Dealing with everything, never losing market: RWA will continue the contract -- DeFi devours Wall Street's last puzzle

Looking to the future, RWA Perps is not just a shadow market for Nasdark or CME, but a bottom-up restructuring of pricing rights, liquidity global distribution and risk transfer mechanisms。

Yes"Preamble."In chapter III of the article, we focused on the projects Syndetix, Gains Network and Ostium. This section will build on the earlier and will build on other representative cases。

III. Representation of the project and architecture game: Predicator pricing + pool (Pool price pricing) vs. Order book

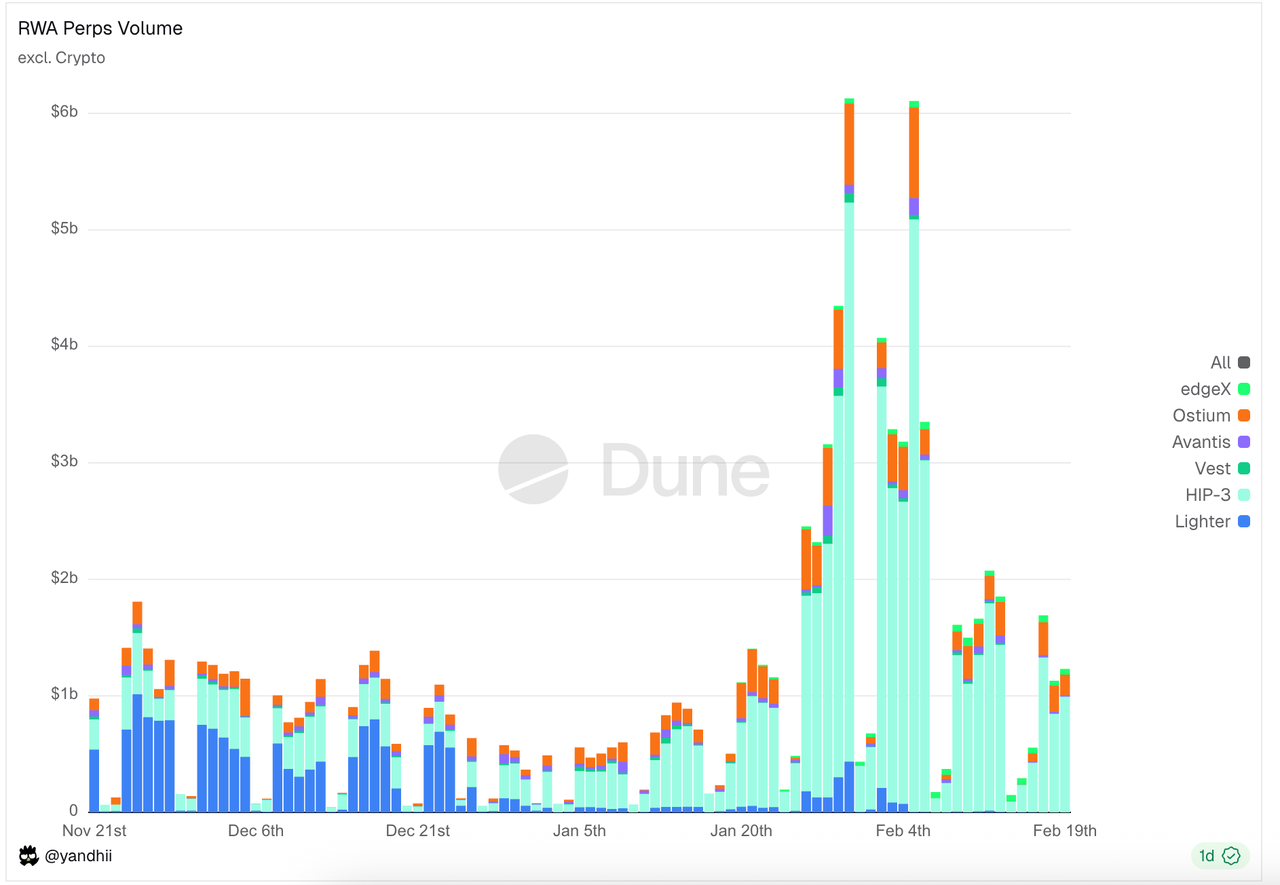

3.3 Orderbook for: Hyperliquid HIP-3 Ecology

In Orderbook, Hyperliquid HIP-3 ecology accounts for the vast majority of transactions and holdouts. There are platforms like Lighter and Vest Markets that compete outside the Hyperliquid ecology。

Data source:https://dune.com/yandhii/rwa-perps

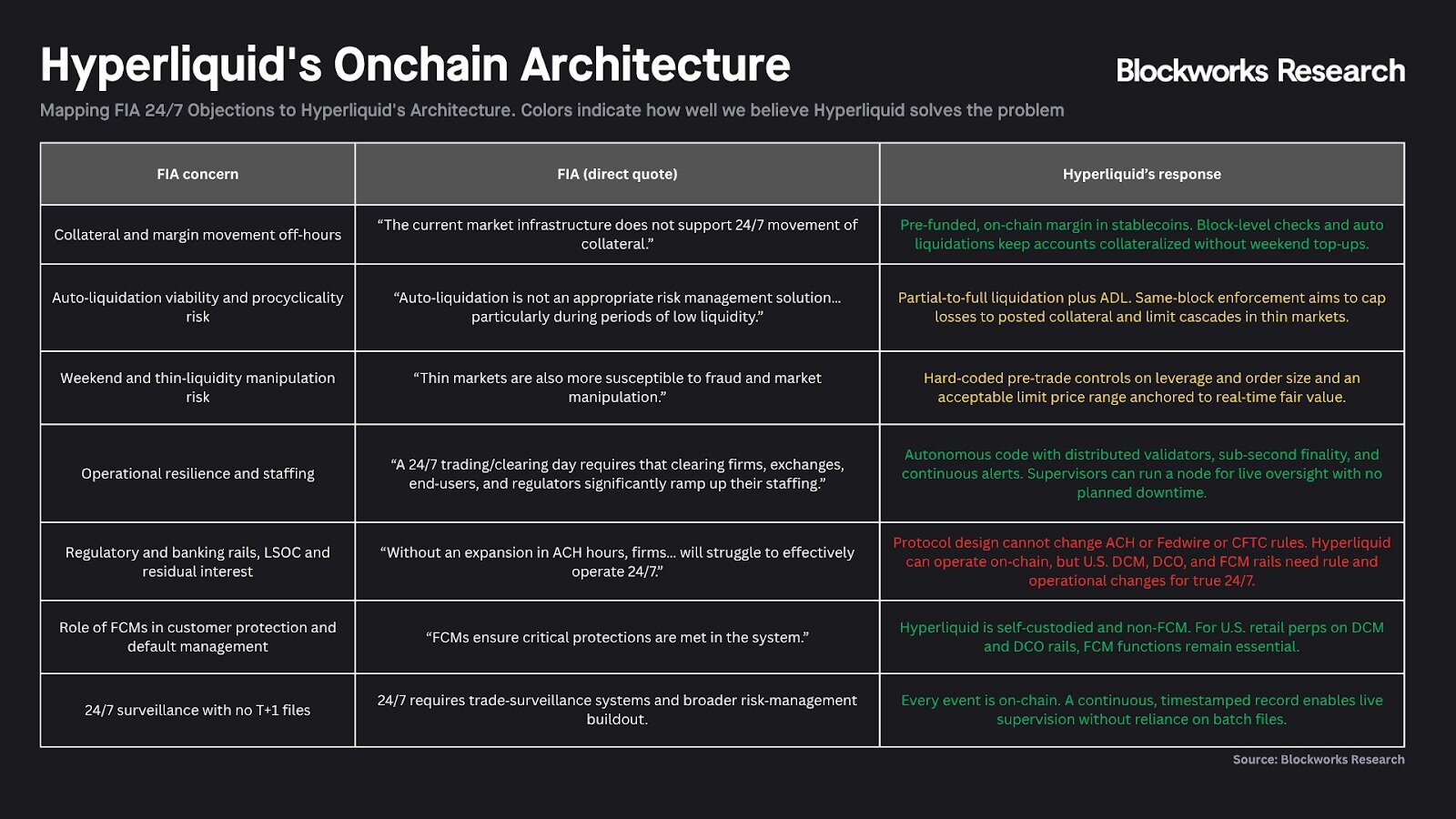

Hyperliquid & HIP-3: Decentralized NASDAQ infrastructure

Hyperliquid completed the strategic transition from a single permanent contract exchange to a “high-performance clearing and blending infrastructure floor” through HIP-3 upgrades. Its central vision is to segregate the functions of the DCM in traditional finance (designated contracting markets) from those of the DCO (designation clearing agency). Under this structure, the Hyperliquid chain itself plays a unified DCO role, providing ground-level blending engines, risk control and financial settlements, while the third-party team, as the “deplacers”, assumes the role of DCM, which is responsible for front-end customers, market operations and asset build-ups. The stratification was designed to create a “decentreized NASDAQ” through a uniform settlement layer carrying a continuum of assets。

Figure: The figure above summarizes Hyperliquid in the hope of becoming “a more open, transparent and efficient financial system”RESPONDING TO CFTC'S CHALLENGE TO THE CONTRACT AND THE 24/7 DEALI DON'T KNOW. FOR EXAMPLE, THE TRADITIONAL DCO DEPENDENCE ON THE BANKING SYSTEM HAS BEEN REPLACED BY A 24/7 AUTOMATIC SETTLEMENT AGREEMENT, WHICH IS BASED ON NON-TRUST TECHNOLOGY. IN ADDITION TO SWOLLEN FCM INTERMEDIARIES, REGULATORY LOGIC FOR RECASTING DCM USING REAL-TIME CHAIN DATA SUGGESTS PHYSICAL TIME DIFFERENTIALS AND EFFICIENCY BOTTLENECKS THAT CAN BE USED TO MOVE DIRECTLY ACROSS TRADITIONAL FINANCE USING BLOCK CHAIN TECHNOLOGY。

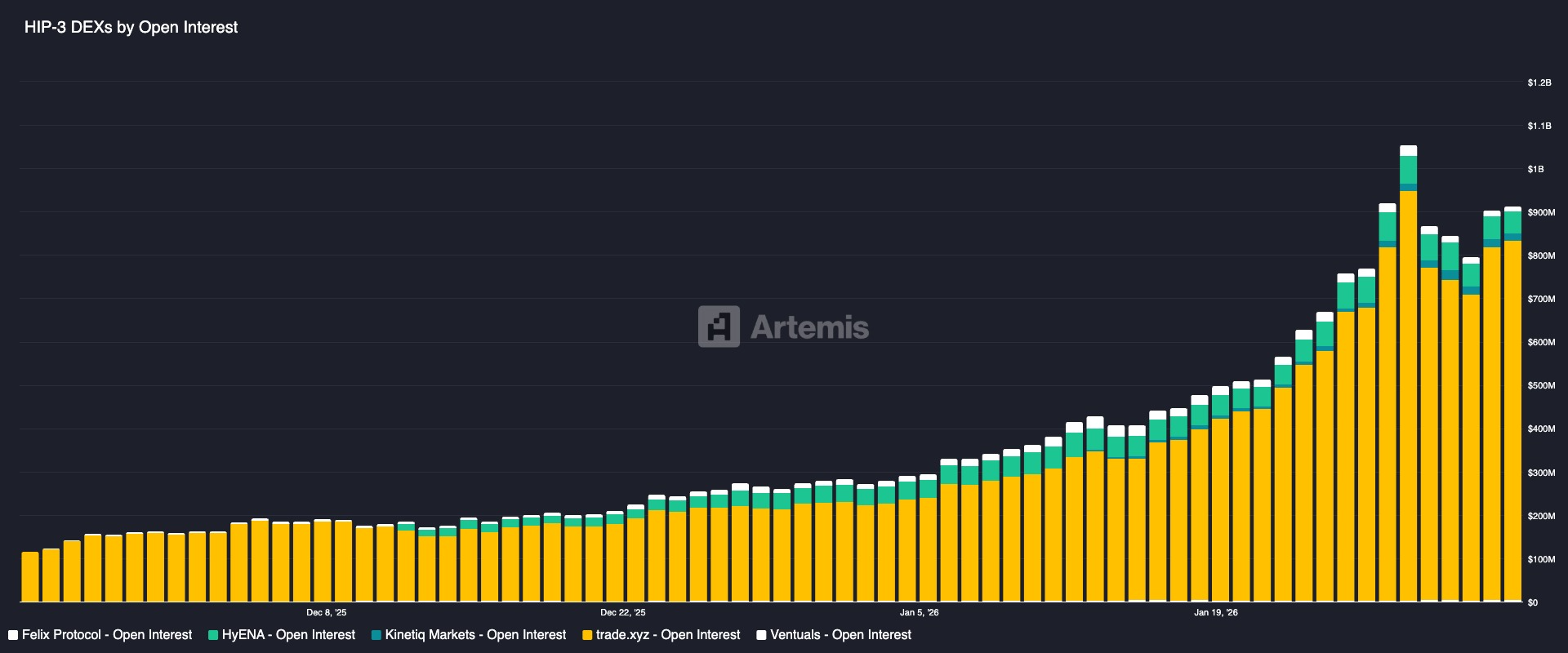

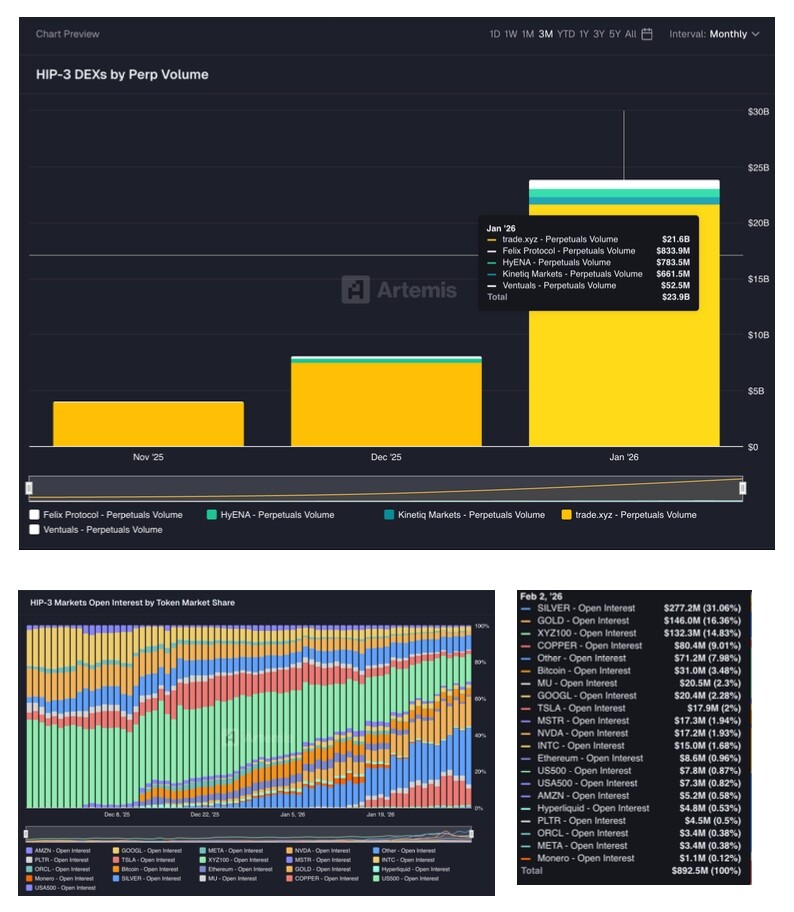

HIP-3 Ecology RWA Perps Project

Project overview

- Trade.xyz was created by HyperUnit, an official corporate asset team of Hyperliquid, and led to the renewal of the XYZ100 contract to track the NASDAQ 100 index and to the leading American technology. Trade.xyz currently leads in all HIP-3 sustainable exchanges, contributing about 90 per cent of the market turnover, with a rich asset bridge (through HyperUnit supporting BTC, ETH, SOL cross-chain liquidity)。

- Markets.xyz is an RWA Perps Dex project launched by the Kinettiq team on Hyperliquid. Markets is slightly different from Trade location: It has focused on indicators and has introduced multiple index/macro perpetuity contracts (covering the Standard 500, the United States share technology index, the euro, the United States Treasury Index, the Energy Index, etc.). Another difference is the use of USDH as a surety currency to significantly reduce transaction costs and increase the return of domestic workers in order to compete with Trade by cost advantage (USDH, an original Hyperliquid stabilization currency issued by the Native Markets team, for distribution in competition with Unit, an asset cross-chain project)Fee relief and return activitiesI don't know。

- Felix was initially a loan and stabilization currency agreement for Hyperliquid, which issued a synthetic dollar feUSD through the CDP and provided a “Felix Vanilla” bond market. Following the roll-out of the HIP-3, Felix has been able to expand its business landscape as one of the deployments of the HIP-3 market for sustainability. Felix also uses USDH stabilization currency for the settlement currency。

- Dreamcash is a mobile end product developed by the Beam Incubation, which locates itself as a mobile trading terminal for RWA renewal。

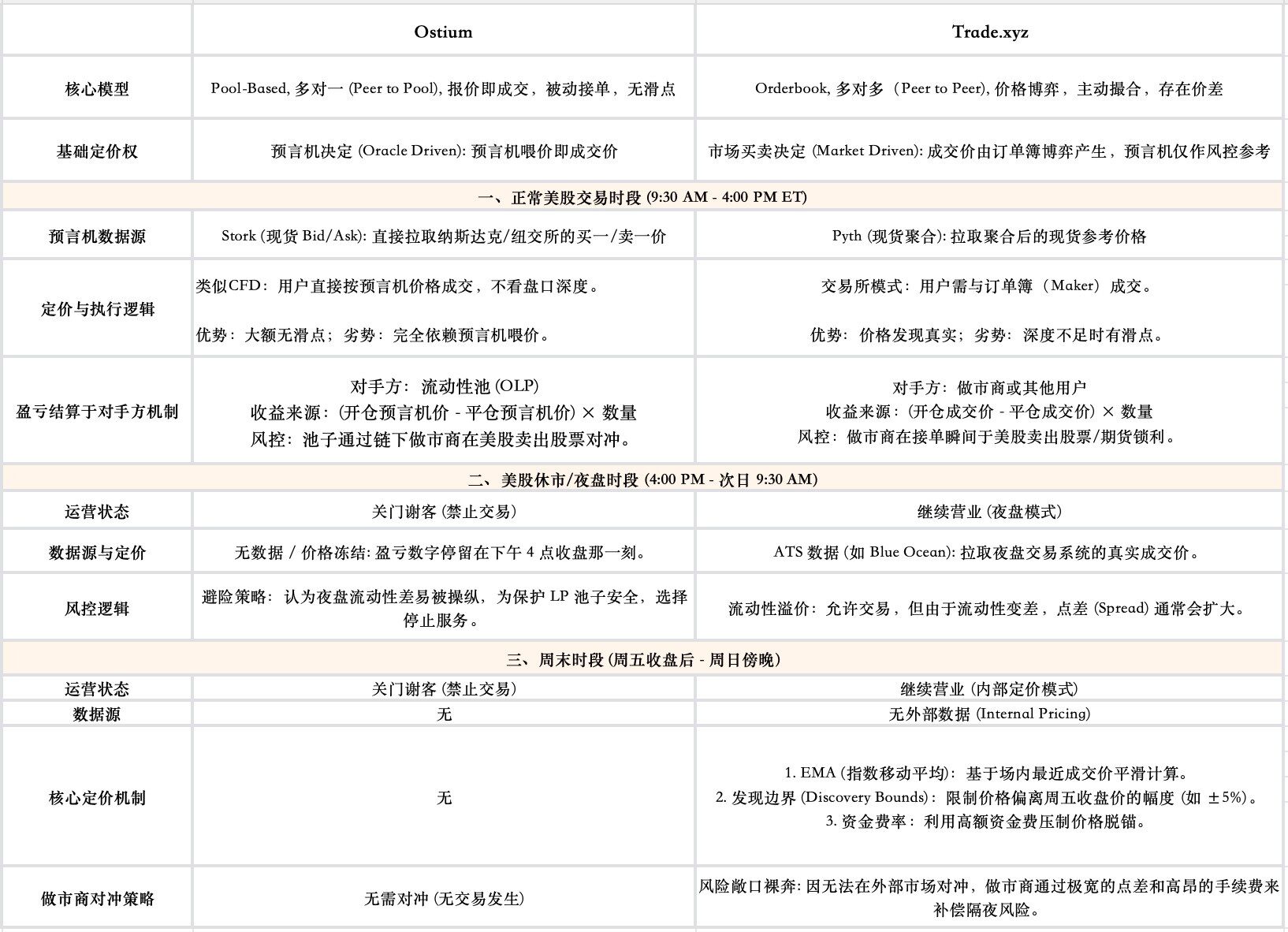

Core pricing mechanisms: market-driven pricing + prophecies

The core technical challenge of the 24/7 RWA Perps project, based on the Orderbook model, is how to still provide fair and robust pricing when the targeted assets are closed. In the example of the HIP-3 ecological lead project, Trade, the core design is a two-track system of market pricing, predictive wind control。

- The heart of the price discovery: the market, not the prophecy

Unlike Pool-based, which made a deal directly with the prophecies, the trading price of Trade was created entirely by the auction of buyers and sellers on its order book. The prophecies do not play the role of “pricing” here, but rather as “tribunals”, which offer prices that are primarily for risk control。

- Marked price: used to calculate the user ' s position gains and losses and to determine whether it is even

The calculation of the system ' s gains and losses, the financial rates and the compulsorily flat rate are not based on instantaneous exchange rates but on a more robust tag price. Trade price is generated by taking the median of three components: a predictor price, a long-term deviation from the average value, and an instant order book price. The purpose of the design was to smooth market noise and prevent malicious manipulations to ensure that user accounts were not mistaken for price collapse in the order book。

- The data source of the prognosis machine in full-time trading time is changed: in order to operate 24 hours a day, the data source of the prognosis machine will be seamlessly transacted according to the time of the United States stock exchange: external prophecies such as Pyth are quoted during normal trading times; nighttime prices (other types of trading system, such as Blue Ocean) are quoted in the ATS; and internal pricing models are initiated on weekends off the market。

3.4 Opium vs Trade price logic versus prophecies

Ostium chose greater security and price accuracy at the expense of some availability (not available on weekends). Trade chose usability and gaming, at the expense of some price stability (which could break anchors or have high financial rate fluctuations on weekends). The role of the prophecies under these two models is also very different, with the prophecies being pricers in the Pool-based model of Ostium, and the prophecies in Trade being adjudicative

Chapter IV RWA Perps Regulatory Constraints Analysis

4.1 Core logic of United States derivative regulation: bottom asset characterization determines compliance path

In the United States financial regulatory system, the first step in determining whether and how a derivative can be listed is to determine the legal attributes of its bottom assets, which directly determine the attribution of regulatory jurisdiction and, in turn, the type of licence that the exchange must acquire。

For assets such as gold, silver, foreign currency (FX) and bitcoin, United States law defines them as “commodity”. The long-term contracts based on such assets fall under the category of commodity futures, with relatively single and clear lines of supervision: They fall fully within the jurisdiction of the Commodity Futures Trading Commission (CFTC). An exchange can operate only if it is registered as a designated contract market (DCM, Designed Contracting Market) and has access to the Derivative Clearing Organization (DCO, Derivatives Clearing Organization)。

However, once the object of the contract is transformed into a single stock or narrow base index (Narrow-based Security Index), a fundamental change occurs:DERIVATIVES INVOLVING A SINGLE OR A SMALL PORTFOLIO MUST BE SUBJECT TO JOINT SUPERVISION BY BOTH SEC AND CFTCI don't know。

THE NEED FOR JOINT REGULATION BY BOTH THE SEC AND THE CFTC IS THE MAIN REASON FOR THE CONTINUATION OF THE CURRENT NON-COMPLIANT STOCK CONTRACTS IN THE UNITED STATES MARKET。The background to this regulation dates back to a territorial war between the SEC and the CFTC in the 1980s, when the SEC and the CFTC fought for regulatory authority over the products of the new futures contracts for emerging stocks, and the final solution to the dispute was that the Shad-Johnson Agreement, signed by the two parties in 1982, directly prohibited trading in single stock futures and narrow base stock forwards on the United States exchange in a nearly one-size-fits-all manner, with the intention of avoiding further inter-agency friction. Although this prohibition was amended by the Commodity Futures Modernization Act (CFMA) of 2000 to allow for the trading of such contracts in the market in the form of “Security Futures Products”, the conditions attached were extremely stringent: the product had to be subject to double regulation by both SEC and CFTC, which constituted a fundamental legal obstacle to equity derivatives innovation。

Any platform that wishes to provide permanent contracts of shares to retail clients in the United States cannot hold a single licence, but must complete both:

- REGISTERED AS A SPECIFIED CONTRACT MARKET (DCM) OR SWAP EXECUTION FACILITY (SEF) IN CFTC

- REGISTERED AT SEC AS A NATIONAL STOCK EXCHANGE

This means that the Platform must simultaneously meet two sets of compliance standards that have been developed by different agencies and that may be in conflict in terms of margin calculations, information disclosure and transaction reporting. This extremely high compliance threshold and operating costs essentially constitute an “access ban” for a single stock contract that will last forever, leading to a near non-existent United States mainland retail product of this type。

4.2 Conflict in exchange structures: why compliance migration costs too much

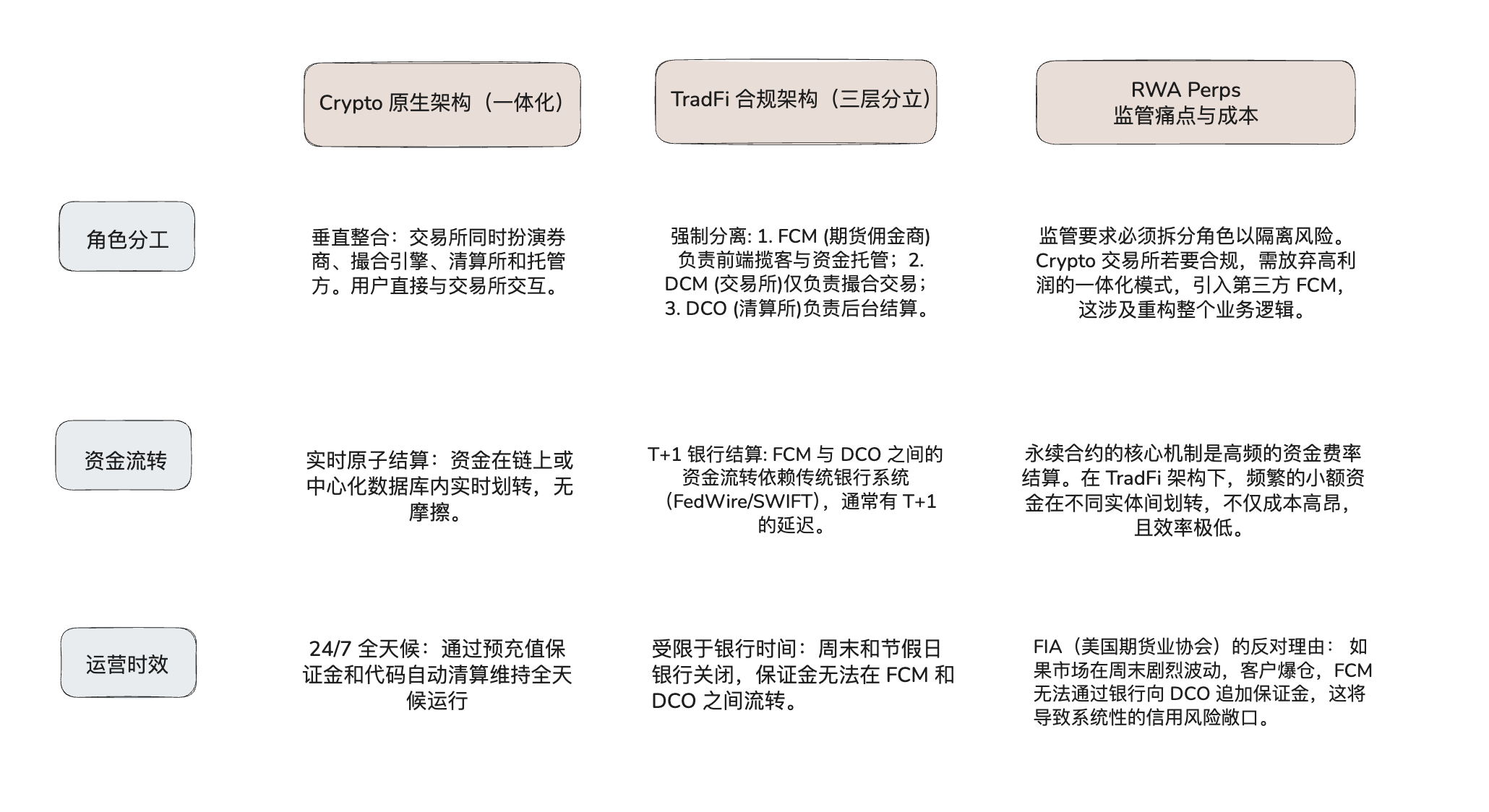

If exchanges in the United States like Coinbase, Robinwood really want to go online on Equity Perps products, in addition to the difficulty of obtaining the above-mentioned legal plates, it will have to face structural conflicts in the bottom infrastructure。

the encrypted currency exchange generally follows an integrated structure of “vertical integration”, while the united states regulatory requirements are a “triple-tiered” structure based on risk segregation. if the crypto exchange is to comply, it will have to dismantle its existing high-efficiency technology depot to adapt to the traditional financial liquidation process。

Cripto compares the analysis of the tradFi market structure:

As a result, the U.S. Exchange will need to address not only the legal aspects of “dual licence”, but also the physical contradiction between “24/7 transaction needs” and “non-24/7 bank settlement systems”. This infrastructure mismatch is currently the largest card point。

4.3 Window opportunities for offshore markets: Regulation S

As United States-owned regulatory restrictions are difficult to break in the short term, the liquidity of the majority of permanent contracts for equities is squeezed into offshore markets. Offshore exchanges (serving non-United States customers) are usually governed by United States securities lawsRegulation S(S)Exemption from compliance. The core logic of the regulation is that no registration in the SEC is required as long as the issue and sale of securities products takes place exclusively outside the United States and the issuer does not make a targeted sale (Directed Selling Projects) against the United States. This requires the platform to technically enforce a strict geographical fence to shield U.S. IPs and to explicitly prohibit U.S. users in legal provisions。

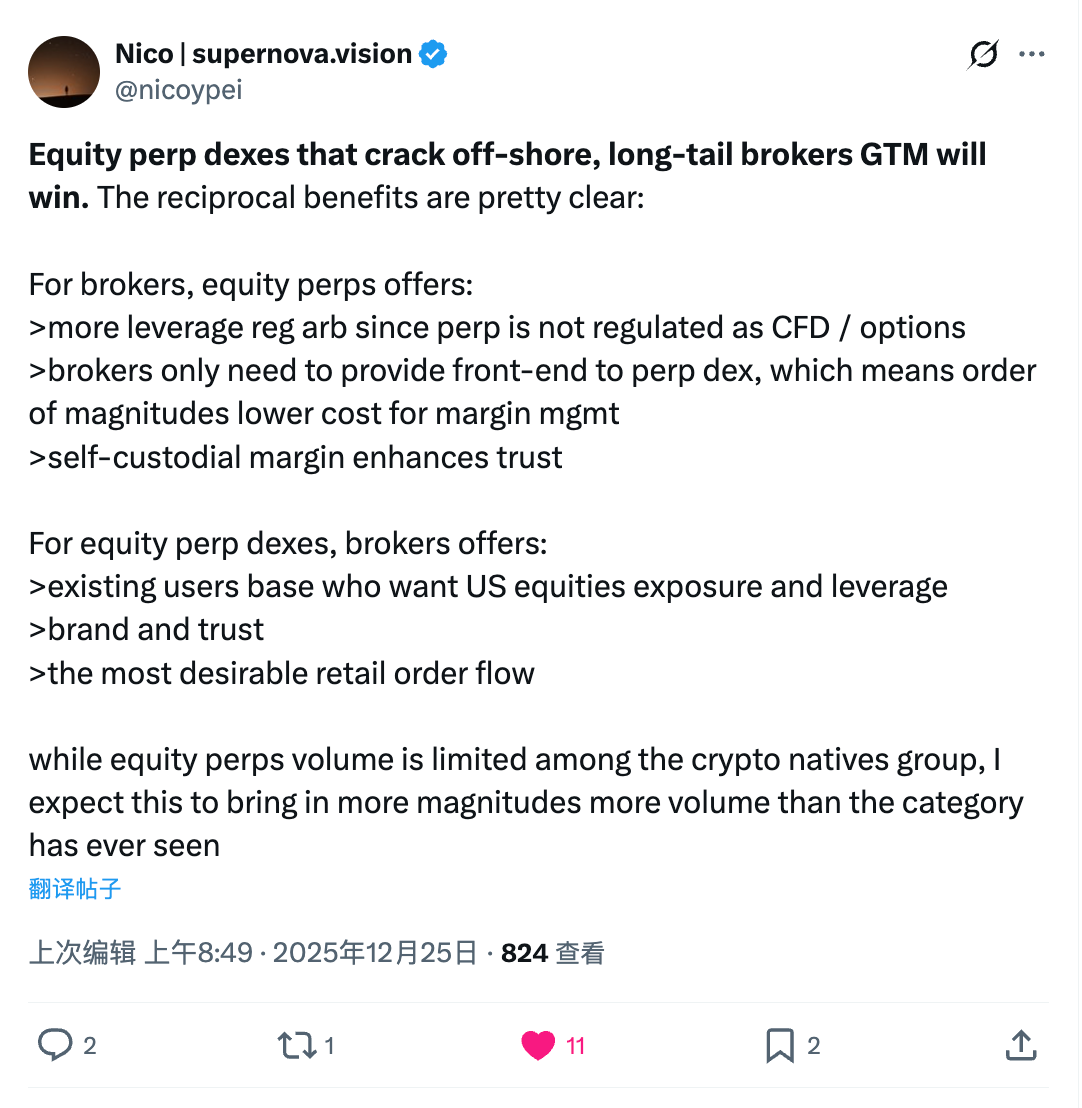

Against this background, RWA Perps Dex is ushering in a unique market window period. They have the opportunity to establish a mutually beneficial commercial distribution model through cooperation with traditional longtail brokers in offshore areas:

The CFD Broker + RWA Perps Dex reciprocity model:SUCH COOPERATION MAY BE ATTRACTIVE TO TRADITIONAL BROKERS, WHICH CAN PROVIDE GREATER LEVERAGE THAN TRADITIONAL PRICE DIFFERENTIAL CONTRACTS, WHICH ARE SUBJECT TO INCREASINGLY TIGHT REGULATION (E.G., THE EUROPEAN UNION ESMA RESTRAINING LEVER), AND CHAIN-LONG CONTRACTS TEND TO REMAIN IN A REGULATORYLY DEFINED BLIND ZONE. MORE IMPORTANTLY, BROKERS SIMPLY NEED TO MAINTAIN A FRONT-END USER RELATIONSHIP AND OUTSOURCE COMPLEX BOND MANAGEMENT, LIQUIDATION AND HEDGE RISK TO CHAIN AGREEMENTS (BACK-END), WHICH WOULD SIGNIFICANTLY REDUCE THE OPERATING COSTS OF BACK-OFFICES. AT THE SAME TIME, THE SELF-CUSTODY OF DEX ADDRESSES THE ISSUE OF USER CONFIDENCE IN THE DIVERSION OF FUNDS BY SMALL AND MEDIUM-SIZED BROKERS。

For Equity Perps Dex, this model solves the most difficult client problem. The interest of encrypted primary users in United States stock transactions is relatively limited, while traditional brokers hold large, real retail flows seeking United States stock openings. By being embedded as a technology backend broker, DEX can handle the KYC/AML process at the front end, while maintaining technology neutrality, thereby providing an opportunity to break the original DeFi world to grow in scale。

4.4 Potential legal risks

While the offshore and DeFi models are commercially logical, they must also be wary of the risk of “long arm jurisdiction” by United States regulators. FOBs still face severe regulatory penalties if they do not completely sever links with United States users at the technical and compliance levels (e.g. through front-end reviews or IP blockades) or if their commercial behaviour is found to be related to the United States market。

CHAPTER V EXTERNAL VARIABLES: THE DUAL IMPACT OF THE NYSE 24/7 PLAN

The New York Stock Exchange (NYSE) parent company, ICE, plans to launch a 7x24-hour trading market, which constitutes the largest external variable on the RWA sustainable contract track. If this change materializes, it will have a profound double impact on DeFi. If users can trade Tesla shares legally and safely at 7x24 hours in regulated New York houses or surplus securities, the advantage of the “day-to-day trading” on which the DeFi agreement depends may be affected. DeFi may then need to look for new value propositions, such as higher leverage, unlicensed access mechanisms, or complex financial products based on compositionality, in order to survive in the face of traditional financial giants。

CORE DRIVERS AND INSTITUTIONAL INNOVATIONS: FROM T+2 TO 24/7 ON THE CHAIN

NYSE plans to launch a 24/7 trading platform designed to use block-chain technology to effect monetization transactions for US shares and ETFs. Its core innovation is to completely break down the “trade-settlement separation” of traditional stock markets and eliminate settlement risks similar to those exposed in the GameStop incident by stabilizing currency receipts, instant settlement payments (T+0) and multi-chain hosting. This is the strategic defence of NYSE against competition from NASDAQ equivalents and global capital against all-weather liquidity needs, marking the evolution of traditional exchanges from “electronic order book” to “full chain-up infrastructure” in an attempt to integrate the efficiency advantages of DeFi under the highest regulatory standards。

CATALYSING AND CHALLENGES TO THE RWA ECOLOGY: ENDING MOBILITY BOTTLENECKS

NYSE'S ENTRY PROVIDED A TOP-END ENDORSEMENT FOR RWA MONETIZATION, ADDRESSING THE “LIQUIDITY DEPLETION” AND “PRICING FAULT” OF CHAIN ASSETS DUE TO WEEKENDS OFF IN TRADITIONAL MARKETS. FOR THE RWA SUSTAINABLE CONTRACT MARKET, 24/7 SPOT-PRICE FLOWS WILL SIGNIFICANTLY REDUCE THE VOLATILITY OF ARBITRAGE COSTS AND FINANCIAL RATES AND INCREASE MARKET DEPTH. WHILE THE NYSE COMPLIANCE “WALL GARDEN” MODEL MAY SQUEEZE THE LIVING SPACE OF SOME NON-COMPLIANT, SYNTHETIC ASSET-TYPE PROJECTS, IT ALSO PROVIDES DIRECTION FOR COMPLIANCE STABILIZATION CURRENCY AND LIQUIDATION FACILITIES. THE ENCRYPTED ORIGINAL RWA PROJECT NEEDS TO USE THE WINDOW PERIOD PRIOR TO LANDING IN 2026 TO CREATE COMPLEMENTARITIES OR COMPETITION WITH TRADITIONAL GIANTS THROUGH DIFFERENTIATED POSITIONING (E.G., HIGH LEVERAGE, NO THRESHOLD, INTEROPERATING ACROSS AGREEMENTS)。

Looking forward: the deep integration of traditional and encrypted finance

Despite disputes in the encrypted community over the investment pressures and regulatory controls of the 24/7 round-the-clock stakeout, the financial chain has become irreversible. In the medium to long term, the intervention of traditional giants will reshape the value chain and transform intermediaries such as coupons and trustees. The future market will evolve into a competing ecological complex: compliance platforms such as NYSE provide high-trust bottom spot liquidity, while the DeFi agreement continues to provide flexibility in innovative derivatives and global asset allocation. With the blurring of encryption and traditional asset boundaries, global capital markets will enter a new era of AI-driven, real-time pricing, atomicized settlements。

Summary

- Structural upgrading of Delta One (linear derivatives)。At present, bulk traders often rely on inefficient trading instruments when obtaining directional leverage. The U.S. ' s 0DTE (end-date rights) would cause unnecessary losses in the Theta (time value) for purely directional bets; and in the off-shore CDF market of up to $30 trillion, there were issues such as the lack of transparency of brokering mechanisms and the risk to the counterparty. The RWA contract for perpetuity completely removes the risk of time loss and centralization and provides this real market demand with a transparent and mathematical linear chain substitution。

- Structure trade-offs in the off-market。Connecting a 24/7-day encryption infrastructure with traditional markets that are constrained by physical transaction time forces agreements to compromise between high leverage, continuous transactions and risk externalities. Two distinct models have evolved in response to the breakout in traditional markets: Ostium's active hedge liquidity pool, which puts solvency first and eliminates flight risk (Gap Risk) by suspending transactions during the break, while Trade.xyz (based on Hyperliquid) maintains 24/7 uninterrupted transactions by converting the risk of weekend fluctuations into dynamic fund rates and market spreads。

- Offshore distribution strategy。In the face of the dual jurisdiction of the SEC and the CFTC, it is not realistic to introduce a compliance-based, long-term contract for the extension of the diaspora. Thus, the RWA Perps early core growth engine will depend on the United States external market (through the Republic of S exemption clause). At the distribution level, RWA Perps Dex may explore in the future models of cooperation with traditional CFC brokers to scale up as a “back-end clearing engine” as a regional offshore broker, without the need to go directly to the front end to access the bulk. • Outsourcing of KYC and front-end buyers to traditional financial entities, with its own focus on chain management and atomicization。

- Adaptation to traditional financial infrastructure。Traditional institutions such as NYSE are moving forward with a business continuity scheme for United States shares, which may soon break DeFi's monopoly on “all-weather transactions”. While this change will completely eliminate the risk of a weekend jump for a chain agreement, it also forces DeFi to diversify competitive strategies. In the long run, RWA sustainable contracts must create differential advantages in terms of unlicensed access, financial efficiency and higher leverage, which eventually evolves into a “high-speed enforcement layer” built on the traditional regulated spot market。

Looking to the future, RWA Perps is not just a shadow market for Nasdark or CME, but a bottom-up restructuring of pricing rights, liquidity global distribution and risk transfer mechanisms. As the liquidity facility grows, it will become the best carrier in the chain for global leverage demand。