumvention itself。Once Viet Nam implements KYC, CatFee's daily handling fees for Tron USDT flows, $82,000 disappears -- users pay not for practicality, but for "no identity."I DON'T KNOW. THERE IS NO BUSINESS MODEL FOR COMPLIANCE. THIS IS THE FUNDAMENTAL DIFFERENCE BETWEEN AN AGREEMENT WITH A PMF AND AN AGREEMENT WITH ONLY A REGULATORY PACKAGE. BOTH GENERATE INCOME, BUT ONLY ONE CAN INVEST。

DeFi Mullet's proposition came directly from this framework。Other.fi Cash and the next generation of Latin American financial technology have won because they provide a front-end for compliance outside the encrypted backend. Users don't see or care what the chain is. The regulation sees a general financial technology. The agreement captures the economy of "the cheapest track"。These projects do not currently have any coins — this is in itself a signal that value capture takes place at the equity level rather than at the currency level, and that the institutional investors who will win in the current cycle will be those who hold shares rather than shares。

The three structural opportunities that are recurring in the full text of the briefing are also emerging from this synthesis:

Emerging market liquidity infrastructure (user presence and income not yet in place); the electricity company track paid by cross-border B2B and freelancers (the part of the power supplier gap that survives); and the Tron Neighborhood Ecology, which remains uncovered and in its life cycle phase. Both of them are best suited to the DeFi Mullet modelAll three reward product selection rather than de-centre purity; all three are underestimated today, because Western capital is still looking at the wrong dashboard。

Data quality appendix

All data in the present report are accompanied by one of the following three confidence ratings:

I don't knowHigh- Multiple independent sources, chainable verification, or regulatory filing (e.g. Exodus SEC 8-K, Tokenterminal daily verification, Tether/Opera joint disclosure)

I don't knowMedium- a single credible source, or company self-reported and partially independently certified (e.g. Travala self-reported revenue, Coins.ph Latka estimate)

I don't knowLow— press releases, unverified statements or estimates at the Growjo level (e.g. Telegram 150 million registered, UQUID 220 million users, Bitget 9 million users)

Original Link